Here we are providing Class 12 Business Studies Important Extra Questions and Answers Chapter 9 Financial Management. Business Studies Class 12 Important Questions are the best resource for students which helps in class 12 board exams.

Class 12 Business Studies Chapter 9 Important Extra Questions Financial Management

Financial Management Important Extra Questions Short Answer Type

Question 1.

What are the various factors affecting Financial Planning?

Answer:

A financial plan should be prepared very carefully because it has a long-term impact on the working of an enterprise. A financial plan is affected by a number of factors. All these factors should be’ taken into consideration while preparing a financial plan.

1. Nature of Business: The nature of business plays a decisive role in formulating a financial plan. A manufacturing business requires more amount of long-term funds than a trading business. In addition to it, the factors such as stability and regularity of income, future prospects of growth, seasonal fluctuations, assets structure, etc. affect the financial requirements as well as sources of finance.

2. Degree of Risk: The risk involved in the business also plays an important role while planning the sources of finance. A firm whose sales and earnings are subject to wide fluctuations runs the risk of not being able to meet the required payments in respect of interest and repayment of loans. Clearly, such firms should use more amount of their own funds and rely less on debt. On the other hand, the enterprises with stable sales and earnings can employ more amount of debts and hence can take the advantage of trading on equity.

3. Standing of the concern: Credit standing of concern among investors affects financial planning to a great extent. The credit standing of concern is determined by a number of factors such as the age of the firm, its past performance, size, market area, the reputation of management, etc.

4. Plans for future Growth: The plans for growth and expansion of the firm in near future are considered while formulating a financial plan. The financial plan should be developed in such a way as to facilitate required funds without much difficultly.

5. Alternative Sources of Finance: Since finance can be procured from a number of sources, the pros and cons of all the sources should be properly considered while choosing the proper sources of finance. The sources should be able to provide adequate funds to meet the requirements of the business.

6. Attitude of Management: The attitude of management towards risk and control of the business affects financial planning to a great extent. If the management is of risk-taking nature, it would employ more amount of borrowed funds. On the contrary, if it is of conservative nature it will employ more amount of equity capital. From the control point of view, if the management desires to keep full control of the enterprise, it will not issue fresh equity shares so that the new shareholders may not control the enterprises.

7. Government Policies and Control: The financial plan of a company is affected by the rules and regulations framed by the Government stock exchanges and financial institutions from time to time. The terms of issue of shares and debentures, interest rates, dividend payments, etc. are governed by the rules framed by the government periodically. Permission of the Securities and Stock Exchange Board of India (SEBI) is also required for the issue of shares and debentures.

8. Changes in Technology, Consumer Tastes, and Competitive Factors: Rapid innovations are taking place in every field nowadays. A financial plan is adequately affected by changes in technology, consumer preferences, degree of competition, and general economic conditions.

Question 2.

Explain in brief the various steps in financial planning.

Answer:

Following steps should be taken for preparing a financial plan:

1. Determination of Financial Objectives: For the purpose of preparing an effective financial plan first of all the financial objectives of a firm should be clearly determined. The financial objectives should be divided into short-term objectives as well as long-term objectives. The short-term objectives may include maintaining the liquidity of funds, maintaining the market standing of the firm and proper maintenance of sales, etc.

On the other hand, the long-term objectives may include the achievement of maximum efficiency of factors of production at minimum cost and the maximization of shareholder’s wealth. The objectives should be clearly defined so that they can be used as guidelines for determining the 1 policies and procedures.

2. Formulation of Financial Policies: The second step in financial planning is the formulation of financial policies. Financial policies act as guidelines for the f procurement, allocation, and effective utilization of funds of the organization. Financial policies are framed by the top management with the advice of the financial manager. The policies may be regarding capitalization, capital structure, trading on equity, fixed assets management, working capital management, dividend distribution, etc.

3. Formulation of Procedures: The policies laid down must be clarified in the form of detailed procedures. Each subordinate must know what he is required to do. Procedures are essential to ensure the consistency of actions. In financial procedures, financial executives decide about the control system, establish the standards of performance and compare the actual performance with the standards to ascertain the deviations and their causes. Thereafter, necessary steps are taken to control the deviations.

4. Provision of Flexibility: The objectives, policies, and procedures laid down as above constitute the financial plan of a business. Financial planning is a continuous process and hence there should be proper flexibility in the financial objectives, policies, and procedures so that these may be revised or thoroughly overhauled according to the changing circumstances.

Question 3.

Explain the major characteristics or Principles of a sound financial plan.

Answer:

An ideal financial plan must be based on the principles or qualities mentioned below:

1. Simplicity: Financial plan should be so simple that it may be easily understood by everyone. It should have a simple capital structure capable of being managed easily. The type of securities issued should be kept at a minimum because various types of securities will create unnecessary suspicion in the minds of investors.

2. Foresight: The financial plan should be prepared to keep in view the future needs of the business. It should take into consideration the future demand of the company’s products, the future scale of operations, technological innovations, and various other changes. A financial plan should be able to meet the future requirements of fixed as well as working capital.

3. Optimum use of Funds: An ideal financial plan should always aim at the best possible and intensive use of all available resources of finance. The business should neither be starved of funds nor it should have a surplus or idle funds. Unnecessary idle funds are as bad as inadequate funds. A proper balance should also be kept between the short-term and long-term funds of the business.

4. Flexibility: A financial plan should be sufficiently flexible. It should be possible for a company to change its financial plan with minimum cost and delay if warranted by changed circumstances. The company should be able to substitute one form of financing for another to economize the use of funds. The financial plan should allow a scope for adjustments as and when a new situation arises like recession, boom, etc. A rigid financial plan can easily become a burden rather than a 1 technique of financial management.

5. Liquidity: Liquidity is the ability of the enterprise to pay off its day-to-day expenses and other short-term liabilities on time. The financial plan should provide sufficient liquidity of funds as it will ensure the creditworthiness and goodwill of the enterprise. Adequate liquidity in the \ financial plan increases its flexibility also.

6. Economical: Financial plan must be prepared in such a way that the cost of capital is minimum. The average cost of capital will be minimum when a fair 1 balance is maintained between debt funds and owned capital. Also, the financial plan should involve minimum expenses on the issue of capital such as underwriting Commission, brokerage, etc.

7. Contingencies: A financial plan should keep-in view the requirement of funds for contingencies. Contingencies mean the requirement of funds for unseen: events.

8. Adequate system of Control: A financial plan should establish and maintain a proper system of financial control.

9. Suitable to the Organisation structure: A financial plan should be in accordance with the size and organizational structure of the firm.

Question 4.

Define the nature and types of working capital.

Answer:

Along with the fixed capital, almost every business requires working capital though the extent of working capital requirement differs in different businesses. Working capital is needed for running the day-to-day business activities. When a business is started, working capital is needed for purchasing raw materials. The raw’ material is then converted into finished goods by incurring some additional costs on it.

Now goods are sold. Sales do not convert into cash instantly because there is invariably some credit sales. Thus, there exists a time, lag between sales of goods and receipt of cash. During this period, expenses are to be incurred for continuing the* business operations.

For this purpose working capital is needed, Therefore, sufficient working capital is needed which shall be involved from the purchase of raw materials to the realization of cash.

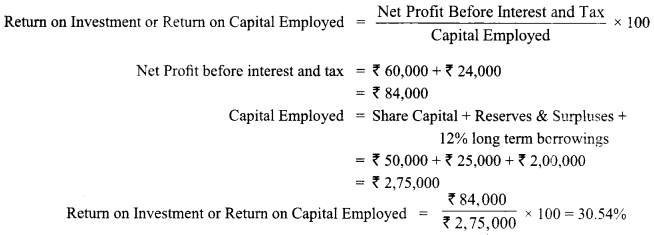

The time period which is required to convert raw materials into finished goods and then into cash is known as the operation cycle or cash cycle. The need for working capital can also be explained with the help of the operating cycle.

The operating cycle of a manufacturing concern involves five phases:

- Conversion of cash into raw material

- Conversion of raw material into work-in-progress

- Conversion of work-in-progress into finished goods

- Conversion of finished goods into debtors by credit sales

- Conversion of debtors into cash by realizing cash from them.

Thus the operating cycle starts from cash, finishes at cash, and then again restarts from cash. The need for working capital depends upon the period of the operation cycle. Greater the period, more will be the need for working capital. The period of operation cycle in a manufacturing concern is greater than a period of operating cycle in a trading concern because in trading units cash is directly converted into finished goods.

Diagram: Operating Cycle (Nature of Working Capital)

Because of the time involved in an operating cycle, there is a need, for working capital in the form of current assets. Firms have to keep I adequate stock of raw materials to avoid the risk of non-availability of raw materials. Similarly, the concern must have adequate stock of finished goods to meet the demand in the market on a continuous basis and to avoid being out of stock. Concern also has to sell finished goods on credit due to competition which necessitates the money tied up in debtors. Y and bills receivables. In addition to all these, concerns have to necessarily keep cash to pay the manufacturing expenses, etc., and to meet the contingencies.

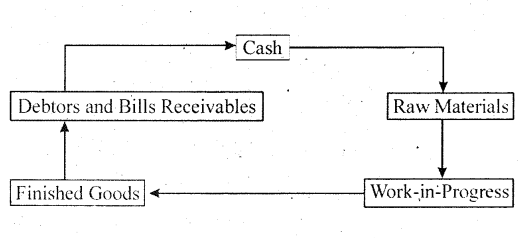

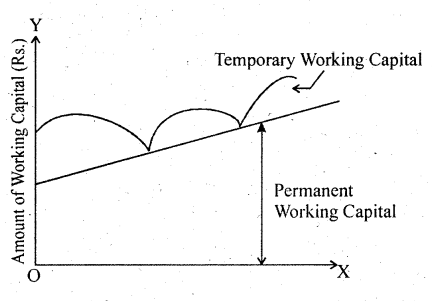

Permanent and Temporary Working Capital Working Capital in a business is needed because of the operating cycle.

But the need for working capital does not .come to an end after the cycle is completed. Since the operating cycle is a continuous process, there remains a need for a continuous supply of working capital. However, the amount of working capital required is not constant. throughout the year, but keeps fluctuating.

On the basis of this concept, working capital is classified into two types:

(a) Permanent Working Capital: The need for working capital or current assets fluctuates from time to time. However, to carry on day-to-day operations of the business without any obstacles, a certain minimum level of raw- materials, work-in-progress, finished goods and cash must be maintained on a continuous basis. The amount needed to maintain current assets on this minimum level is called permanent or regular working capital. The amount involved as permanent working capital has to be met from long-term sources of finance, e.g., capital, debentures, long-terms loans, etc.

(b) Temporary or Variable Working Capital: Any amount over and above the permanent level of working capital is called temporary, fluctuating, or variable working capital. Due to seasonal changes, the level of business activities higher than normal during some months of the year, and therefore, additional working capital will be required along with the permanent working capital. It is so because during peak season, demand rises and more stock is to be maintained to meet the demand.

Similarly, the amount of debtors increases due to excessive sales. Additional working capital thus needed is known as temporary working capital because once the season is over, the additional demand will be no more.’The need for temporary working capital should be met from short-term sources of finance, e.g. short-terms loans, etc. So that it can be refunded when it is not required.

Both types of working capital are necessary to run the business smoothly. The distinction between permanent and temporary working capital is illustrated in the following diagram:

Diagram: Showing Permanent and Temporary Working Capital.

The above diagram shows that permanent working capital remains the same throughout the year, while temporary working capital is fluctuating in accordance with seasonal demand.

However, in case of an expanding concern, the need for permanent working capital may not be constant and it would be increasing.

Therefore, the permanent working capital line also may not be horizontal and it will go on rising as illustrated in the following diagram:

Diagram: Showing Permanent and Temporary Working Capital in a Growing Concern

Question 5.

Define the term ‘Cost of Capital’. Also, explain the Significance of the cost of capital.

Answer:

The cost of capital of a firm is the minimum rate of return expected by its investors. The capital used by a firm may be in the form of equity shares, preference shares, debts, and retained earnings. The cost of capital is the weighted average cost of these sources of finance used by the firm. The concept of cost of capital occupies a very important role in financial management because investment decisions are based on it. If a firm is not able to achieve its cost of capital the market value of its shares will fall.

Definition:

Cost of capital for a firm may be defined as the cost of obtaining the funds, i.e., the average rate of return that the investors in a firm expect, for investing funds in the firm.

It is also referred to as cut-off rate,-target rate, hurdle rate, the minimum required rate of return, etc.

Some of the important definitions of cost of capital are stated below:

- “The cost of capital is the minimum required rate of earnings or the cut-off rate of capital expenditures.” – Ezra Salomon

- “The cost of capital is the minimum rate of return which a firm requires as a condition for undertaking as an investment.” – Milton H. Spencer

- “Cost of Capital represents a cut-off rate for the allocation of capital to investments of projects. It is the rate of return on a project that will leave unchanged the market price of its securities.” – James C. Van. Horne

- “The Cost of Capital is the rate of return a company must earn on an investment to maintain the value of the company.” – M. J. Fordon

- “A firm’s so-called cost of capital – commonly expressed as an annual percentage figure – is simply that rate of return which its assets must produce in order to justify raising the funds to acquire them.” – W. G. Lawpllen

Thus, on the basis of the above definitions, we can say that cost of capital is the minimum rate of return that a firm, must and, is expected to earn on its investments so as to maintain the market value of its shares.

Significance of the Cost of Capital: The concept of cost of capital is very important in making all the financial decisions of the firm. No financial decision is possible without the use of the cost of capital. Some important uses of cost of ’ capital are:

1. Helpful in Designing the Capital Structure: The concept of cost of capital plays a vital role in designing the capital structure of a company. The capital structure of a company consists of different sources of capital such as equity capital, retained earnings. Preference capital and debt capital. These sources differ from each other in terms of their respective costs. As such a company will have k to design such a capital structure that minimizes the cost of capital. Hence, the calculation of the cost of capital of different sources of capital is very essential to design an optimum capital structure.

2. Helpful in taking Capital Budgeting Decisions Capital budgeting is the process of decision making regarding the investment of funds in long-term projects of the company. The concept of cost of capital is very useful in making capital budgeting decisions $ because the cost of capital is the minimum required rate of return on an investment project. Also, a Finn must not invest in those projects which generate a return less than the cost of capital incurred for its financing.

Net Present Value (NPV) and Internal Rate of Return (IRR) are two important methods used in capital budgeting. Both of these methods are dependent upon the use of the cost of capital. In the NPV method, a project is accepted if its NPV is positive. The project’s NPV is calculated by discounting its cash flows at the cost of capital rate. Under the IRR method, the cost of capital is used as a minimum required rate of return. Hence, the cost of capital serves as a decision criterion for taking capital budgeting decisions.

3. Helpful in Evaluation of Financial Efficiency of Top Management: The concept of cost of capital can be used to evaluate the financial efficiency of top management. Such an evaluation will involve a comparison of the projected overall cost of capital with the actual cost of capital incurred by the management. Lower the actual cost of capital better is the financial performance of the management of the firm.

4. Helpful in Comparative Analysis of Various Sources of Finance: Cost of capital to be raised from various sources goes on changing from time to time. Calculation of cost of capital is helpful in the analysis of the usefulness of various sources of finance. A particular source of finance may be encouraged or discouraged on the basis of its changed cost.

5. Helpful in taking other Financial Decisions: The cost of a capital concept is also useful in making other financial decisions such as dividend policy, rights issue, working capital decisions, and capitalization of profits.

Question 6.

Explain the various factors affecting working capital requirements.

Answer:

Factors affecting working capital requirements:

1. Nature of Business: The basic nature of business influences the amount of working capital required. A trading organization usually needs a lower amount of working capital compared to a manufacturing organization. This is sales can be effected immediately upon the receipt of materials, sometimes even before that. In a manufacturing business, however, raw material needs to, be converted into furnished goods before any sales become possible. Other factors remaining the same, trading business requires less working capital. Similarly, service industries that usually don’t have to maintain inventory require less working capital.

2. Scale of operations: For an organization that operates on a higher scale of operations, the quantum of inventory, debtors that are required is generally high. Such organizations, therefore require a large amount of working capital as compared to the organizations which operate on a lower scale.

3. Business Cycle: Different phases of business cycles affect the requirement of working capita! by a firm. In case of a boom, the sales, as well as production, are likely to be higher, and therefore higher amount of working capital is required. As against this, the requirement for working capital will be lower during the period of depression as the sales as well as production will below.

4. Seasonal factor: Most businesses have some seasonality in their operations. In peak season, because of a higher level of activity, a higher amount of working capital is required. As against this, the level of activity, as well as the requirement for working capital, will be lower during the lean season.

5. Production Cycle: The production cycle is the time span between the receipt of raw materials and their conversion into finished goods. Some businesses have a longer production cycle while some have a shorter one. Duration and the length of the production cycle affect the number of funds required for raw materials and expenses. Consequently working capital requirement is higher in firms with longer processing cycles and lower in firms with shorter processing cycles.

6. Credit Allowed: Different firms allow different credit terms to their customers. These depend upon the level of competition that a firm faces as well as the creditworthiness of its clientele.

A liberal credit policy results in a higher amount of debtors, increasing the requirement of working capital.

7. Credit Availed: Just as a firm allows credit to its customers it also may get credit from its suppliers. To the extent, it avails the credit on its purchases, the working capital requirement is reduced.

8. Operating Efficiency: Firms manage their operations with varying degrees of efficiency. For example, a firm managing its raw materials efficiently may be able to manage with a smaller balance. This is reflected in a higher inventory turnover ratio. Similarly, a better debtors turnover ratio may be achieved reducing the amount tied up in receivable. Better sales effort may reduce the average time for which finished goods inventory is held. Such efficiencies may reduce the level of raw materials, finished goods, and debtors resulting in the lower requirement of working capital.

9. Availability of raw material: If the raw materials and other required materials are available freely and continuously, lower stock levels may suffice. If however, raw materials do not have a record of uninterrupted availability, higher stock levels may be required. In addition, the time lag between the placement of the order and actual receipt of the materials (also called lead time) is also relevant. The higher the lead time, the higher the quantity of material to be stored and the higher is the amount of working capital requirement.

10. Growth Prospects: If the growth potential of concern is perceived to be higher, it will require a higher amount of working capital so that it is able to meet higher production and sales target whenever required.

11. Level of Competition: A higher level of competitiveness may necessitate higher stocks of finished goods to meet urgent orders from customers. This increases the working capital requirement. Competition may also force the firm to extend liberal credit terms.

12. Inflation: With rising prices, higher amounts are required even to maintain a constant volume of production and sales. The working capital requirement of a business thus becomes higher with a higher rate of inflation. It must, however, be noted that an inflation rate of 5%, does not mean that every component of working capital will change by the same percentage. The actual requirement shall depend upon the rates of price change of different components (e.g. raw materials,’ labor cost, finished goods.) as well as their proportion in the total requirement.

Financial Management Important Extra Questions Long Answer Type

Question 1.

Explain the various determinants of the financial needs of a business?

Answer:

Determination of Financial Needs of a Business

or

Assessing Funds Requirements

Answer:

Estimating or determining the financial requirements of the business is one of the main objectives of financial planning. Before raising funds, it is essential that the requirement of funds be correctly estimated. In the absence of correct estimates, the firm may suffer either from inadequate or surplus funds. If the funds are short of its requirements, the firm will not be able to meet its day-to-day expenses and pay the short-term and long-term liabilities on time.

On the other hand, if the funds are in excess of the requirements of the business, they will remain idle and will reduce the profitability of the business. Hence, the estimates should be made in a way that all financial requirements are properly satisfied.

Funds requirements of a business can broadly be classified into two main categories. They are:

- Fixed Capital Requirements, and

- Working Capital Requirements.

Assessment of Fixed Capital Requirements: Fixed capital is the capital that is meant for fulfilling the permanent or long-term needs of the business. In the words of Shubin, “Fixed capital is the funds required for the acquisition of those assets that are to be used over and over for a long period.”

Fixed capital is required for acquiring fixed assets. Fixed assets may include the following:

- Tangible assets such as land, buildings, plant and machinery, furniture, etc.

- Intangible assets such as goodwill, patents, copyrights, etc.

A certain amount of fixed capital is also required for meeting certain expenditures not leading to the creation of an asset like research expenses, promotional expenditure incurred for the establishment of business, share issue expenses, underwriting commission, etc. The requirement of funds for these expenditures is long-term and hence the funds required in respect thereof are also included under fixed capital.

Every business needs a fair amount of fixed capital to be invested in fixed assets so as to create production or business facilities. For a new business, the fixed capital is needed in the beginning because fixed assets are needed at the time of promoting or establishing the business. For an existing business fixed capital is required for the development and expansion of the business. Hence, it is essential to have an adequate amount of fixed capital in the business.

The assessment of fixed capital requirements for a new business can be made by preparing a list of fixed assets needed by the business.

The list is prepared by the promoters by studying similar units and by taking advice from technical experts. The estimation of cost of land can be made from property dealers, estimation regarding the cost of building can be made with the help of building contractors and the cost of machinery can be ascertained from the suppliers of the machinery. Similarly, the amount to be paid for goodwill, patents, trade-marks, etc. can also be estimated.

Factors Affecting the Estimation of Fixed Capital/Fixed Assets Requirements: Factors that affect the estimation of Fixed Capital or Fixed assets requirements can be studied under two heads

(a) Internal Factors and

(b) External Factors.

(a) Internal Factors:

1. Nature of Business: Certain types of businesses require heavy investment in fixed assets, while others do not. Usually, the manufacturing concerns require more fixed assets than trading concerns. Similarly, public utility undertakings like railway, electricity, water supply, etc. require huge funds to be invested in fixed assets.

2. Size of Business: Larger the size of a concern, the greater will be the requirement of fixed capital. Also, in larger concerns, most of the activities are performed with the help of automatic machines. As such, they require a huge investment in fixed assets.

3. Types of Products: A concern that manufactures simple consumer products such as soap, oil, etc. will need a lesser amount of fixed capital in comparison to a concern that manufactures complicated products such as motorcycles, cars, etc.

4. Activities Undertaken by the Enterprise: A concern that is engaged in the manufacturing of all parts of a product by itself will require a greater amount of fixed capital as compared to a concern that gets most of the parts manufactured from outside and merely assembles them. Similarly, if a concern itself manufactures and markets its products, it will require more amount of fixed capital as compared to a concern that is engaged only in the manufacturing or only in marketing activities.

5. Mode of Acquisition of Fixed Assets: If some of the fixed assets are available on the lease or on hire, a lesser amount of fixed capital will be required. On the contrary, if all the fixed assets are to be purchased on immediate cash payment, a larger amount of fixed capital will be needed.

6. Acquisition of Old Assets: In certain industries, old plant and machinery may be available at sufficiently reduced prices and which can be used ‘satisfactorily. It would reduce the requirement of fixed capital to a great capital to a great extent. But the old plant and machinery should be used in the industries where the technological changes are moderate or slow.

7. Availability of Fixed Assets of Concessional Rate: In some areas, the Government provides land and other equipment at concessional rates to promote balanced industrial growth. In such a case, the requirement of fixed capital is reduced.

(b) External Factors:

1. General Economic Outlook: If the economy is recovering from depression and the level of business activity is expected to rise, the requirement for fixed assets will also rise and hence the need for fixed capital will also rise.

2. Technological Changes: If rapid technological innovations are taking place in an industry, the need for fixed capital will be larger because the old and out-dated machinery will have to be replaced by new ones.

3. Degree of Competition: The degree of Competition also affects the Fixed Capital-requirements. If there is a lot of competition in some industries, the need for fixed capital will be more because if some firms go on adopting the new technology, the others have to follow them.

4. Shift in Consumer Preferences: If the consumer preferences go on changing in some industries, the need for fixed capital will be more because the firm will have to produce new varieties accordingly, which require more investment in fixed assets.

Assessment of Working Capital Requirements: After the assessment of fixed Capital, funds required for working capital are assessed. The term ‘Working Capital’ is used in two ways.

In one sense it denotes the ‘total current assets’ whereas in another sense it is regarded as the excess of current assets over current liabilities. Current assets include cash, receivables (i.e., debtors and bills receivables), stock, etc. The amount required to be invested in current assets differs from one business to another. The amount depends on various factors such as nature and size of the business, duration of the production cycle, rapidity of turnover, credit policy, the quantity of stock, seasonal fluctuations, rate of growth, etc.

Working capital may be fixed or fluctuating. Fixed working capital refers to the minimum amount which would always be invested in raw materials, work-in-progress, finished goods, receivables, and cash balance. This amount is absolutely essential throughout the year on a continuous basis to maintain a desirable level of business activity. The amount required for fixed working capital mainly depends on the duration of the production cycle.

The cycle starts from the purchase of raw material; then the raw material is converted into finished goods by incurring labor and other costs. On sale, these finished goods are converted into debtors and lastly, the firm will again have cash when the debtors pay. The length of the production cycle (i.e., the length of time between the purchase of raw material and receiving cash from debtors) will determine the quantum or requirements of fixed working capital. The longer the cycle, the higher will be the requirements of fixed working capital.

The requirement of working capital over and above the fixed working capital is known as fluctuating working capital. It keeps on fluctuating from time to time according to the change in the level of business activities. For instance, during peak season, due to intensive sales, more funds are blocked in stocks and debtors and thus more amount will be required for fluctuating working capital.

The total amount of working capital can be estimated by estimating the needs of working capital for the following:

- For maintaining adequate stock

- For receivables.

- For paying day-to-day expenses

- For contingencies

1. For maintaining adequate stock: Every industrial undertaking is required to maintain a minimum stock of raw materials, work in progress, and finished goods. The requirement of the stock is determined by various factors like volume of production, the length of the production cycle, and the period for which the finished goods have to remain in a warehouse before they are sold.

2. For receivables: Finished goods may be sold for cash or on credit. Credit sales take the form of receivables (i.e., debtors and bills receivables). The amount is tied up in receivables until cash is realized from them. The amount tied up in receivables depends upon a number of factors such as quantum of credit sales, credit period allowed, the efficiency of the debt collection system, etc. For example, if a firm changes its credit period from 30 days to 60 days, the amount tied up in debtors will go up, and consequently, the need for working capital will also increase by a similar amount.

3. For paying day-to-day expenses: A firm has to carry some minimum cash balance to make payment for wages, salaries, and other expenses throughout the year. A proper cash balance is also maintained to avail of the cash discounts facilities offered by proper cash balance is also maintained to avail of the cash discounts facilities offered by the suppliers.

4. For contingencies: A minimum cash balance is also maintained for meeting unseen contingencies so that the business successfully sails through the period of crisis.

Thus, the overall financial needs of a business can be determined, by assessing the needs for fixed capital and working capital separately and then by adding the two.

Question 2.

Define the term ‘Over-Capitalisation’ and ‘Under Capitalisation’ and their causes?

Answer:

Over Capitalisation: Quiet often, the term ‘Over-Capitalisation’ is misunderstood to mean the excess of capital. But in actual practice, over-capitalized concerns have been found short of funds.

In fact, over-capitalization refers to that state of affairs where a company earns less than what should have earned at a fair rate of return on the capital invested in it. In other words, if a company is continuously unable to earn a fair rate of return on its capital, it is termed an over-capitalized company.

In the words of Bonneville Dewey, ” When a business is unable to earn a fair rate of return on its outstanding securities, it is over¬capitalised.”

According to Gerstenberg, “A corporation is over-capitalized when its earnings are not large enough to yield a fair return on the number of stocks and bonds that have been issued or when the amount of securities outstanding exceeds the current value of assets.”

The same view has been expressed by Harold Gilbert in these words, “When a company has consistently been unable to earn the prevailing rate of return o.n its outstanding securities (considering the earning of similar companies in the same industry and the degree of risk involved) it is said to be over-capitalized.”

It is clear from the above definitions that the situation of over¬capitalisation arises due to a fall in the earning capacity of the business. On account of this, the earnings will not be sufficient to give a reasonable return on capital employed in it. For example, a company is earning a profit of Rs. 8,00,000 on a total capital investment of Rs. 80,0, 000. In case the normal, rate of return prevailing in the market is 10%, this company will be said to be fairly capitalized. However, if it earns only Rs. 2,20,000 while the normal rate is 10%, the company will be said to be over-capitalized because it will be able to give a return of only 6% on the total capital employed.

In order to ascertain whether a company is earning a fair return or not, the rate of return earned by the company should be compared with similar firms in that industry. If the company’s rate of return is t .substantially less than the average rate earned by other firms, will indicate that the company is unable to earn a fair return on the capital 1 employed in it. It may also be noteworthy that a company will be said to be over-capitalized only when it is continuously unable to earn fair income over a long period of time. If its earning is reduced temporarily, owing to the occurrence of abnormal events like strikes, lockouts, etc. the company will not be called over-capitalized.

Causes of Over-Capitalisation:

Following are some of the important causes of over-capitalization:-

1. Over-Issue of Capital: If a company raises more capital than it can profitably use, there will be a large number of idle funds will the company. Because of idle funds, the earning capacity of the company will be reduced. This leads – to the situation of over-capitalization because the company will have to pay dividends on idle capital too. Hence, the rate of dividend will fall which in turn leads to a fall in the market price of its shares.

2. Promotion of the Company with Inflated Assets: A company will fall prey to over-capitalization if it is promoted with assets purchased at excessive prices, the reason is that such prices of the assets do not fear any relation to their earning capacity. Such a situation arises particularly when a partnership firm or private company is converted into a public company and in that process, their assets may be transferred to the public company at price higher than their real values. Sometimes, the promoters also transfer their property to the new company at inflated prices.

3. Promotion or Expansion of the Company during Boom Period: If a company is formed or expanded during the boom period, it; may becomes a victim of over-capitalization. The reason is that the price paid for assets will be quite high. When the boom disappears the real value of such assets will decline to a great extent whereas they will be shown in the books at their original values. Such a company is over-capitalized because its earning will fall due to depression but the assets and capital will be shown in the books in previous figures.

4. High Promotion Expenses: A certain degree of over-capitalization may be caused due to the. fact that the promoters have incurred heavy expenses on the promotion. of the company, a huge amount may have been spent on issue and underwriting of shares and the promoters may have taken a fabulous. remuneration for the services rendered by them. A major part of the earnings of the company will be utilized to write off these expenses and consequently, the company will not be able to pay fair dividends on its shares.

5. Over-estimation of Earnings at the Time of promotion: In case of a new concern,-the amount of capitalization is determined on the basis of estimates of future earnings. However, if it is found that the actual earning is less than the estimated earning, it will lead to a situation of over-capitalization. For example, if a company’s annual earnings were estimated at Rs, 50,000 and its current rate of return (or N capitalization rate) is 10% its, capitalization will be fixed at Rs. 5,00,000. Subsequently, it was found that the company actually earned (Rs. 40,000. On this basis, the company’s capitalization should have been: fixed at Rs. 4,00,000. Thus, the company will be over-capitalized by 4 Rs. 1,00,000.

6. Under-estimation of Rate of Return at the Time of Promotion: A concern may have correctly estimated the number of its earnings, but it may have under-estimated its rate of return (i.e., capitalization, rate). For example, a company’s annual earnings were estimated at ‘ Rs. 50,000 and the rate of return were fixed at 10%. By applying this rate the company’s capitalization was worked out at Rs. 5,00,000. Subsequently, it was found that the actual rate of return was 12.5%, and hence the amount of capitalization should have been fixed at Rs. i.e., Rs. 50,000 × 100. 12.5 Obviously, there is over-capitalization to the extent of Rs.1,00,000.

7. Shortage of Capital: Sometimes, the shortage of capital may also lead to over-capitalization. It may happen when the promoters underestimate the requirements of capital and raise less capital in relation to the needs of the business. In such a case the company will be forced to borrow a large sum of money at an unreasonably high rate of interest. A major part of the earnings will be absorbed by the amount of interest, leaving little for the shareholders. This will bring down the value of shares leading to over-capitalization.

8. Inadequate Depreciation: If a company does not make sufficient provisions for depreciation and replacement of assets, it will find after some time that the earning capacity of the assets is diminished leading to a fall in its earnings. This is yet another case of over-capitalization.

Under-capitalization: The term ‘under-capitalization’ does not mean a shortage or inadequacy of capital. The term is just reverse to over-capitalization. In the words of Greenberg:

“A corporation may be under-capitalized when the rate of profits, it is making on total Capital, is exceptionally high in relation to the return enjoyed by similarly situated companies in the same industry, or when it has too little capital with which to conduct its business.”

In simple words, under-capitalization is a state of affairs when the capital or resources of the company are being utilized more efficiently. As a result, the company succeeds in continuously earning an abnormally high rate of return on the capital employed in it. Such a company declares a high rate of dividend in comparison to the prevailing rate and the market value of its shares exceeds their book value. Thus under-capitalization refers to the sound financial position and good management of the company.

Causes of Under-Capitalisation:

The following are the important causes of under-capitalization:

1. Under-Estimation of Capital Requirements: At the time of promotion, the promoters may under-estimate the capital requirements of the company. This results in a situation of under-capitalization at later stages when more capital is required.

2. Under-Estimation of Earnings: Sometimes at the time of promotion, the future earnings of the company are under-estimated and the company is capitalized accordingly. If afterward it is found that the actual earnings are far in excess of the estimates, the company may find itself in a situation of under-capitalization.

3. Over-Estimation of Rate of Return at the Time of Promotion: Sometimes a concern estimates its income correctly but it over-estimates its rate of return (i.e„ capitalization rate). For example if a company’s earnings were estimated at Rs. 60,000 and the rate of earnings were fixed at 15%. By applying this rate the capitalization was fixed at‘Rs. 4,00,000 (i.e., Rs. 60,000 × \(\frac{100}{15}\)). Subsequently, it was ascertained that the actual rate was 10% and hence the amount of capitalization should have been Rs, 6,00,000 (i.e., Rs. 60,000 × \(\frac{100}{10}\)). Thus, the company is under-capitalized by Rs. 2,00,000.

4. Promotion of Company During Deflation: Companies that are floated under recessionary conditions often experience under-capitalization after the recession is over. This is because of two reasons. Firstly, during recession assets are purchased at a price that is must lower in comparison to their earning capacity. Secondly, companies established during a recession are capitalized at a low figure anticipating low earnings but when the recession is over earnings increase and the company becomes under-capitalized.

5. Conservative Dividend Policy: Certain companies follow a policy of declaring low dividends and plowing back a major part of their earnings. They build up large funds for replacement, renovation, and expansion. The result of such a policy is reflected in high earnings which is a situation of under-capitalization.

6. High Level of Efficiency: In a company where the management is very efficient, the company may operate on a high efficiency even with a meager amount of capital. Over a period, earning the position of the company will improve and it will become under-capitalized.