Reconstitution of Partnership Firm: Retirement / Death of a Partner Class 12 MCQs Questions with Answers

MCQ On Retirement And Death Of A Partner Class 12 Question 1.

Retirement or death of a partner will create a situation for the continuing partners, which is known as:

(A) Dissolution of Partnership

(B) Dissolution of partnership firm

(C) Winding up of business

(D) None of these

Answer:

(A) Dissolution of Partnership

Explanation:

Admission, retirement or death 6f a partner leads to the dissolution of the partnership and a new partnership takes its place.

![]()

MCQ Questions For Class 12 Accountancy Chapter 4 Question 2.

Saurabh, Shirin and Somesh are partners in a firm sharing profits and losses in the ratio of 3 : 2 : 1. Somesh retires and the new profit sharing ratio between Saurabh and Shirin in 3 : 2. The gaining ratio between Saurabh and Shirin will be :

(A) 3 : 2

(B) 3 :1

(C) 1 : 1

(D) 2 : 1

Answer:

(A) 3 : 2

Explanation:

Gaining ratio = New ratio – Old ratio

Saurabh’s gain = 3/5 – 3/6 = 3/30

Shirin’s gain = 2/5 – 2/h = 2/30

Gaming ratio = 3 : 2

Retirement And Death Of A Partner MCQ Class 12 Question 3.

Amla, Bimal and Kavita were partners sharing profits and losses in the ratio of 4 : 3 : 1. Bimla retires and gives her share of profit to Amla for ₹ 3,600 and to Kavita for ₹ 3,000. The gaining ratio of Amla and Kavita will be :

(A) 4 : 5

(B) 2 : 1

(C) 6 : 5

(D) 4 : 1

Answer:

(C) 6 : 5

Explanation:

Gaining ratio = 3,600/3,000 = 6 : 5

![]()

Retirement Of A Partner MCQ Class 12 Chapter 4 Question 4.

On the death of a partner, his share in the profits of the firm till the date of his death is transferred to the:

(A) Debit of Profit & Loss Account

(B) Credit of Profit & Loss Account

(C) Debit of Profit & Loss Suspense Account

(D) Credit of Profit & Loss Suspense Account

Answer:

(C) Debit of Profit & Loss Suspense Account

Explanation:

It is not possible for any firm to close its books of accounts at any time. Thus, the amount of profit or loss so ascertained is dispensed to the deceased partner through the Profit & Loss Suspense Account.

Retiring Or Death of a Partner MCQ Class 12 Question 5.

A, B and C are partners sharing profit in the ratio of 2 : 2 : 1. C retired. The new Profit Sharing ratio between A and B will be :

(A) 2 : 1

(B) 1 : 1

(C) 3 : 1

(D) 4 : 1

Answer:

(B) 1 : 1

Explanation:

As C is retiring, the ratio between A and B will remain 2 : 2 which is 1 : 1.

Retirement Or Death Of A Partner MCQ Class 12 Question 6.

According to the Partnership Act, 1932, the interest payable to the deceased partner on the amount left by him will be :

(A) 6% p.a.

(B) 10% p.a.

(C) 12% p.a.

(D) 16% p.a.

Answer:

(A) 6% p.a.

Explanation:

The Partnership Act, 1936 states that the interest payable to the deceased partner needs to be 6% p.a.

![]()

Retirement Of Partner MCQ Class 12 Chapter 4 Question 7.

The old profit sharing ratio among Rajendra, Satish and Tejpal were 2 : 2 : 1. The new profit sharing ratio after Satish’s retirement is 3 : 2. The gaining ratio is :

(A) 3 : 2

(B) 2 :1

(C) 1 : 1

(D) 2 : 2

Answer:

(C) 1 : 1

Explanation:

Gaining Ratio = New Ratio – Old Ratio

Rajendra’s Gain = \(\frac{3}{5}-\frac{2}{5}=\frac{1}{5}\)

Tejpal s Gam = \(\frac{2}{5}-\frac{1}{5}=\frac{1}{5}\)

Gaining Ratio = 1 : 1

MCQ On Retirement Of Partner Class 12 Question 8.

Pick the odd one out:

(A) Credit Balance of Capital A/c

(B) Credit Balance of Revaluation A/c

(C) Debit Balance of Statement of Profit & Loss

(D) Undistributed Reserve

Answer:

(C) Debit Balance of Statement of Profit & Loss

Explanation:

Debit balance of statement of profit and loss is odd as it is the only item that will reduce the capital.

Death Of A Partner MCQ Questions Class 12 Question 9.

A, B and C are partners. C expired on 18th December, 2019 and as per agreement surviving partners A and B directed the accountant to prepare financial statement as on 18th December, 2019 and accordingly the share of profits of C (decreased partner) was calculated as ? 12,00,000. Which account will be debited to transfer C’s share of profit:

(A) Profit and Loss Suspense Account

(B) Profit and Loss Appropriation Account

(C) Profit and Loss Account

(D) None of the above

Answer:

(B) Profit and Loss Appropriation Account

Explanation:

When a partner dies or retires, the profit is appropriated to them as well in the Profit and Loss Appropriation Account.

![]()

MCQ On Retirement Of A Partner Class 12 Question 10.

In case of retirement, if full or part of the amount payable to the retiring partner still remains to be paid, and there is no agreement among the partners then retiring partner will get :

(i) Interest @ 6% p.a. on the balance amount.

(ii) Share of profit earned proportionate to his amount outstanding to total capital of the firm,

(iii) Interest @ 9% p.a. on the balance amount.

Which out of the following is correct ?

(A) (i)

(B) (ii)

(C) (iii)

(D) Have a choice to get either (i) or (ii)

Answer:

(D) Have a choice to get either (i) or (ii)

Explanation:

In case of no agreement the retiring partner will either get @ 6% p.a-. interest rate on the remaining amount or share of profit earned proportionate to the amount outstanding to the total capital of the firm.

MCQ On Death Of A Partner Class 12 Chapter 4 Question 11.

At the time of retirement of a partner ‘Loss on Revaluation’ is debited:

(A) only to the capital account of the retiring partner

(B) to the capital accounts of all the partners in their old profit sharing ratio

(C) to the capital accounts of the remaining partners in their new profit sharing ratio

(D) to the capital accounts of remaining partners in their old profit sharing ratio

Answer:

(B) to the capital accounts of all the partners in their old profit sharing ratio

Explanation:

Loss on revaluation is a loss for the firm, i.e., there is an increase in the liabilities or a decrease in the assets.

![]()

MCQ Of Retirement Of A Partner Class 12 Question 12.

On the retirement of Hari from the firm of ‘Hari, Ram and Sharma’ the Balance Sheet showed a debit balance ₹ 12,000 in the Profit and Loss Account. For calculating the amount payable to Hari this balance will be transferred:

(A) to the credit of the Capital Accounts of Hari, Ram and Sharma equally

(B) to the debit of the Capital Accounts of Hari, Ram and Sharma equally

(C) to the debit of the Capital Accounts of Ram and Sharma equally

(D) to the credit of the Capital Accounts of Ram and Sharma equally

Answer:

(B) to the debit of the Capital Accounts of Hari, Ram and Sharma equally

![]()

Question 13.

At the time of retirement of a partner, profit on revaluation will be credited to the capital accounts of:

(A) Retiring Partner

(B) All partners in the old profit sharing ratio

(C) The remaining partners in their old profit sharing ratio

(D) The remaining partners in their new profit sharing ratio

Answer:

(B) All partners in the old profit sharing ratio

Question 14.

Gobind, Hari and Pratap are partners. On retirement of Gobind, the goodwill already appears in the Balance Sheet at ₹ 24,000. The goodwill will be written-off:

(A) by debiting all partners’ capital accounts in their old profit sharing ratio

(B) by debiting remaining partners’ capital accounts in their new profit sharing ratio

(C) by debiting retiring partners’ capital accounts from his share of goodwill

(D) None of the above

Answer:

(A) by debiting all partners’ capital accounts in their old profit sharing ratio

Explanation:

The retiring partner is entitled to his/her share of goodwill at the time of retirement because the goodwill is the result of the efforts of all the partners including the retiring one in the part. The retiring partner is compensated for his/her share of goodwill.

Question 15.

Chaman, Raman and Suman are partners sharing profits in the ratio of 5 : 3 : 2. Raman retires. The new profit sharing ratio between Chaman and Suman will be 1 : 1. The goodwill of the firm is valued at ₹ 1,00,000. Raman’s share of goodwill will be adjusted:

(A) by debiting Chaman’s Capital Account and Suman’s Capital Account with ₹ 15,000 each

(B) by debiting Chaman’s Capital account and Suman’s Capital Account with ₹ 21,429 and ₹ 8,571 respectively

(C) by debiting only Suman’s Capital Account with ₹ 30,000

(D) by debiting Raman’s Capital account with ₹ 30,000

Answer:

(C) by debiting only Suman’s Capital Account with ₹ 30,000

![]()

Explanation:

The goodwill of the retiring partner is compensated by the gaining partner/s in the gaining ratio, which in this case is only Suman. Remaining partner share the profit of retiring partner in future, therefore at the time of retirement of partner, remaining partnei/s has to compensate to the retiring partner.

Question 16.

Retiring partner’s share of goodwill is debited to remaining partners in their :

(A) Capital Ratio

(B) Gaining Ratio

(C) New Profit Sharing Ratio

(D) None of the above

Answer:

(B) Gaining Ratio

Explanation:

Retiring partner’s share of goodwill is debited to the remaining partners- in their gaining ratio.

Capital Ratio is not considered in partnership. New Profit Sharing Ratio only helps in the calculation of the gaining or sacrificing ratio.

Question 17.

In the event of death of a partner, the amount of General Reserve is transferred to Partners’ Capital Accounts in the:

(A) New Profit Sharing Ratio

(B) Old Profit Sharing Ratio

(C) Capital Ratio

(D) None of the above 32

Answer:

(B) Old Profit Sharing Ratio

Explanation:

It is done to give the required amount of share in profits of the firm to the retried partner.

![]()

Question 18.

Pick the odd one out:

(A) General Reserve

(B) Workman’s Compensation Reserve

(C) Debit balance of Statement of Profit & Loss

(D) Reserve fund ifi

Answer:

(C) Debit balance of Statement of Profit & Loss

Explanation:

Debit Balance of Statement of Profit and Loss account is an odd one as the rest are shown on the credit side and it is shown on the debit side of the Capital Account, though all axe shared among aH the partners in the old profit sharing ratio.

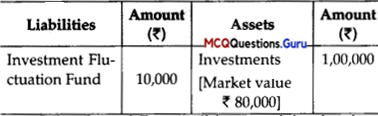

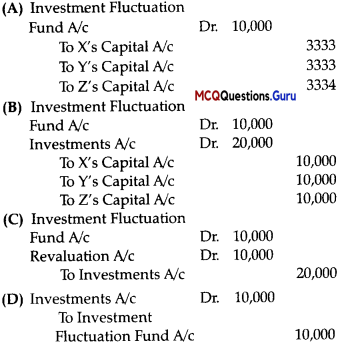

Question 19.

X, Y- and Z were partners. On 30th June, 2019 Y retired. The extract of their balance sheet is given below :

What Journal Entry will be passed for item on Y’s retirement ?

(A) Retiring Partner

(B) All partners in the old profit sharing ratio

(C) The remaining partners in their old profit sharing ratio

(D) The remaining partners in their new profit sharing ratio

Answer:

(B) All partners in the old profit sharing ratio

Assertion And Reason Based MCQs

Directions: In the following questions, a statement of Assertion (A) is followed by a statement of Reason (R). Mark the correct choice as:

(A) Both Assertion (A) and Reason (R) are true, and Reason (R) is the correct explanation of Assertion (A).

(B) Both Assertion (A) and Reason (R) are true, but Reason (R) is not the correct explanation of Assertion (A).

(C) Assertion (A) is true, but Reason (R) is false.

(D) Assertion (A) is false, but Reason (R) is true.

Question 1.

Assertion (A): On retirement, the old partnership agreement comes to an end and a new partnership agreement comes into existence between the remaining partners.

Reason (R): Retirement of the partnership leads to the reconstitution of the firm.

Answer:

(A) Both Assertion (A) and Reason (R) are true, and Reason (R) is the correct explanation of Assertion (A).

Explanation:

Retirement of a partner leads to the reconstitution of the partnership which leads to ending the old agreement and start of a new agreement.

![]()

Question 2.

Assertion (A): Retirement of partner is legal when done at will and with the consent of the partner.

Reason (R): According to Section 32 (1) of the Indian Partnership Act, 1932, “a partner may retire from the firm with the consent of all the partners or at his will, by giving written notice to all the other partners of his intention to retire.”

Answer:

(A) Both Assertion (A) and Reason (R) are true, and Reason (R) is the correct explanation of Assertion (A).

Question 3.

Assertion (A): Partnership comes to an end with the death of a partner but the firm may continue its business with new partnership agreement.

Reason (R): Death of a partner leads to the restructuring of the firm and not to the dissolution of the partnership firm.

Answer:

(A) Both Assertion (A) and Reason (R) are true, and Reason (R) is the correct explanation of Assertion (A).

Explanation:

Partners need to make a new agreement when there is a death of a partner as the partnership ceases to exist but the firm still goes on and can continue with a new agreement.

![]()

Question 4.

Assertion (A): There is only need of finding the gaining ratio in case of retirement and death of a partner.

Reason (R): The gaining ratio is used by the remaining partner to compensate the share of the outgoing or dead partner.

Answer:

(A) Both Assertion (A) and Reason (R) are true, and Reason (R) is the correct explanation of Assertion (A).

Explanation:

At the time of death or retirement, it is important to determine the gaining ratio of partners, as the gaining partners need to pay the retirinj’partner or the dead partner’s legal heir.

Question 5.

Assertion (A): When goodwill is not appearing in the books, retiring or deceased partner’s capital account is to be credited with his share of goodwill and gaining partners’ capital accounts are to be debited in gaining ratio.

Reason (R): Goodwill needs to be compensated by the gaining partners in the gaining ratio.

Answer:

(A) Both Assertion (A) and Reason (R) are true, and Reason (R) is the correct explanation of Assertion (A).

Explanation:

The gaining partner transfers the amount of goodwill to the retiring or deceased partners in proportion in order to compensate for the sacrificed goodwill as per the gaining ratio.

Question 6.

Assertion (A): Ram, Rahim and Ron share profits in the ratio 2 : 3 : 5. Ram decides to retire. The new profit sharing ratio is 3 : 5. If the profit earned was ₹ 1,50,000 before retirement. Rahim’s share is ₹ 45,000.

Reason (R): The profits are shared in the new profit sharing ratio.

Answer:

(C) Assertion (A) is true, but Reason (R) is false.

Explanation:

Rahim will get ₹ 45,000 as his share of profit but the profits are shared in the old profit sharing ratio.

![]()

Question 7.

Assertion (A): Nisha, Okra and Piya are partners. Nisha retires and her capital account after making adjustment for reserves and profit on revaluation exists at ₹ 90,000.

Okra and Piya have agreed to pay her ₹ 1,30,000 in full settlement of his claim. It implies that ₹ 40,000 (₹ 1,40,000 – ₹ 90,000) is Nisha’s share of goodwill of the firm. This will be treated by debiting T40,000 in Okra’s and Piya’s Capital Accounts in their gaining ratio and crediting Nisha’s Capital A/c.

Reason (R): If the firm has agreed to settle the account of retiring partner by paying him/her a lump-sum amount, then amount paid to him/her in excess of his adjusted capital shall be treated as his/ her share of goodwill.

Answer:

(A) Both Assertion (A) and Reason (R) are true, and Reason (R) is the correct explanation of Assertion (A).

Explanation:

In case of hidden goodwill, the amount in excess of the capital paid by the remaining partners to the retiring or deceased partner is treated as his share of goodwill.

![]()

Question 8.

Assertion (A): When a partner retires, all the unrecorded assets and liabilities, the increase or decrease in the value of assets and liabilities are done with the help of a revaluation account.

Reason (R): A Revaluation Account is prepared in order to ascertain net gain (loss) on revaluation of assets or reassessment of liabilities and bringing unrecorded items into firm’s books and the same is transferred to the capital account of all partners including retiring/deceased partner in their old profit sharing ratio.

Answer:

(A) Both Assertion (A) and Reason (R) are true, and Reason (R) is the correct explanation of Assertion (A).

Explanation:

The revaluation account helps in recording the unrecorded assets and liabilities, the increase and decrease in the value of assets and liabilities, to bring the items into firm’s books and transfer the same to the capital account of all partners in the old profit sharing ratio.

Case-Based MCQs

I. Analyse the case given below and answer the questions that follow:

Alia, Karan and Shilpa were partners in a firm sharing profits in the ratio of 5 : 3 : 2. Goodwill appeared in their books at the value of ₹ 60,000. Karan decided to retire from the firm. On the date of his retirement, goodwill of the firm was valued at ₹ 2,40,000. The new profit sharing ratio decided among Alia and Shilpa was 2 : 3. Give the answers to the questions given below:

Question 1.

How much will be transferred to Karan’s Capital Account of the existing goodwill?

(A) ₹ 18,000

(B) ₹ 30,000

(C) ₹ 12,000

(D) ₹ 72,000

Answer:

(A) ₹ 18,000

Explanation:

The existing goodwill will be transferred in the old profit sharing ratio.

![]()

Question 2.

What is Alia’s gaining or sacrificing ratio:

(A) \(\frac {1}{10}\) Gain

(B) \(\frac {1}{10}\) Sacrifice

(C) \(\frac {4}{10}\) Gain

(D) \(\frac {4}{10}\)

Answer:

(B) \(\frac {1}{10}\) Sacrifice

Explanation:

Alia = \(\frac {5}{10}\) – \(\frac {2}{5}\) = \(\frac {1}{10}\) (Sacrifice)

Question 3.

What is Shilpa’s gaining or sacrificing ratio:

(A) \(\frac {1}{10}\) Gain

(B) \(\frac {1}{10}\) Sacrifice

(C) \(\frac {4}{10}\) Gain

(D) \(\frac {4}{10}\)

Answer:

(C) \(\frac {4}{10}\) Gain

Explanation:

Shilpa = = —(gain)

Question 4.

What amount of goodwill will be transferred to Karan’s Capital account?

(A) ₹ 96,000

(B) ₹ 72,000

(C) ₹ 24,000

(D) ₹ 18,000

Answer:

(B) ₹ 72,000

Explanation:

The new goodwill is shared in the new profit sharing ratio.

II. Read the following information and answer the given questions:

Rohit, Karan and Karim are partners sharing profits and losses in the ratio of 14 : 5 : 6 respectively. Karan retires and surrenders 5/25th share in favour of Rohit. The goodwill of the firm is valued at 2 years’ purchase of Super Profit based on average profits of last three years. The profits for the last three years are ₹ 50,000, ₹ 55,000 and ?60,000, respectively. The normal profits for the similar firm are ₹ 30,000. Goodwill already appears in the books of the firm at ₹ 75,000.

![]()

Question 1.

What value of existing goodwill will be transferred to Karan’s Capital Account?

(A) ₹ 42,000

(B) ₹ 15,000

(C) ₹ 18,000

(D) ₹ 75,000

Answer:

(B) ₹ 15,000

Explanation:

Existing goodwill is shared among I the partners in the old profit sharing ratio.

Question 2.

Who is the gaining partner?

(A) Rohit

(B) Karim

(C) Both (A) and (B)

(D) Neither (A) nor (B)

Answer:

(A) Rohit

![]()

Explanation:

As Karan surrenders his full 5/25,h share to Rohit, thus Rohit is a gaining partner only.

Question 3.

What is the value of new goodwill determined?

(A) ₹ 50,000

(B) ₹ 10,000

(C) ₹ 30,000

(D) ₹ 75,000

Answer:

(A) ₹ 50,000

Explanation:

Actual Average Profit = \(\frac {50,000 + 55,000 + 60,000}{3}\) = ₹ 55,000

Normal Profit = ₹ 30,000

Super Profit = Average Profit – Normal Profit

= ₹ 55,000 – ₹ 30,000 = ₹ 25,000

Firm’s Goodwill = ₹ 25,000 x 2 = ₹ 50,000

Question 4.

What amount will be brought in by Rohit as goodwill for Karan?

(A) ₹ 50,000

(B) ₹ 10,000

(C) ₹ 30,000

(D) ₹ 75,000

Answer:

(B) ₹ 10,000

Explanation:

The goodwill is to be brought in by Rohit himself as he is the only gaining partner.

Karan’s share of Goodwill = ₹ 50,000 x \(\frac {5}{25}\)

= ₹ 10,000

![]()

III. Read the following information and answer the given questions:

Parth, Angad and Leesha are partners in a firm sharing profits and losses in the ratio of 3 : 2 : 1 respectively. Angad retires and his claim, including his capital and entitlements from the firm including his share of Goodwill of the firm, is ₹ 50,000. After this amount was determined, it was found that there was an unrecorded piece of furniture valued at ₹ 12,000 which had to be recorded. Upon recording this piece of furniture, the revised amount due to Angad was determined and settled by giving him this piece of furniture and the balance in cash.

Question 1.

To which account will the unrecorded piece of furniture will be adjusted in?

(A) Angad’s Capital Account

(B) Profit and Loss Adjustment Account

(C) Revaluation Account

(D) Profit and Loss Appropriation A/c

Answer:

(C) Revaluation Account

Explanation:

Assets is increasing

![]()

Question 2.

What is the profit on revaluation?

(A) ₹ 62,000

(B) ₹ 50,000

(C) ₹ 12,000

(D) ₹ 38,000

Answer:

(C) ₹ 12,000

Explanation:

As there is no other things to be entered in the Revaluation Account, thus, profit on revaluation will be ₹ 12,000.

Question 3.

What will be the share of Angad in profit on revaluation?

(A) ₹ 6,000

(B) ₹ 4,000

(C) ₹ 2,000

(D) 2,000

Answer:

(B) ₹ 4,000

Explanation:

Angad’s Share = 12,000 x \(\frac {2}{6}\)

= ₹ 4,000

![]()

Question 4.

What will be the final amount of the claim to be paid to Angad?

(A) ₹ 50,000

(B) ₹ 54,000

(C) ₹ 46,000

(D) ₹ 42,000

Answer:

(B) ₹ 54,000

Explanation:

Angad’s Share = ₹ 50,000+ ₹ 4,000 (profit on revaluation)

= ₹ 54,000