Accounting for Partnership: Basic Concepts Class 12 MCQs Questions with Answers

MCQ Questions For Class 12 Accountancy Chapter 2 Question 1.

The persons who have entered into partnership are individually known as:

(A) Partners

(B) Firm

(C) Associations

(D) None of these

Answer:

(A) Partners

Explanation:

Partners are the persons who enter into partnership.

Fundamentals Of Partnership Class 12 MCQ Question 2.

The Agreement of Partnership may be :

(A) Oral

(B) Written

(C) Both (A) and (B)

(D) None of these

Answer:

(C) Both (A) and (B)

MCQ Questions For Class 12 Accountancy Chapter 2 Pdf Question 3.

The maximum number of partners allowed in a partnership firm are:

(A) 50

(B) 100

(C) 200

(D) 400

Answer:

(A) 50

![]()

MCQ Of Accountancy Class 12 Chapter 2 Question 4.

The minimum number of partners allowed to open a partnership firm are :

(A) 10

(B) 2

(C) 5

(D) 20

Answer:

(B) 2

Chapter 2 Accounts Class 12 MCQ Question 5.

Which of the following is the characteristic of a partnership firm are?

(A) Two or more persons are carrying common business under an agreement.

(B) They are sharing profits and losses in the fixed ratio.

(C) Business is carried by all or any of them acting tor all as an agent.

(D) All of the above

Answer:

(D) All of the above

![]()

Class 12 Account Chapter 2 MCQ Question 6.

Following are essential elements of a partnership firm except:

(A) At least two persons.

(B) There is an agreement between all partners.

(C) Equal share of profits and losses.

(D) Partnership agreement is for some business.

Answer:

(C) Equal share of profits and losses.

Explanation:

A partnership firm is an agreement between the two or more persons to carry on a business, but they not necessarily share equal profit or losses unless otherwise provided by the partnership deed or in the absence of one.

Partnership MCQ Class 12 Chapter 2 Question 7.

According to the Partnership Act, the relation of partnership arises from ……………. and not from status.

(A) Business

(B) Statute

(C) Contract

(D) Consideration

Answer:

(C) Contract

Explanation:

There is a contractual relation between the partners of the partnership firm under the consideration of earning profit and carrying out a business.

![]()

Ch 2 Accounts Class 12 MCQ Question 8.

In the absence of Partnership Deed, the profits of a firm are divided among the partners :

(A) In the ratio of Capital

(B) Equally

(C) In the ratio of time devoted for the firm’s business

(D) According to the managerial abilities of the partners

Answer:

(B) Equally

Explanation:

If there is no partnership deed the partners share the profit and losses equally irrespective of the capital invested by them.

Partnership Class 12 MCQ Chapter 2 Question 9.

In the absence of Partnership Deed, interest on loan of a partner is allowed :

(A) at 8% per annum

(B) at 6% per annum

(C) at 12% per annum

(D) no interest is allowed

Answer:

(B) at 6% per annum

![]()

Explanation:

In the absence of partnership deed the interest on loan is charged at 6% p.a. as per the Partnership Act, 1932.

MCQ Of Chapter 2 Accounts Class 12 Question 10.

The partner who provides capital and shares profit and loss in partnership business but does not take active part in the management is known as :

(A) Active Partner

(B) Sleeping Partner

(C) Secret Partner

(D) Limited Partner

Answer:

(B) Sleeping Partner

![]()

Accountancy Class 12 Chapter 2 MCQ Questions Question 11.

Pick the odd one out:

(A) Interest on capital

(B) Interest on drawings

(C) Interest on partner’s loan

(D) Salary to partner

Answer:

(C) Interest on partner’s loan

Explanation:

Interest on partner’s loan is the only one allowed in the absence of a partnership deed.

Class 12 Accountancy Chapter 2 MCQ Question 12.

When there is no partnership deed, the partners are entitled to which of the following?

(A) Salary

(B) Profit share in capital ratio

(C) Interest on loan and advances

(D) Commission

Answer:

(C) Interest on loan and advances

![]()

Explanation:

The salaries, profit sharing ratio, commission, etc. are in accordance with the partnership deed, but if there is no partnership deed the partner needs to pay the interest on loan taken by him 6%.

MCQ On Partnership Chapter 2 Class 12 Question 13.

Which of the following statements is not true?

(A) All partners share profit and losses equally in the absence of a partnership deed.

(B) A minor can be admitted as a partner, only into the benefits of the partnership.

(C) A sleeping partner is allowed to sleep during a meeting of the partners.

(D) None of the above

Answer:

(C) A sleeping partner is allowed to sleep during a meeting of the partners.

![]()

MCQ Of Partnership Class 12 Question 14.

When only Partner’s Capital Account is maintained all the adjustments are made in :

(A) Partners’ Capital Accounts

(B) Partners’ Current Accounts

(C) Cash Account

(D) None of the above

Answer:

(A) Partners’ Capital Accounts

Explanation:

When only Partner’s Capital Account is maintained all the adjustments are made in the Capital account itself and no separate account is to be opened for such thing.

Class 12 Accounts Chapter 2 MCQ Partnership Question 15.

Partners’ Current Accounts are opened when their Capital Accounts are :

(A) Fixed

(B) Fixed and Fluctuating

(C) Fluctuating

(D) None of these 52

Answer:

(A) Fixed

Explanation:

Partners’ Current Account are opened when their capital accounts are fixed, so that all the items and transactions such as interest on capital, drawings etc are adjusted through the Current Account and the capital remains fixed.

![]()

Question 16.

Pick the odd one out:

(A) Interest on capital

(B) Salary to partner

(C) Commission to partner

(D) Interest on drawings

Answer:

(D) Interest on drawings

Explanation:

Interest on drawings is the only item which comes on the debit side.

![]()

Question 17.

Fluctuating capital account is credited with :

(A) Interest on capital

(B) Profit of the year

(C) Remuneration of partners

(D) All of the above

Answer:

(D) All of the above

Explanation:

In case of fluctuating capital account, the capital account is credited with all the transactions related to the capital of the partners.

![]()

Question 18.

Where would the interest on capital be recorded if the fixed capital account is followed in the partnership firm?

(A) Capital Account

(B) Current Account

(C) Profit and Loss Account

(D) None of the above

Answer:

(B) Current Account

Explanation:

The interest on capital is recorded in the current account if the fixed capital account is followed as the capital amount do not change.

Question 19.

Which of the following will not be recorded in the Current Account?

(A) Interest in capital

(B) Interest on drawings

(C) Partner’s Commission

(D) Additional capital brought by a partner

Answer:

(D) Additional capital brought by a partner

Explanation:

Additional capital brought by a partner is recorded in the Capital Account of the partner even if Current Account is maintained.

![]()

Question 20.

Where is the Interest on drawings recorded in the Current Account?

(A) Debit side

(B) Credit Side

(C) Not recorded

(D) Recorded as a foot note

Answer:

(A) Debit side

![]()

Question 21.

In Fluctuating Capital Method, the capital remains …………..

(A) Unchanged

(B) Fluctuates from time to time

(C) Fluctuates only at the start of the year but is fixed at the end

(D) Maintained

Answer:

(B) Fluctuates from time to time

Explanation:

With every transaction relating to the capital of the partners, the capital keeps on fluctuating, in fluctuating capital account.

![]()

Question 22.

Which of the following items is not dealt through Profit and Loss Appropriation Account ?

(A) Interest on partner’s loan

(B) Partner’s salary

(C) Interest on partner’s drawings

(D) Partner’s commission

Answer:

(A) Interest on partner’s loan

Explanation:

Interest on partner’s loan directly comes in the Profit and Loss Account. The partner’s salary, interest on partner’s drawings and partner’s commission are dealt through the Profit and Loss Appropriation Account.

![]()

Question 23.

Pick the odd one out:

(A) Rent to a partner

(B) Interest on partner’s loan

(C) Interest on apital

(D) Deprecudon

Answer:

(C) Interest on apital

Explanation:

Interest on capital is the only item that comes in the Partner’s Capital or Current Account

Question 24.

The Journal Entry to transfer interest on capital to Profit and Loss Appropriation Account would be :

(A) Interest on Capital A/c Dr.

To Profit & Louis Appropriation A/c

(B) Profit & Loss Appropriation A/c Dr.

To Interest on Capital A/c

(C) Profit & Loss A/c Dr.

Partner’s Current A/c Dr.

To Interest on Capital A/c

(D) None of the above

Answer:

(B) Profit & Loss Appropriation A/c Dr.

To Interest on Capital A/c

![]()

Question 25.

Identify the journal entry for transferring interest on drawings to the Profit and Loss Appropriation A/c.

(A) Partners’ Capital/Current A/cs Dr.

To Interest on drawings A/c (Being interest on drawings transferred to Profit & Loss Appropriation A/c)

(B) Interest on Drawings A/c Dr.

To Partners’ Capital/Current A/cs

(Being interest on drawings transferred to Profit & Loss Appropriation A/c)

(C) Interest on Drawings A/c Dr.

To Profit and Loss Appropriation A/c

(Being interest on drawings transferred to Profit & Loss Appropriation A/c)

(D) Profit & Loss Appropriation A/c Dr.

To Interest on Drawings A/c

(Being interest on drawings transferred to Profit & Loss Appropriation A/c) ®

Answer:

(C) Interest on Drawings A/c Dr.

To Profit and Loss Appropriation A/c

(Being interest on drawings transferred to Profit & Loss Appropriation A/c)

Explanation:

When the interest on drawings is transferred to Profit and loss appropriation account, interest on drawings in debited and profit and loss appropriation account is credited.

![]()

Question 26.

Identify the journal entry for transferring salaries paid to the Active Partner A to the Profit and loss Appropriation A/c.

(A) Profit and Loss Appropriation A/c Dr.

To Salary A/c

(Being Salary transferred to Profit and Loss Appropriation Account)

(B) Profit and Loss Appropriation A/c Dr.

To A’s Capital A/c

(Being Salary transferred to Profit and Loss Appropriation Account)

(C) A’s Capital A/c Dr.

To Profit and Loss Appropriation A/c

(Being interest on drawings transferred to Profit & Loss Appropriation A/c)

(D) Salary A/c Dr.

To A’s Capital A/c

(Being interest on drawings transferred to Profit & Loss Appropriation A/c)

Answer:

(A) Profit and Loss Appropriation A/c Dr.

To Salary A/c

(Being Salary transferred to Profit and Loss Appropriation Account)

![]()

Explanation:

When the salary is transferred to profit and loss appropriation account, salary account is credited and profit and loss appropriation account is debited.

Question 27.

When is the Profit and Loss Appropriation Account prepared?

(A) When there are certain adjustments related to partnership.

(B) When the firm is dissolved.

(C) When there is an audit to be done.

(D) It is never prepared.

Answer:

(A) When there are certain adjustments related to partnership.

Explanation:

The profit and loss appropriation account is prepared when there are adjustments to be done with related to the partnership due to the changes that have occurred.

![]()

Question 28.

Pick the odd one out:

(A) Rent to Partner

(B) Manager’s Commission

(C) Interest on Partner’s Loan

(D) Interest on Partner’s Capital

Answer:

(D) Interest on Partner’s Capital

Explanation:

Interest on Partner’s Capital is the the only one that is written in the Capital or Current account.

Question 29.

Mohit and Rohit were partners in a firm with capitals of ₹ 80,000 and ₹ 40,000 respectively. The firm earned a profit of ₹ 30,000 during the year. Mohit’s share in the profit will be :

(A) ₹ 20,000

(B) ₹ 10,000

(C) ₹ 15,000

(D) ₹ 18,000

Answer:

(C) ₹ 15,000

Explanation:

As there is no partnership deed, the profit will be shared equally, that is ₹15,000 each.

![]()

Question 30.

Rahul and Shubham are partners in a partnership. Rahul withdraw ? 4,000 during the year as drawings. Interest on drawings is charged @ 15% p.a. The amount of interest on drawings at the end of the year will be :

(A) ₹ 300

(B) ₹ 600

(C) ₹ 1,200

(D) ₹ 150 IS

Answer:

(A) ₹ 300

Explanation:

₹ 4000 x 15% x \(\frac {1}{2}\) = ₹ 300

![]()

Question 31.

Ramesh and Suresh are partners in the ratio of 3 : 2. Before profit distribution, ‘Ramesh is entitled to 5% commission of the net profit (after charging such commission). Before charging commission, firm’s profit was ₹ 84,000. Suresh’s share in profit will be :

(A) ₹ 32,000

(B) ₹ 48,000

(C) ₹ 56,000

(D) ₹ 32,800 S

Answer:

(A) ₹ 32,000

Explanation:

₹ 84000 x \(\frac {5}{105}\) = ₹ 32,000

Question 32.

Abin, Babin and Chavi are partners in the ratio of 5 : 3 : 2. Before Babin’s salary of ₹ 34,000 firm’s profit is ₹ 1,84,000. How much in total Babin will receive from the firm?

(A) ₹ 55,200

(B) ₹ 79,000

(C) ₹ 89,200

(D) ₹ 45,000

Answer:

(B) ₹ 79,000

Explanation:

Profit = ₹ 1,84,000 – ₹ 34,000 = ₹ 1,50,000

Babin’s Share of Profit = x ₹ 1,50,000 = ₹ 45,000

Babin gets = ₹ 45,000 + ₹ 34,000

= ₹ 79,000

![]()

Question 33.

What will be the interest on drawing 12.5% p.a. for Abhishek if he withdraws ₹ 5,000 once in month?

(A) 13,500

(B) ₹ 7,500

(C) ₹ 3,750

(D) ₹ 3,000

Answer:

(C) ₹ 3,750

Explanation:

\(\frac {5,000 x 12 x 12,5 x 6}{100 x 12}\) = ₹ 3,750

Question 34.

What will be the interest on capital for C @6%p.a for A, B and C who have invested ₹ 15,000, ₹ 25,000 and ₹ 30,000 and share profits in the ratio 1 : 2 : 3?

(A) ₹ 900

(B) ₹ 11,500

(C) ₹ 1,800

(D) ₹ Nil K

Answer:

(C) ₹ 1,800

![]()

Explanation:

6% of 30,000 = ₹ 1,800

Question 35.

Rani and Sumi are partners in the ratio of 1 : 2. Before profit distribution, ‘Rani is entitled to 5% commission of the net profit (before charging such commission). Before charging commission, firm’s profit was ₹ 60,000. Sumi’s share in profit will be :

(A) ₹ 38,000

(B) ₹ 119,000

(C) ₹ 20,000

(D) ₹ 40,000

Answer:

(A) ₹ 38,000

Explanation: ₹ 60,000 x \(\frac {5}{100}\) = ₹ 3,000

Profit after commission = ₹ 60,000 – ₹ 3,000 = ₹ 57 000

ISumi’s Share of profit = ₹ 57,000 x ₹ \(\frac {2}{3}\)

= ₹ 38,000

![]()

Question 36.

Journal Entry to be passed in case of loss on adjustment transferred to Partner’s Current Accounts is :

(A) Profit and Loss Appropriation A/c Dr.

To Partners’ Current A/cs

(B) Partners’ Current A/cs Dr.

To Profit and Loss Adjustment A/c

(C) Partner’s Current A/c Dr.

To Partner’s Capital A/c

(D) None of the above SI

Answer:

(B) Partners’ Current A/cs Dr.

To Profit and Loss Adjustment A/c

![]()

Question 37.

Which account is prepared when past adjustments are to be done?

(A) Profit and Loss Appropriation Account

(B) Profit and Loss Adjustment Account

(C) Both (A) and (B)

(D) Neither (A) nor (B)

Answer:

(B) Profit and Loss Adjustment Account

Explanation:

Profit and Loss Adjustment Account is prepared when the past adjustments are to be done. Profit and Loss Appropriation Account is made to make any transactions of the partners that affect the profit to be shared.

Question 38.

If the interest on capital is omitted what will be the journal entry during the situation?

(A) Profit & Loss Adjustment A/c Dr.

To Partners’ Capital/Current A/cs

(Being adjustment made for interest on capital previously omitted, now carried out)

(B) Profit & Loss A/c Dr.

To Partners’ Capital/Current A/cs

(Being adjustment made for interest on capital previously omitted, now carried out)

(C) Partners’ Capital/Current A/cs Dr.

To Profit and Loss Appropriation A/c

(Being adjustment made for interest on capital previously omitted, now carried out)

(D) Profit and Loss Appropriations A/c Dr.

To Profit and Loss A/c

(Being adjustment made for interest on capital previously omitted, now carried out)

Answer:

(A) Profit & Loss Adjustment A/c Dr.

To Partners’ Capital/Current A/cs

(Being adjustment made for interest on capital previously omitted, now carried out)

![]()

Question 39.

If the interest on drawings is omitted to be recorded what will be the journal entry?

(A) Profit & Loss Adjustment A/c Dr.

To Partners’ Capital/Current A/cs (Being adjustment made for interest on

drawings previously omitted, now carried out)

(B) Profit & Loss A/c Dr.

To Partners’ Capital/Current A/cs (Being adjustment made for interest on

drawings previously omitted, now carried out)

(C) Partners’ Capital/Current A/cs Dr.

To Profit and Loss Adjustment A/c (Being adjustment made for interest on drawings previously omitted, now carried out)

(D) Profit and Loss Appropriations A/c Dr.

To Profit and Loss A/c

(Being adjustment made for interest on drawings previously omitted, now carried out)

Answer:

(C) Partners’ Capital/Current A/cs Dr.

To Profit and Loss Adjustment A/c

(Being adjustment made for interest on drawings previously omitted, now carried out)

![]()

Question 40.

How is the interest on capital is treated in the Profit and Loss Adjustment statement?

(A) Added

(B) Subtracted

(C) No Effect

(D) Not shown

Answer:

(A) Added

Question 41.

E, F and G are partners sharing profits in the ratio of 3 : 3 : 2. As per the partnership agreement, G is to get a minimum amount of ₹ 80,000 as his share of profits every year and any deficiency on this account is to be personally borne by E. The net profit for the year ended 31st March, 2020 amounted to ₹ 3,12,000. What will be the amount of deficiency to be borne by E ?

(A) ₹ 1,000

(B) ₹ 4,000

(C) ₹ 8,000

(D) ₹ 2,000

Answer:

(D) ₹ 2,000

Explanation:

G’s Share = \(\frac {2}{8}\) x ₹ 3,12,000 = ₹ 78000

Deficient to be borne by E = ₹ 80,000 – ₹ 78,000 = ₹ 12,000

![]()

Question 42.

Guarantee of profit to a partner is given by:

(A) Only one partner of the firm

(B) Only two partners of the firm

(C) All the partners of the firm

(D) All of the above

Answer:

(D) All of the above

Explanation:

Guarantee of profit to a partner is given by one or more partner to one or more partner or the firm. The guaranteed amount is even paid in case of loss.

Question 43.

Ram, Shyam and Balweer are partners. They share profit and loss equally. Ram is guaranteed to get ₹ 30,000 profit. Any deficiency if arises, will be borne by Shyam. During the year, they earned a profit of ? 60,000. Which of the following statement/statements is/are correct as per the above information :

(A) Shyam will get ₹ 10,000 as profit.

(B) Balweer will get ₹ 20,000 as profit.

(C) Ram will get ₹ 30,000 as profit.

(D) All of the above 150

Answer:

(D) All of the above 150

Explanation:

Ram’s Share = \(\frac {1}{3}\) x ₹ 60,000

= ₹ 20,000

Deficient to be borne by Shyam

= ₹ 30,000 – ₹ 20,000 = ₹ 10,000

Ram’s Share = ₹ 30,000

Shyam’s Share = ₹ 30,000 – ₹ 10,000 = ₹ 20,000

Balweer’s Share = ₹ 20,000

![]()

Question 44.

When the profits are guaranteed by the partners on the old profit sharing ratio, which of the following is not true?

(A) Amount guaranteed to a partner is transferred to Profit and Loss Appropriation A/c.

(B) Then the remaining profits are distributed among old partners / remaining partners in remaining ratio.

(C) Guaranteed amount is calculated according to his share.

(D) All of the above

Answer:

(C) Guaranteed amount is calculated according to his share.

Question 45.

A, B and C are partners sharing profits in the ratio of 2 : 3 : 1. As per the partnership agreement, C is to get a minimum amount of ₹ 1,00,000 as her share of profits every year and any deficiency on this account is to be personally borne by B. The net profit for the year ended 31st March, 2021 amounted to ₹ 3,00,000. What will be the amount of deficiency to be borne by B?

(A) ₹ 50,000

(B) ₹ 30,000

(C) ₹ 20,000

(D) Nil

Answer:

(A) ₹ 50,000

![]()

Explanation:

C’s Share = ₹ 3, 00,000 x \(\frac {1}{6}\) = ₹ 50,000

Deficient to be borne by B = ₹ 1,00,000 – ₹ 50,000 = ₹ 50,000

Question 46.

Rehana, Shakina and Jasmine are partners. They share profit and loss in the ratio 1 : 2 : 3. Shakina is guaranteed to get ₹ 50,000 profit. Any deficiency if arises, will be borne by Rehana and Jasmine equally. During the year, they earned a profit of ₹ 6,00,000. How much money has to be given to her by Rehana and Jasmine?

(A) ₹ 2,000 by Rehana and Jasmine each

(B) ₹ 2,500 by Rehana and Jasmine each

(C) ₹ 3,000 by Rehana and Jasmine each

(D) Nil

Answer:

(D) Nil

Explanation:

Shakina’s share = ₹ 6,00,000 x \(\frac {2}{6}\)

= ₹ 2,00,000, as she gets the share more than the guaranteed, she will not be reimbursed.

![]()

Question 47.

Ram, Rahim and Robert entered into partnership in the profit sharing ratio of 2 : 3 : 5. Robert guaranteed Ram ₹ 90,000 of profit every year and if there is less he will be reimbursed the deficient amount by him and Rahim in the ratio of 2 : 3. The profit for the year ending March 2021 was ₹ 4,00,000. How much money does Rahim have to give to Ram?

(A) ₹ 4,000

(B) ₹ 6,000

(C) ₹ 2,000

(D) Nil

Answer:

(B) ₹ 6,000

Explanation:

Robert’s Share = ₹ 4,00,000 x \(\frac {2}{10}\) = ₹ 80,000

Deficient = ₹ 90,000 – ₹ 80,000 = ₹ 10,000

Rahim’s share = ₹ 10,000 x \(\frac {3}{5}\) = ₹ 6,000

Question 48.

Tangible Assets of the firm are ₹ 14,00,000 and outside liabilities are ₹ 4,00,000. Profit of the firm is ₹ 1,50,000 and normal rate of return is 10%. The amount of capital employed will be :

(A) ₹ 10,00,000

(B) ₹ 1,00,000

(C) ₹ 50,000

(D) ₹ 20,000

Answer:

(A) ₹ 10,00,000

Explanation:

Capital Employed = Tangible Assets – Outside Liabilities = ₹ 14,00,000 – ₹ 4,00,000 = ₹ 10,00,000

![]()

Question 49.

Goodwill is an ………….. asset.

(A) Tangible

(B) Intangible

(C) Not an asset

(D) None of the above 0

Answer:

(B) Intangible

Explanation:

Goodwill is an intangible asset as we cannot touch it.

Question 50.

Intangible Assets (Goodwill) has been defined in :

(A) AS – 16

(B) AS – 20

(C) AS – 26

(D) AS – 21

Answer:

(C) AS – 26

Question 51.

Identify the formula for calculating goodwill with the help of Average Profit Method.

(A) Goodwill = Average Profit x No. of Years’ Purchases

(B) Goodwill = Total Profit x No. of Years’ Purchases

(C) Goodwill = Total Profit x No. of Years the firm has been in operation

(D) Goodwill = Average Profit x 5 years 0

Answer:

(A) Goodwill = Average Profit x No. of Years’ Purchases

![]()

Question 52.

Identify the formula for calculating goodwill with the help of capitalised method of super profit.

(A) Goodwill = Super profit x No. of Years

![]()

(C) Goodwill = Normal Profit x No. of Years ÷ Super profit

![]()

Answer:

![]()

Question 53.

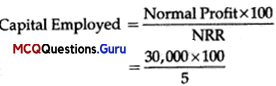

Average profits of a firm during the last few years are ₹ 50,000 and the normal rate of return in a similar business is 5%. If the goodwill of the firm is ₹ 1,00,000 at 5 years’ purchases of super profit, find the capital employed by the firm.

(A) ₹ 6,00,000

(B) ₹ 5,00,000

(C) ₹ 3,00,000

(D) ₹ 2,50,000

Answer:

(A) ₹ 6,00,000

Explanation:

Super profit = \(\frac {1,00,000}{5}\) = ₹ 20,000

Normal Profit = Average Profit – Super Profit = ₹ 50,000 – ₹ 20,000 = ₹ 30,000

= ₹ 6,00,000

Question 54.

How is Goodwill of the firm created?

(A) Due to reputation of the firm

(B) Extra earning capacity of the firm

(C) Both (A) and (B)

(D) Neither (A) nor (B)

Answer:

(C) Both (A) and (B)

![]()

Question 55.

Which of the following factors do not affect the goodwill of the firm?

(A) Competent and capable management

(B) Favourable location

(C) Favourable contracts

(D) None of the above

Answer:

(D) None of the above

Assertion And Reason Based MCQs

Directions: In the following questions, a statement of Assertion (A) is followed by a statement of Reason (R). Mark the correct choice as:

(A) Both Assertion (A) and Reason (R) are true, and Reason (R) is the correct explanation of Assertion (A).

(B) Both Assertion (A) and Reason (R) are true, but Reason (R) is not the correct explanation of Assertion (A).

(C) Assertion (A) is true, but Reason (R) is false.

(D) Assertion (A) is false, but Reason (R) is true.

Question 1.

Assertion (A): Partners shares profit and losses

equally.

Reason (R): Partnership is the relation between persons who have agreed to share the profits of a business carried on by all or any of them acting for all.

Answer:

(D) Assertion (A) is false, but Reason (R) is true.

Explanation:

Partners share profit and losses equally only if provided by the partnership deed or there is no partnership deed.

![]()

Question 2.

Assertion (A): The development of business depends upon the active partners only.

Reason (R): Active Partner is a person who provides his share in capital and also takes active part in the management of the business.

Answer:

(D) Assertion (A) is false, but Reason (R) is true.

Explanation:

As the active partner takes in the part of the management of the business, the development of the business depends on him but it is not completely true as all other partners are to be consulted for the same.

Question 3.

Assertion (A): Secret Partner does not participate in .the affairs of the management.

Reason (R): The secret partner is not liable to pay debts of the firm.

Answer:

(C) Assertion (A) is true, but Reason (R) is false.

Explanation:

Even though the secret partner does not participate in the affairs of the management, he is liable to pay debts of the firm.

![]()

Question 4.

Assertion (A): Nominal partners do not share the profits and losses of the firm.

Reason (R): A firm only uses the name and reputation of the nominal partners.

Answer:

(B) Both Assertion (A) and Reason (R) are true, but Reason (R) is not the correct explanation of Assertion (A).

Explanation:

Nominal partner do not share the profits and losses of the firm, as they are not actually the partners of the firm.

Question 5.

Assertion (A): A minor may become a partner with the consent of all the partners.

Reason (R): A minor partner can share profits and losses as per the agreement but is not liable to pay the debts of the partnership firm.

Answer:

(B) Both Assertion (A) and Reason (R) are true, but Reason (R) is not the correct explanation of Assertion (A).

Explanation:

A minor can become a partner of the firm with the consent of the partners so as to form a partnership agreement.

![]()

Question 6.

Assertion (A): The fixed capital method is better as compared to the fluctuating capital method.

Reason (R): The capital of the partners is fixed, and all the transactions is recorded in the current account.

Answer:

(D) Assertion (A) is false, but Reason (R) is true.

Explanation:

It cannot be determined which I method of maintaining capital is better, it I depends on the preference of the partners.

Question 7.

Assertion (A): The interest on drawings is recorded in the debit side of Current Account when fixed capital method is followed.

Reason (R): The capital of the partners is fixed, and all the transactions is recorded in the Current Account.

Answer:

(A) Both Assertion (A) and Reason (R) are true, and Reason (R) is the correct explanation of Assertion (A).

Explanation:

The interest on drawings is recorded in the current account so as to maintain the capitals of the partners fixed.

![]()

Question 8.

Assertion (A): The interest on capital is recorded in the debit side of the Current Account when fixed capital is maintained.

Reason (R): The capital of the partners is fixed, and all the transactions is recorded in the current account.

Answer:

(D) Assertion (A) is false, but Reason (R) is true.

Explanation:

The interest on capital is recorded in the credit side of the current account.

Question 9.

Assertion (A): When the partners put in additional capital, it is recorded in the credit side of the Current Account.

Reason (R): Current Account records all the transactions relating to the interest on capital, drawings, commissions to partners, etc. when the capital is to remain fixed.

Answer:

(D) Assertion (A) is false, but Reason (R) is true.

Explanation:

When a partner puts in additional capital it is shown in the capital account even if fixed capital is to be followed.

![]()

Question 10.

Assertion (A): Profit and Loss Appropriation Account shows the correct profit earned by the firm.

Reason (R): The net profit is adjusted after taking into account the interest on capital, interest on drawings, salaries/commissions paid to the partner in the Profit and Loss Appropriation Account.

Answer:

(A) Both Assertion (A) and Reason (R) are true, and Reason (R) is the correct explanation of Assertion (A).

Explanation:

The profit and loss appropriation account shows all the other items that needs to be taken into account to be distributed among the partners to find the correct profit of the firm.

Question 11.

Assertion (A): The Profit and Loss Appropriation Account is an extension of the Profit and Loss Account.

Reason (R): Profit and Loss Appropriation Account starts with the Net Profit as found in the Profit and Loss Account.

Answer:

(A) Both Assertion (A) and Reason (R) are true, and Reason (R) is the correct explanation of Assertion (A).

![]()

Question 12.

Assertion (A): Profit and Loss Appropriation Account is only prepared when there are certain adjustments related to partnership.

Reason (R): Profit and Loss Appropriation is prepared to ascertain the profit earned by the firm and distribution among the partners.

Answer:

(B) Both Assertion (A) and Reason (R) are true, but Reason (R) is not the correct explanation of Assertion (A).

Explanation:

Whenever there is an adjustment relating to the partnership, Profit and Loss Appropriation Account is made to ascertain and divide the profit among the partners.

Question 13.

Assertion (A): If percentage of interest on capital is not mentioned in partnership deed, partners will not receive any interest on capital.

Reason (R): The interest on capital is charged on the capital invested by the partners.

Answer:

(B) Both Assertion (A) and Reason (R) are true, but Reason (R) is not the correct explanation of Assertion (A).

Explanation:

The interest on capital is charges in accordance with the partnership deed, and if not mentioned it will not be charged.

![]()

Question 14.

Assertion (A): If percent of interest on drawings is not mentioned in partnership deed, firm would not charge any interest on drawings of partners. Reason (R): Interest on drawings is charged only when there is profit.

Answer:

(C) Assertion (A) is true, but Reason (R) is false.

Explanation:

Interest on drawings is charged even when there is a loss.

Question 15.

Assertion (A): Partner needs to pay the interest on loan at 6% even if not mentioned in the partnership deed.

Reason (R): Interest on loan to partners is charged as per the Section 13 (d) of the Indian Partnership Act.

Answer:

(A) Both Assertion (A) and Reason (R) are true, and Reason (R) is the correct explanation of Assertion (A).

Explanation:

As per the section 13(d) of the Partnership Act, the interest on the loan is to be charged at 6% even if it is not mentioned in the partnership deed.

Question 16.

Assertion (A): When the items are omitted it is necessary to prepare Profit and Loss Adjustment Account only.

Reason (R): For the purpose of correcting these omissions or mistakes, adjustment entries are passed through Profit and Loss Adjustment Account in which adjustments in respect of each and every omission are to be made.

Answer:

(D) Assertion (A) is false, but Reason (R) is true.

![]()

Explanation:

When the items are omitted, profit and Loss Adjustment Statement or necessary journal entries can be passes when Profit and Loss Adjustment Account is prepared.

Question 17.

Assertion (A): Interest on capital amount to ?15,000 was shown on the credit side of the Profit and Loss Adjustment Account.

Reason (R): Interest on Capital is to be credited to the Capital/Current Accounts of the Partner.

Answer:

(D) Assertion (A) is false, but Reason (R) is true.

Explanation:

Interest on capital is shown on the I debit side of the Profit and Loss Adjustment Account.

Question 18.

Assertion (A): The interest on drawings omitted is shown on the credit side of the Profit and Loss Adjustment Account.

Reason (R): Profit and Loss Adjustment Account is prepared when there is an omission of items.

Answer:

(B) Both Assertion (A) and Reason (R) are true, but Reason (R) is not the correct explanation of Assertion (A).

Explanation:

The interest on drawings omitted is either shown on the credit side of Profit and Loss Adjustment Account or statement or a necessary journal entry can be passed.

![]()

Question 19.

Assertion (A): Sandhya and Manoj entered into a partnership in the profit sharing ratio 1:2. Manoj agreed to pay Sandhya if her share of profit fall short of ₹ 50,000. The profit earned was ₹ 1,77,000. Sandhya asked him to pay ₹ 27,000, but Manoj refused to pay anything.

Reason (R): Profit is guaranteed only when the minimum amount of profit is not earned by the partner.

Answer:

(A) Both Assertion (A) and Reason (R) are true, and Reason (R) is the correct explanation of Assertion (A).

Explanation:

As the profit share of Sandhya is ₹ 77,000, which is more than the guaranteed amount, so Manoj did not have to pay her.

Question 20.

Assertion (A): The profit is guaranteed only to a partner.

Reason (R): The guaranteed profit is to be paid by the other partner in the specific ratio as agreed upon to the partner who has been agreed to be paid if the profit fall short.

Answer:

(D) Assertion (A) is false, but Reason (R) is true.

Explanation:

The profit is guaranteed to a partner, few partners or even to the firm.

![]()

Question 21.

Assertion (A): Guaranteed amount is even paid when the firm suffers a loss.

Reason (R): If a partner or partners guarantees a certain amount of profit, it needs to be paid at all costs.

Answer:

(A) Both Assertion (A) and Reason (R) are true, and Reason (R) is the correct explanation of Assertion (A).

Question 22.

Assertion (A): Goodwill is an intangible asset.

Reason (R): Goodwill cannot to touched and felt.

Answer:

(A) Both Assertion (A) and Reason (R) are true, and Reason (R) is the correct explanation of Assertion (A).

Question 23.

Assertion (A): Goodwill of the firm is affected by the reputation of the firm.

Reason (R): The goodwill of the firm is dependent on the management capacity of the firm.

Answer:

(B) Both Assertion (A) and Reason (R) are true, but Reason (R) is not the correct explanation of Assertion (A).

Explanation:

Goodwill of the firm is affected by the reputation of the firm as the firm will be able to earn more profit if its reputation is good.

![]()

Case-Based MCQs

I. On the basis of following information, answer the given questions: Asif and Ravi are partners in a firm, sharing profits and losses in the ratio of 3 : 2. Their fixed capitals as on 1st April, 2016 were ₹ 6,00,000 and ₹ 4,00,000 respectively.

Their partnership deed provides for the following :

- Partners are to be allowed interest on their capital @ 10% per annum.

- They are to be charged interest on drawings @ 4% per annum.

- Asif is entitled to a salary of ₹ 2,000 per month.

- Ravi is entitled to a commission of 5% of the net profit of the firm before charging such commission.

- Asif is entitled to a rent of ₹ 3,000 per month for the use of his premises by the firm.

The net profit of the firm for the year ended 31st March, 2017, before providing for any of the above clauses was ? 4,00,000.

Both partners withdrew ₹ 5,000 at the beginning of every month for the entire year.

Question 1.

The amount of Interest on Asif’s Capital, shown in the Profit and Loss Appropriation Account is:

(A) ₹ 60,000

(B) ₹ 40,000

(C) ₹ 20,000

(D) ₹ 30,000

Answer:

(A) ₹ 60,000

Explanation:

₹ 6,00,000 X 10% = ₹ 60,000

![]()

Question 2.

How much commission is to be given to Ravi?

(A) ₹ 19,047

(B) ₹ 18,200

(C) ₹ 19,200

(D) ₹ 18,047

Answer:

(B) ₹ 18,200

Explanation:

Net Profit = ₹ 4,00,000 – ₹ 36,000 = ₹ 3,64,000

Commission = 5% of 3,64,000 = ₹ 18,200

Question 3.

How much salary is Asif entitled to the full year?

(A) ₹ 24,000

(B) ₹ 20,000

(C) ₹ 18,000

(D) ₹ 21,000

Answer:

(A) ₹ 24,000

Explanation:

Salary = ₹ 2000 x 12 = ₹ 24,000

![]()

Question 4.

How will the rent to be paid to Asif treated?

(A) It will be in the debit side of Profit and Loss Appropriation Account.

(B) It will be subtracted from the Net Profit.

(C) It will be added to the Capital Account of Asif.

(D) It will be deducted from the Capital Account of Ravi.

Answer:

(B) It will be subtracted from the Net Profit.

II. On the basis of following information, answer the given questions:

Anita, Asha and Bashir are partners sharing profits and losses in the ratio of 3 : 2 : 1 respectively. On 1st April, 2016, they decided to change their profit sharing ratio. Their partnership deed provides that in the event of any change in the profit sharing ratio, the goodwill of the firm should be valued at two years’ purchase of the average super profits for the past three years : 2015-16 Profit ₹ 40,000 2014-15 Profit ₹ 30,000 2013-14 loss 10,000 The average capital employed in the business was ₹ 1,10,000; the rate of interest expected from capital invested was 10%.

Question 1.

The total profit earned in three years is …………….

(A) ₹ 80,000

(B) ₹ 70,000

(C) ₹ 60,000

(D) None of these

Answer:

(C) ₹ 60,000

Explanation:

Total Profit = ₹ 40,000 + ₹ 30,000

₹ 10,000 = ₹ 60,000

![]()

Question 2.

The Super Profit of the firm is …………..

(A) ₹ 1o,ooo

(B) ₹ 1o,ooo

(C) ₹ 9,000

(D) ₹ 18,000

Answer:

(C) ₹ 9,000

Explanation:

Super Profit = Average Profit – Normal Profit

Normal Profit = (Capital Employed x Normal rate of return )/100

= (₹, 1o,ooo x 1o)/1oo = ₹11,ooo

Super Profit = ₹ 20,000 – ₹ 11,000

= ₹ 9,000

![]()

Question 3.

What is the amount of goodwill as calculated?

(A) ₹ 18,000

(B) ₹ 1o,ooo

(C) ₹ 7,000

(D) None of these

Answer:

(A) ₹ 18,000

Explanation:

Goodwill = ₹ 9,000 x 2 = ₹18,000

Question 4.

The normal profit earned by the firm is ………….

(A) ₹ 9,ooo

(B) ₹ 11,000

(C) ₹ 18,000

(D) ₹ 60,000

Answer:

(B) ₹ 11,000