Accounting For Not-For-Profit Organisations Class 12 MCQs Questions with Answers

NPO MCQ Class 12 Accountancy Chapter 1 Question 1.

Income and Expenditure Account records :

(A) Receipts and Payments of Revenue and Capital nature both

(B) Income and Expenditure of Revenue nature only

(C) Expenditure of Capital nature only

(D) Receipts of Revenue nature only

Answer:

(B) Income and Expenditure of Revenue nature only

Explanation:

Income and Expenditure account records the income and expenditure of only revenue nature. Capital income and expenditure are recorded in the balance sheet.

![]()

NPO MCQ Class 12 Accountancy Ch 1 Question 2.

Which of the following is not a capital receipt ?

(A) Donations for tournament

(B) Donations for building fund

(C) Life membership fee

(D) Entrance fees

Answer:

(D) Entrance fees

Explanation:

Entrance fees is a revenue receipt as it is paid by the members when they become the members.

MCQ On Non Profit Organisation Pdf Class 12 Chapter 1 Question 3.

Jaipur Club has a prize fund of ₹ 6,00,000. It incurs expenses on prizes amounting to ₹ 5,20,000. The expenses should be :

(A) debited to income and expenditure account.

(B) presented on the assets side of the balance sheet.

(C) debited to income and expenditure account and presented on the assets side of the balance sheet.

(D) deducted from the prize fund on the liabilities side of the balance sheet.

Answer:

(D) deducted from the prize fund on the liabilities side of the balance sheet.

Explanation:

The expenses incurred over the raised fund is deducted from that fund.

![]()

MCQ Of NPO Class 12 Accountancy Chapter 1 Question 4.

The following information has been extracted from the financial statements of a not-for-profit organization for the year ended 31st March, 2019 : Which of the following statements is correct for the presentation of the above items in the financial statements of the not-for-profit organization ?

(A) Negative Balance of Match fund ? 1,000 will be shown on the liabilities side of the Balance Sheet as at 31st March, 2019.?

(B) Opening Balance of Match Fund ? 5,00,000 will be shown on the liabilities side of Balance Sheet as at 1.4.2018.

(C) Negative balance of match fund ? 1,000 will be shown on the expenditure side of the Income and Expenditure Account for the year ended 31.3.2019.

(D) Both (B) and (C).

Answer:

(D) Both (B) and (C).

MCQ Of Accountancy Class 12 Chapter 1 Question 5.

Sports Star Charitable Club has income of ₹ 16,000 and ‘deficit’ debited to capital fund of ₹ 4,300 for the year 2019-20, then expenditure for 2019-20 is :

(A) ₹ 11,700

(B) ₹ 4,300

(C) ₹ 20,300

(D) None of the above

Answer:

(C) ₹ 20,300

Explanation:

The deficit of ₹ 4,300 will be added to the income of ₹ 16,000.

![]()

NPO Class 12 MCQ Accountancy Chapter 1 Question 6.

Receipts and Payments Account is a summary of:

(A) Debit and Credit balance of Ledger Account

(B) Cash Receipts and Payments

(C) Incomes and Expenses

(D) Balances of assets and liabilities

Answer:

(B) Cash Receipts and Payments

Explanation:

Receipts and Payments Account is a summary of Cash Receipts and Payments as it records all the cash transactions.

Question 7.

The nature of Receipts and Payments Account is :

(A) Nominal Account

(B) Real Account

(C) Personal Account

(D) None of the above

Answer:

(B) Real Account

Explanation:

It is an asset account since it is a summary of cash receipts and cash payments including bank balance.

![]()

Question 8.

Subscription received in advance during the current year is :

(A) An income

(B) An asset

(C) A liability

(D) None of the above

Answer:

(C) A liability

Explanation:

Any income received in advance is a liability for the firm during the current year. Subscription received in advance is considered as liability because services are yet to be rendered.

![]()

Question 9.

Donation received for special purpose is a :

(A) Liability

(B) Revenue Receipt

(C) Capital Receipt

(D) None of these

Answer:

(C) Capital Receipt

Explanation:

Donation received for specific purpose is a capital receipt as it can be used only for that specific purpose.

Question 10.

Pick the odd one out:

(A) Entrance fees

(B) Subscription

(C) Government grant

(D) Life membership fees

Answer:

(D) Life membership fees

Explanation:

Life Membership fees is the odd one as it is the only capital receipt.

![]()

Question 11.

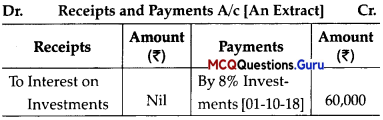

The following information below is related to an NPO :

If the firm closes its accounts on 31st March every year, what amount of accrued interest on , investments will be shown in the Balance Sheet of the firm on 31-03-19 ?

(A) ₹ 2,400

(B) ₹ 14,800

(C) ₹ 6,000

(D) None of these

Answer:

(A) ₹ 2,400

Explanation:

Accrued Interest = \(\frac {60,000 x 6 x 8}{12 x 100}\)

= c 2,400

Question 12.

Identity the type of fund stated below :

‘Himanshu Club has a fund which can only be used for the distribution of prizes.’

(A) Prize fund

(B) Endowment fund

(C) Non-approved fund

(D) Honorarium C

Answer:

(A) Prize fund

![]()

Question 13.

Pick the odd one out:

(A) Receipts and Payments A/c

(B) Income and Expenditure A/c

(C) Balance Sheet

(D) Profit and Loss A/c

Answer:

(D) Profit and Loss A/c

Explanation:

Profit and Loss A/c is odd as it is made only for the Business Entities and rest are made for the Non-profit organization.

Assertion And Reason Based MCQs

Directions: In the following questions, a statement of Assertion (A) is followed by a statement of Reason (R). Mark the correct choice as:

(A) Both Assertion (A) and Reason (R) are true, and Reason (R) is the correct explanation of Assertion (A).

(B) Both Assertion (A) and Reason (R) are true, but Reason (R) is not the correct explanation of Assertion (A).

(C) Assertion (A) is true, but Reason (R) is false .

(D) Assertion (A) is false, but Reason (R) is true.

Question 1.

Assertion (A): The Subscription received during

the year is recorded in the Receipts and Payments Account.

Reason (R): Receipts and Payments Account records all the cash transactions whether pertaining to the current year or previous year.

Answer:

(A) Both Assertion (A) and Reason (R) are true, and Reason (R) is the correct explanation of Assertion (A).

![]()

Question 2.

Assertion (A): The Income and Expenditure Account is like the cash book.

Reason (R): Income and Expenditure Account shows the surplus or deficit that is earned during the financial year by the non-profit organisation.

Answer:

(D) Assertion (A) is false, but Reason (R) is true.

Explanation:

The Income and Expenditure Account is like the Profit and loss Account of the Business or Profit Making Firms.

Question 3.

Assertion (A): The amount of subscription of ₹ 15,000 was paid out of which ₹ 3,000 is pertaining to the next year. The amount of subscription to be recorded in the Income and Expenditure Account is ₹ 15,000.

Reason (R): The Income and Expenditure Account records all the transactions that are relevant only for the current financial year.

Answer:

(D) Assertion (A) is false, but Reason (R) is true.

Explanation:

The amount of subscription to be recorded in the Income and Expenditure Account is ? 12,000. As the amount of ? 3,000 is related to the next year, and is the subscription received in advance, it will be deducted from the total amount received and the balance amount comes in the Income and Expenditure account.

![]()

Question 4.

Assertion (A): Endowment Fund is recorded only in the Balance Sheet.

Reason (R): Endowment is treated as capital receipt hence shown on the liabilities side of Balance Sheet.

Answer:

(A) Both Assertion (A) and Reason (R) are true, and Reason (R) is the correct explanation of Assertion (A).

Case-Based Mcqs

I. Read the following information and answer the questions that follow:

Dr. Rajani Mehta a qualified M.B.B.S. doctor got voluntary retirement at the age of 50 years from a renowned hospital. She was residing in a flat of a wide apartment which is surrounded by a slum which is inhabited by economically weaker strata of the society. As the people in that area were not aware about importance of health care, a widespread ailment had been persistently prevailing.

Rajani met with some of the well-off people of apartment and decided to open a dispensary named as ‘LOCAL Clinic’ to provide them cost free medical assistance and make them aware about hygienic living, physical fitness, and economic balance diet. Many of the apartment members agreed to it. She approached health department of the town with her proposal which was accepted and an initial one time grant of ₹ 2,00,000 was sanctioned immediately for purchase of medical equipment and test kits for pathological tests. 10 members of the apartment contributed ₹ 20,000 each as lifetime subscription to the clinic. Rajni decided to charge ₹ 10 as one

time registration fee from patients. Apart from above Rajni made following transactions for first year:

Marble’s popularity began in ancient Rome and Greece, where white and off-white marble were used to construct a variety of structures, from hand?held sculptures to massive pillars and buildings.

| S. No. | Particulars | Amount ₹ |

| 1. | Purchased Equipment | 1,20,000 |

| 2. | Purchased Medicines | 95,000 |

| 3. | Purchased Furniture | 10,000 |

| 4. | Rent paid | 12,000 |

| 5. | Fee received for medical tests | 45,000 |

| 6. | Honorarium paid to Yoga teacher | 35,000 |

| 7. | Honorarium paid to physiotherapist and sports teacher | 38,000 |

![]()

Question 1.

Not for profit organization prepares:

(i) Income and Expenditure account

(ii) Trading and Profit loss account

(iii) Receipt and Payment account

(iv) None of the above

(A) Only (ii)

(B) Only (iii)

(C) Both (i) and (ii)

(D) Both (i) and (iii)

Answer:

(C) Both (i) and (ii)

Explanation:

Final Accounts prepared by Not- for-Profit Organisation:

- Receipts and Payments Account

- Income and Expenditure Account

- Balance Sheet

![]()

Question 2.

Honorarium paid to Physiotherapist and sports teacher will be posted to:

(A) Debit side of Income and Expenditure Account.

(B) Debit side of Receipt and Payment Account.

(C) Debit side of Profit and Loss Account.

(D) Credit side of Income and Expenditure account.

Answer:

(A) Debit side of Income and Expenditure Account.

Explanation:

The honorarium is a voluntary payment given to a person for the services rendered by him to the organization. Any amount paid to someone as honorarium is treated as revenue expenditure and is debited to Income and Expenditure Account for the period concerned.

Question 3.

“Donations received by Ms Rajani Mehta from health department should be capitalized.” Consider the statement and chose the correct options:

(A) The statement is true.

(B) The Statement is false

(C) The Statement is partially true.

(D) The statement is incomplete.

Answer:

(A) The statement is true.

Explanation:

Donations for specific purposes should always be capitalized. In the above case, donation was given for purchase of medical equipment and test kits for pathological tests.

![]()

Question 4.

Lifetime subscription paid by 10 members will be posted in:

(A) Expenditure side of Income and Expenditure Account

(B) Liability side of closing Balance Sheet

(C) Income side of Income and Expenditure Account

(D) Assets side of closing Balance Sheet

Answer:

(B) Liability side of closing Balance Sheet

Explanation:

Life membership is the long?term or non-recurring income of Not-for-Profit organisation, so it will be shown as a liability side of Balance Sheet.

II. Read the following information and answer the questions that follow:

Talent sports Club is engaged in the activity of identifying and promoting sports talent from rural and tribal areas of the country. Identifying with this Noble cause Mr. Manohar, a renowned industrialist donated ₹ 50,00,000 on 1st July, 2020, for the construction of a new hostel and mess for upcoming sportsmen.

Besides this, Mr. Manohar offered the services of his personal chartered accountant, free of charge, to streamline the account of Total Sports Club. The chartered accountant visited the office of the NPO on 31st March, 2021 and found that till date ₹ 35,00,000 had been spent on construction of hostel and mess building. He also noted that the NPO had a capital fund of ₹ 1,20,00,000 in the beginning of the year. Other important points that he noted were that NPO had 2000 regular members each having an annual subscription of ₹ 2,000 per annum.

![]()

On 1st April, 2020, 180 members had not paid for subscription of previous year and 20 members had paid for 2020-2021 in advance (out of which 5 had paid advance of 2021- 2022 as well). 31st March, 2021,110 members he had outstanding balance (including 50 who had not paid for 2019-20 as well) and 25 members had paid for 2021- 2022 in advance (including all 5 who had paid in advance in 2019-20).

Since the accountant of NPO was not clear about how to deal with all the above information he drafted a set of questions for guidance. Considering that you are the Chartered Accountant of Mr. Manohar answer the following questions based on the information detailed above.

Question 1.

The amount of ₹ 50,00,000 received from Mr. Manohar towards building and mess should be transferred to:

(A) Capital fund

(B) General fund

(C) Income and Expenditure account

(D) Building fund

Answer:

(A) Capital fund

Explanation:

If an organisation has established a fund for a specific purpose or has received donation for specific purpose, it is credited to a separate Fund Account.

![]()

Question 2.

The amount of ₹ 35,00,000 spent on construction of building should be:

(i) reflected on debit side of income and expenditure account as an expense.

(ii) reflected on asset side of balance sheet.

(iii) reflected as a deduction from Building fund and addition to capital fund.

(iv) not be recorded till the building is complete. On basis of given information choose which of the following stands true?

(A) Only (iv)

(B) Both (i) and (iv)

(C) Both (ii) and (iii)

(D) None of the above

Answer:

(C) Both (ii) and (iii)

Explanation:

1. Expenses related to specific funds are first adjusted from available fund.

2. If any Investment or Capital expenditure is made out of this fund then such Investment is shown on the Assets side of Balance Sheet. On the other hand, as such investments increases the overall capital base of the organisation so these are added to the Capital Fund.

![]()

Question 3.

The amount of subscription in arrears on 1st April, 2020 is:

(A) ₹ 3,60,000

(B) ₹ 3,00,000

(C) ₹ 2,000

(D) ₹ 1,80,000

Answer:

(A) ₹ 3,60,000

Explanation:

Subscription in arrears

= 180 x ₹ 2,000

= ₹ 3,60,000

Question 4.

The amount of subscription in arrears on 31st March, 2021 is:

(A) ₹ 2,20,000

(B) ₹ 3,60,000

(C) ₹ 3,20,000

(D) ₹ 1,80,000

Answer:

(C) ₹ 3,20,000

Explanation:

Subscription in arrears

= 110 x ₹ 2000 + 50 x ₹ 2000

= ₹ 2,20,000 + ₹ 1,00,000

= ₹ 3,20,000

![]()

III. Read the following information and answer the questions that follow:

VIJAYA SHANKAR, an Ex-Indian cricketer decided to start a cricket academy to train the young enthusiastic players of down south. With the support and guidance of his family he started the Star cricket academy at Tirunelveli township area on 1st April, 2020. Land was donated by his grandfather worth ₹ 10,00,000 as per his will for cricket coaching. His father Shankar donated ₹ 5,00,000 for the construction and running the academy.

He spent ₹ 3,00,000 for construction of the pavilion. 200 players of Tirunelveli joined the academy and they paid yearly subscription of ₹ 1200 each. 10 players paid in advance for the next year 2021-22. Vijaya shankar appointed well experienced coach for them, the coach fee amounted to ₹ 1,20,000 p.a. The maintenance expenses amounted to ₹ 75,000. Bats and balls purchased during the year amounted to ₹ 15,000. Closing stock of bats and ball amount to ₹ 1000.

Question 1.

What is the Primary source of income for the academy?

(A) Subscription

(B) Fund

(C) Donation

(D) All of the above

Answer:

(A) Subscription

Explanation:

Subscription is the amount paid by the members periodically so that their membership remains alive.

![]()

Question 2.

The amount of subscription to be credited to income and expenditure account

(A) ₹ 2,00,000

(B) ₹ 1,40,000

(C) ₹ 2,40,000

(D) ₹ 3,00,000

Answer:

(C) ₹ 2,40,000

Explanation:

Amount of subscription to be credited to Income and Expenditure Account = ₹ 200 x ₹ 1200 = ₹ 2,40,000

![]()

Question 3.

How will you treat the land donated by his grandfather?

(A) To be treated as legacy and is to be capitalized.

(B) To be treated as donation and is debited to Income and Expenditure Account

(C) To be treated as legacy and shown in the assets side.

(D) To be treated as legacy and is credited to Income and Expenditure Account?

Answer:

(A) To be treated as legacy and is to be capitalized.

Question 4.

The liability towards advance subscription amounted to:

(A) ₹ 12,000

(B) ₹ 24,000

(C) ₹ 1,200

(D) ₹ 1,20,000

Answer:

(A) ₹ 12,000

Explanation:

Advance Subscription:

10 x ₹ 1200 = ₹ 12,000