Here we are providing Class 12 Business Studies Important Extra Questions and Answers Chapter 5 Organising. Business Studies Class 12 Important Questions are the best resource for students which helps in class 12 board exams.

Class 12 Business Studies Chapter 5 Important Extra Questions Organising

Organising Important Extra Questions Short Answer Type

Question 1.

Explain the term organization structure in brief.

Answer:

Organization structure: The organization structure can be defined as the framework within which managerial and operating tasks are performed. It specifies the relationships between people, work, and resources. It allows coordination among human, physical and financial resource to accomplish the desired goals.

An organization structure provides the framework which enables the enterprise to function as an integrated unit by regulating and coordinating the responsibilities of individuals and departments.

According to Peter Drucker, the Organization structure is an indispensable means, and the wrong structure wins seriously impair business performance and even destroy it.

The organization structure can be categorized as –

- Functional structure

- Divisional structure.

Question 2.

Explain the terms authority, responsibility, and accountability?

Answer:

Meaning and definition of Authority: Management is getting work done through others. This is not possible unless the managers get the adequate authority to get work done through others. No manager can get work successfully executed through his subordinates in the absence of suitable authority. Authority refers to the right to make decisions and to get the decisions carried out. It is the right to act.

In the field of management, authority means the right to give orders to the subordinates and the power to get them executed for the attainment of organizational goals. Various scholars have defined authority in the following different ways

According to Henry Fayol, “Authority is the right to give orders and the power the exact obedience.”

According to George R. Terry, “Authority is the power to exact other to take actions considered appropriate for the achievement of predetermined objectives.”

According to Herbert A. Simon, “Authority may be defined as the power to make decisions which guide the actions of another. It is a relationship between two individuals, one superior; the other subordinate. The superior frames and transmits decisions with the expectation that these will be accepted by the subordinate. The subordinate executes such decisions and his conduct is determined by them.”

Responsibility: According to Theo Hamman, “Responsibility is the obligation of the subordinate to perform the duty as required by his superior.”

According to Davis, “Responsibility is an obligation of the individuals to perform assigned duties to the best of his ability under the direction of his executive.”

Thus, responsibility is the obligation of an individual to perform a particular work that arises from the formal relationship of a superior and a subordinate in an organization.

Accountability: When an individual works under some other person, he also becomes answerable to such officer for the proper discharge of his responsibilities. A superior can requisite an account of results from his subordinate of the duties assigned to him. The subordinate has a responsibility to give information and render a report of the task performed by him. Such responsibility is known as accountability.

According to Davis and Filley, “Each member in the organization is obliged to report to his superior how well he has exercised responsibility and made use of authority delegated to him.”

Thus, it is clear that accountability arises out of responsibility and goes hand in hand with it.

Question 3.

Explain in brief the principles of delegation of authority?

Answer:

Delegation is an important instrument in the process of organization and management, requires a few precautions and principles to be followed on the part of the delegator and the delegatee. Some principles are as follows

1. Principle of Parity of Authority and Responsibility:

When somebody is assigned any task, he must also be given adequate authority to perform such a task. For example, if a sales manager is assigned the task of doubling the sales, he must also be given the authority of advertising, appointing salesmen, selecting the channel of distribution, deciding the discount on sales, and incurring selling expenses. The parity of authority and responsibility does not mean that if sales are to be doubled, the selling expenses should be commensurate with the responsibility. If the authority is more than responsible, it shall lead to its misuse.

2. Responsibilities cannot be delegated:

No superior can evade his responsibilities simply by delegating his authority to subordinates. The ultimate responsibility lies with the superior who delegates the authority. The flow of responsibility is from bottom to top, thus after delegating authority superior remains accountable for the activities of his subordinates towards his own superiors. Similarly, the subordinates remain accountable to their superiors for the performance of assigned duties.

3. Principle of Clarity of Authority and Responsibilities:

It is a very important concept in the area of delegation. The subordinates should be well clear about their rights and responsibilities. It will help them in knowing their area of operation and the extent of freedom of action. So, that there shall arise no conflict between different persons.

4. Principle of the standard of performance:

A subordinate can be self-responsible for failure only when certain standards are established for measuring his performance and such standards are made clear to the subordinates while assigning the work. The subordinate should be well aware of what is expected of him and what type of results should be shown. A delegation without control is like a wild horse without reins. Determination of the standards of performance helps the subordinate in being alert and prudent towards his responsibilities.

5. Principle of Unity of Command:

According to Earnest Dale, every individual should receive orders from only one individual and he should be responsible only towards him. If an employee receives orders from many individuals then he shall get confused about whose orders to obey and whom to report to. A person with more than one boss is like a pawn in a game of chess.

6. Authority level principle:

This principle implies that a subordinate should have complete authority to make decisions at his level or position. If the subordinate has to take the approval of his superior even for small matters then his performance shall be hampered. This is also known as the exception principle.

7. Scalar principle:

According to this principle, authority and responsibility should; move in a straight line from the superior to the subordinate. This principle should be well considered while resorting to the delegation. For example, if there are four persons A, B, C, and D in a straight line and ‘ if A wants to delegate to C or D, he cannot do so. As per the principle of Scalar chain, A will first have to delegate to B, who in turn will delegate to C and then C will delegate to D. If a superior delegates some work to the subordinate next to the most immediate one then the immediate subordinates shall have an inferiority complex and will not cooperate fully.

8. Principle of completeness of Delegation:

Once a decision is taken as to which tasks are to be assigned, it is important that an individual should be assigned an entire task. There should be ho splits i.e., the responsibility for the same task should not be assigned to more than one individual. Otherwise, there will be confusion of authority and responsibility.

Question 4.

Differentiate between Formal organization and Informal organization?

Answer:

| Basis | Delegation of authority | Decentralization |

| 1. Nature | It is the first step towards decentralization | Decentralization is the last step in the process of delegation. It includes delegation. |

| 2. Freedom to make decisions | Under delegation, subordinates have to follow the directions given by their superiors while making decisions. | Under decentralization, subordinates are free to take decisions |

| 3. Scope | Its scope is limited since it refers to entrusting some part of the authority by the superior to his nearest subordinate on a personal basis. | Its scope is wide since it refers to the wide dispersal of authority to all levels in the entire organization. |

| 4. Routine or important | It is considered to be the routine task of managers. | It is considered to be the very important decision of organizational arrangement. |

| 5. Transfer of Responsibility | Under it, only the authority is transferred and not the responsibility. The ultimate responsibility lies with the delegator. | Under it, authority, as well as responsibility, is transferred. Subordinates are independently responsible for their performance. |

| 6. Power to Control | In it superior has the power to exercise control over his subordinates. | In it superior losses the power to control his subordinates. |

| 7. Temporary or permanent | It is a temporary arrangement where the authority is taken back after the assigned task is completed. | It is a permanent feature where the authority is granted for the future also. |

| 8. Essential or optional | It is essential for all types of organizations because no superior can get the things done from his’ subordinates without delegating sufficient authority to them. | It is optional because it is not necessary’ that the superior must disperse his authority in a systematic manner throughout the entire organization. |

| 9. Dependence | Decentralization is not essential for delegation i.e. delegation does not depend on decentralization | Delegation is essential for decentralization, i.e. it depends on delegation. |

Question 5.

Differentiate between a delegation of authority and Decentralization?

Answer:

The distinction between Decentralisation and Delegation of authority. Though decentralization is the expanded form of delegation, there is a considerable difference in them. Decentralization is much more than delegation. Louis A. Allen says, when a person hands over his work to others it is known as delegation but it will be known as decentralization only when the authority to complete the entire work is handed over to them.

For example, when the chief executive of a company hands over the responsibility to make appointments in h:s department to a particular manager, it is known as delegation. But when all the departmental managers are given authority to make appointments in their respective departments, it is known as decentralization. The extent of decentralization increases when the departmental managers extend this authority to the executives below them:

The distinction between Delegation of authority and Decentralisation. Delegation of authority

| Basis | Formal organization | Informal organizations |

| (1) Formation | It is formed by the top management in a thoughtful and organized way. | It is formed automatically due to the social relationship. |

| (2) Purpose | Its main purpose is the achievement of the objectives of the organization eff’içieñtly. | Its main purpose is the fulfillment of individual needs and to protect their mutual interests. |

| (3) Nature or Structure | The activities, rights, and responsibilities are clearly defined in suçh organizations. | The rules are neither written nor clearly defined. |

| (4) Authority | In such an organization authority ¡s derived from assigned positions and from above. | In this authority is derived from the acceptance and capabilities of an individual. |

| (5) Flow of authority or Communication | This authority flows from top to bottom. | This authority flows from top to bottom or horizontally. |

| (6) Behaviour of Members | In this organization, the relation among employees is according to the position and functions. Thus, the behavior is highly formal. | In this organization, there exists a personal relationship among members. Thus the behavior among them is informal. |

| (7) Tenure | Due to the establishment of the organization on some logical planning, the tenure is relatively | Since it is based on personal and mutual relationships it is highly flexible and temporary. |

| (8) Use of organization charts | In this, an organization chart is prepared to present the position of authority and responsibility. | No organization chat is prepared |

| (9) Size | They can be huge in size. | They are mainly small in size. |

Question 6.

Explain in brief the matrix or Grid organization? Also, mention its merits and demerits.

Answer:

Matrix or Grid organization:

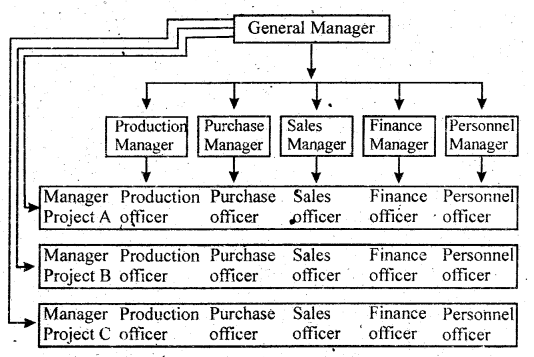

When the size and operational field of any organization are too wide and the number of products produced by it and its number of customers is large, it cannot be divided on any of the bases mentioned above. In such a situation, a matrix organization is established. Such organizations are divided on the basis of functions like the production department, purchase department, sales department, finance department, personnel department, etc. Besides this, a separate Project Manager is appointed for different projects.

This is explained through the diagram given below –

From the above diagram, it is clear that a separate Project Manager is appointed to complete the project quickly like Project A, Project B, Project C, etc. The project manager is given full responsibility for that particular project and all the other departmental; officers are instructed to co-operate with him. Project Managers make plans for the project and undertake all the functions of organizing, control, direction, etc. The project manager is responsible for the success or failure of the project. The middle level and lower level officers work under the control of the project manager until the completion. of the project and get involved in their normal activities after the completion of the project.

Thus in a matrix organization, two types of organizational structures work together – Functional and Project. Project managers do not wholly use the services of middle level and lower level officers but make use of their services temporarily according to their needs.

Advantages of Matrix Organisation:

- Quick Completion of the Project: The project manager makes plans for all the activities of the project like giving orders, direction, etc. Thus the project gets completed quickly.

- Advantages of Functional as well as project departmentation: Advantages of two types of organization-functional and project, can be availed of Project managers are the experts in their own field and they have the full co-operation of other officers.

- Flexibility: Such type of organization is flexible as it can be easily implemented without bringing many changes in the existing organizational structure.

- The economy in costs: There is no need of appointing special staff for each project. Services of departmental officers can be utilized as and when needed by the project manager which leads to economy in costs.

Disadvantages of Matrix organization:

- Violation of the Principle of Unity of Command: The principle of unity of command is not followed because the officers are responsible to their superior as well as to the project manager. Thus they have to follow more than one boss.

- The problem of coordination: There is a problem of coordination between the functions of departmental officers and project managers. There arises a conflict between the functions of the two because departmental officers give priority to the activities of their own department whereas project managers give priority to their project work.

- Lack of Fixation of Responsibility: On non-completion of the project, in time, the project managers normally complain of non-cooperation of the departmental officers.

- The problem of communication: The problem of internal communication arises.

Organising Important Extra Questions Long Answer Type

Question 1.

Explain the term Decentralization and mention its importance in business activities?

Answer:

Decentralization:

Decentralisation of authority means systematic dispersal of authority in all departments and at all levels of management. According to Louis Allen decentralization is “the systematic effort to delegate to the lowest levels all authority, except that which can be exercised at central points”. An organization is said to be decentralized when managers at middle and lower levels are given the authority to make decisions and actions on matters relating to their respective areas of work. The top management retains the authority for taking major decisions and formulating policies for the organization as a whole. Top management also retains authority for overall coordination and control of the organization.

For example, let us take the case of a large steel manufacturing company. The board of directors and managing director of the company lay down the overall objectives and policies of the enterprise. Major decisions on product lines, capital investment, marketing methods are taken by the respective heads of departments. The marketing manager, for instance, is authorized to decide the quality and prices of products, channels of distribution, advertising methods, and organizing sales campaigns. The top management of the company does not interfere with his authority. However, departmental managers are required to keep in view the overall policies of the company while making decisions on matters within their authority. This is how a decentralized organization works.

Centralization and decentralization are opposite terms. They should not be confused with the location of work. An organization having ‘ branches in different cities may be centralized. Similarly, a company; maybe decentralized even though all its offices are located in one budding. Centralization and decentralization are relative terms. No organization can be completely centralized or completely decentralized. They exist together.

For example, even in a decentralized organization, the top management retains the authority for-overall policy decisions to ensure coordination and control. The degree of centralization and decentralization differs from one organization to another. According to Henri Fayol, “Everything which goes to increase the subordinates. the role is decentralization; everything which goes to decrease it is centralization.”

Importance of Decentralisation:

The main benefits of decentralization are as follows –

1. Reduction in Burden of Top Executives: Decentralisation helps to reduce the workload of top executives.

They can devote greater time and attention to important policy matters by decentralizing authority for routine operational decisions.

2. Motivation of subordinates: Decentralisation helps to improve the job satisfaction and morale of lower-level managers by satisfying their needs for independence, participation, and status. It also fosters team-spirit and group cohesiveness among the subordinates.

3. Better Decisions: Under decentralization, the authority to make decisions is placed in the hands of those who are responsible for executing the decisions, as a result, more accurate and faster decisions can be taken as the subordinates are well aware of the realities of the situation. This avoids red-tapism and delays.

4. Growth and Diversification: Decentralisation facilitates the growth and diversification of the enterprise. Each product division is given sufficient autonomy for innovations and creativity. The top management can extend leadership over a giant enterprise. A sense of competition can be created among different divisions or departments.

5. Development of managers: When authority is decentralized, subordinates get the opportunity of exercising their own judgment. They learn how to decide and develop managerial skills. As a result, the problem of succession is overcome and the continuity and growth of the organization are ensured. There is a better utilization of lower-level executives.

6. Effective communication: Under decentralization, the span of an organization is wider and there are fewer levels of an organization. Therefore, the communication system becomes more effective. Intimate relationships between superiors and subordinates can be developed.

7. Efficient supervision and control: Managers at lower levels have adequate authority to make changes in work assignments, rechange production-schedules, recommend supervision, and take disciplinary actions. Therefore, more effective supervision can be exercised. Control can JiS-Jnade effective by evaluating the performance of each decentralized unit in the light of clear and predetermined standards. Decentralization permits management by objectives and self-control.

8. Democratic Management: Decentralisation of authority distributes decision making authority at all levels and in all departments. Therefore, it creates democracy in the management of an organization. People at all levels are involved in decision making.

Decentralization, may, however, create problems of coordination and control. It is costly to set up semiautonomous departments and divisions. Lack of competent managers at middle and lower levels hinders decentralization. The degree of decentralization varies from one organization to another. It may also change from one time period to another in the same organization.

Question 2.

Give the meaning of delegation of authority and its importance?

Answer:

Meaning of Delegation of Authority:

Delegation of authority takes place when a manager assigns a .part of his work to others and gives them the authority to perform the assigned tasks. The manager who delegates authority holds his subordinates responsible for the proper performance of the assigned tasks. Thus, the process of delegation involves assigning duties, entrusting authority, and imposing responsibility on subordinates.

Some popular definitions of the delegation are given below –

- Delegation of authority merely means granting of authority to subordinates to operate within prescribed limits. Theo Haimann

- Authority is delegated when enterprise discretion is vested in a subordinate by a superior. The entire process of delegation involves the determination of results expected, assignment of tasks, transfer of authority for the accomplishment of these tasks, and the exaction of responsibility for their accomplishment. – Koontz and O’ Donnell.

Importance of Delegation:

When the size of an organization expands, a manager alone cannot do all the work himself. He has to share his work and authority with others. An executive can extend his personal capacity through delegation of authority. Delegation is the means by which a manager can get results through others. Failure to delegate reduces the efficiency of the individual and blocks the development of his juniors. How one delegate determines how one manages. Just as authority is the key to the manager’s job, delegation is the key to the organization.

The main advantages of the delegation are as follows –

1. Relief to Top Executives: Delegation of authority enables a manager to share his workload with his subordinates. It reduces the burden of work on senior executives. By transferring routine work to subordinates, a manager can concentrate on important policy matters. He can, therefore, make better use of his valuable time and ability. Delegation facilitates the proper distribution of workload as it takes place at all levels. The manager who delegates authority can achieve greater results than the one who does not. This is because by delegating authority, a manager secures the cooperation and participation of his subordinates.

2. Scalar Chain: Delegation of authority creates a chain of superior-subordinate relationships among managers. It provides meaning and content to managerial jobs. It also directs and regulates the flow of authority from the top to the bottom of an organization. It serves as a basis of superior-subordinate relations.

3. Specialization: Through delegation, an executive can assign jobs to his subordinates according to abilities and experience. In this way, he can obtain the benefits of the division of work.

4. Quick Decisions: When authority is delegated, lower-level employees can take decisions quickly without consulting senior executives. Subordinates are better in touch with local conditions and can take more practicable decisions within the policy framework laid down by top management.

5. Motivation: Delegation provides a feeling of status and importance to subordinates. Their independence and job satisfaction increase due to the authority they enjoy. They become more willing to work hard and achieve the targets laid down by higher authorities. Thus, delegation promotes a sense of initiative and responsibility among employees. It inspires employees to make full use of their skills.

6. Executive Development: Delegation gives an opportunity to employees to learn decision-making and leadership skills by exercising authority. It helps to improve the quality of personnel at lower levels because they are required to handle situations and solve managerial problems. They acquire competence and problems and can take up higher responsibilities in course of time. In this way, the delegation of authority is a means of developing future managers.

7. Growth and Diversification: Delegation of authority facilitates expansion and growth of the organization. As the quality of managerial talent improves, the organization can face future challenges better. It can grow and expand to a bigger size.