Reconstitution of Partnership Firm: Admission of a Partner Class 12 MCQs Questions with Answers

MCQ Questions For Class 12 Accountancy Chapter 3 Question 1.

Which of the following does not result into reconstitution of a firm ?

(A) Dissolution of partnership firm

(B) Dissolution of partnership

(C) Change in profit sharing ratio of existing partners

(D) Death of partner

Answer:

(A) Dissolution of partnership firm

Explanation:

In case of dissolution, the firm ceases to exist as in the dissolution, the relationship between the partners is terminated.

![]()

Class 12 MCQ Chapter 3 Accountancy Question 2.

Which of the following is/are required at the time of change in profit sharing ratio among partners?

(A) Accounting treatment of goodwill

(B) Revaluation of assets and reassessment of liabilities

(C) Accounting treatment of Accumulated Profit

(D) All of the above

Answer:

(D) All of the above

Admission Of A Partner MCQ Chapter 3 Question 3.

Change in profit sharing ratio among partners results in:

(A) Sacrifice of share in profit by one or more partners

(B) Gain of share in profit by one or more partners

(C) Both (A) and (B)

(D) None of the above

Answer:

(C) Both (A) and (B)

Explanation:

This may result in the gain to a few partners and loss to others. The partners who are in profit due to this change should compensate the sacrificing partner/partners in the profit sharing ratio.

![]()

Admission Of Partner MCQ Chapter 3 Class 12 Question 4.

Which of the following does not result in the change in the profit sharing ratio?

(A) When one or more partners acquire an interest in the business from another partner or partners

(B) When a partner is admitted in the firm.

(C) When a partner goes on a vacation.

(D) When a partner dies.

Answer:

(C) When a partner goes on a vacation.

Explanation:

When a partner goes on a vacation, he is not retiring from the firm, so the profit sharing ratio will not change.

MCQ Questions For Class 12 Accountancy Chapter 3 Question 5.

At the time of change in profit sharing ratio, it is important to determine the …………. and …………… of partners.

(A) Sacrificing ratio, gaining ratio

(B) Profit, loss

(C) Goodwill, profit

(D) Capital, Profit

Answer:

(A) Sacrificing ratio, gaining ratio

Explanation:

This may result in the gain to a few partners and loss to others. The partners who are in profit due to this change should compensate the sacrificing partner/partners in the profit sharing ratio.

![]()

MCQ Questions For Class 12 Accountancy Chapter 3 Question 6.

Which of the following is not required to be adjusted at the time of change in the profit sharing ratio?

(A) Determination of sacrificing ratio and gaining ratio

(B) Accounting treatment of Goodwill

(C) Revaluation of assets and reassessment of liabilities

(D) Determination of the capital of the partners

Answer:

(D) Determination of the capital of the partners

Explanation:

At the time of change in the profit sharing ratio, the sacrificing ratio and gaining ratio is to be calculated, goodwill is to be adjusted and assets and liabilities are to be adjusted but there is no necessity of determining the capital of the partners.

Reconstitution Of Partnership Firm Class 12 MCQ Question 7.

Which of the following statements is not true?

(A) When the partner is admitted it leads to reconstitution of the firm.

(B) When the partner dies it is considered as reconstitution of the firm.

(C) When the partners change their profit sharing ratio it is said to be as the reconstitution of the firm.

(D) When the partner buys an asset it is considered as the reconstruction of the firm.

Answer:

(D) When the partner buys an asset it is considered as the reconstruction of the firm.

Explanation:

When the partner buys an asset it is considered as increase in the assets of the firm.

MCQ On Admission Of A Partner Chapter 3 Class 12 Question 8.

Pick the odd one out:

(A) Admission of Partner

(B) Death of a Partner

(C) Retirement of a Partner

(D) Dissolution of the Partnership firm

Answer:

(D) Dissolution of the Partnership firm

Explanation:

Dissolution of the Partnership firm is odd one as it leads to the closure of the firm altogether and rest result in the reconstitution of partnership.

![]()

Admission Of Partner MCQ Pdf Chapter 3 Class 12 Question 9.

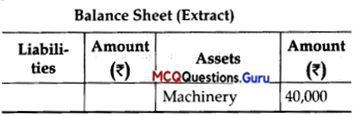

Arun and Vijay are partners in a firm sharing profits and losses in the ratio of 5 :1.

Balance Sheet (Extract)

If value of machinery in the balance sheet is undervalued by 20%, then at what value will machinery be shown in new balance sheet ?

(A) ₹ 44,000

(B) ₹ 48,000

(C) ₹ 32,000

(D) ₹ 50,000

Answer:

(D) ₹ 50,000

Explanation:

x – 20% of x = ₹ 40,000

= x – \(\frac {1}{5}\) x = ₹ 40,000

\(\frac {1}{5}\) x = ₹ 40,000

x = ₹ 40,000 x \(\frac {5}{4}\)

x = ₹ 50,000

therefore, the value of machinery is 50,000

Question 10.

Avya, Divya and Kavya were equal partners. They decided to change the profit sharing ratio to 4 : 3 : 2. For this purpose the goodwill of the firm was valued at ₹ 90,000. They journal entry for the treatment of goodwill on change in profit sharing ratio will be :

| S. No. | Particulars | L. F | Amount Dr. (₹) | Amount Cr. (₹) |

| (A) | Kavya’s Capital A/c | 10,000 | 10,000 | |

| (B) | To Avya’s Capital A/c | 10,000 | 10,000 | |

| (C) | Divya’s Capital A/c | 90,000 | 90,000 | |

| (D) | To Avya’s Capital A/c | 10,000 | 10,000 |

Answer:

Option (a) is correct.

Explanation:

AvyasGam

\(\frac {4}{9}\) – \(\frac {1}{3}\) – \(\frac {4}{9}\) – \(\frac {3}{9}\) – \(\frac {1}{9}\)

Kavya’s Sacrifice = \(\frac {1}{3}\) – \(\frac {2}{9}\) = \(\frac {3}{9}\) – \(\frac {2}{9}\) = \(\frac {1}{9}\)

Thus the sacrificing value of goodwill is \(\frac {1}{9}\) x ₹ 90,000 = ₹ 10,000 which will be transferred from Avya (Gaining Partner) to Avya (Sacrificing Partner) The sacrificing value of goodwill is ₹ 10,000.

![]()

Question 11.

Ram and Shyam are equal partners in a partnership. They decided to change their ratio as 2 : 1. On that date, general reserve appeared in the books as ₹ 30,000. What amount of reserve will be transferred to Shyam’s Capital Account ?

(A) ₹ 5,000

(B) ₹ 10,000

(C) ₹ 15,000

(D) ₹ 20,000

Ans.

(C) ₹ 15,000

Explanation:

As the general reserve is transferred as per the old profit sharing ratio, so the amount to be transferred to Shyam’s Capital Account is ₹ 15,000.

Question 12.

Avi and Babi were partners in a firm sharing profit or loss equally. With effect from 1st April 2021 they agreed to share profits in the ratio of 3 : 4. Due to change in profit sharing ratio, Avi’s gain or sacrifice will be:

(A) Gain \(\frac {1}{14}\)

(B) Sacrifice \(\frac {1}{14}\)

(C) Gain \(\frac {4}{7}\)

(D) Sacrifice \(\frac {3}{7}\)

Ans.

(B) Sacrifice \(\frac {1}{14}\)

Explanation: = \(\frac {1}{2}\) – \(\frac {3}{7}\) = \(\frac {7}{14}\) – \(\frac {6}{14}\) = \(\frac {1}{14}\) (Sacrifice)

![]()

Question 13.

Anwar and Bashir were partners in a firm sharing profit or losses in the ratio 7:5. With effect from 1st April 2021 they agreed to share profits in the ratio of 5:4. Due to the change in profit sharing ratio what is Bashir’s gain or sacrifice?

(A) Gain \(\frac {1}{36}\)

(B) Sacrifice \(\frac {1}{36}\)

(C) Gain \(\frac {1}{12}\)

(D) Sacrifice \(\frac {1}{12}\)

Ans.

(B) Sacrifice \(\frac {1}{36}\)

Explanation: = \(\frac {1}{36}\) = \(\frac {1}{36}\) = \(\frac {1}{36}\) = \(\frac {1}{36}\) (Gain) I

Question 14.

Identify the journal entry for the transfer of workman compensation fund to the Partner’s Capital Account at the time of change of profit sharing ratio.

(A) Profit & Loss AppropñatiOfl A/c Dr.

To Partners’ Capital/Current A/cs

(Being Workmen’s Compensation Fund to the Partners Capital A/c)

(B)IPrOflt&LOSSNC Dr.

To Workmen’s CompensationFund A/cs

(Being Workmen’s Compensation Fund to the Partners Capital A/c)

(C) Partners’ Capital/Current A/cs Dr.

To Workmen’s Compensation Fund A/c

(Being Workmen’s Compensation Fund to the Partners Capital A/c)

(D) Workmen’s Compensation Fund A/c Ðr

To All Partners’ Capital A/cs

(Being Workmen’s CompensationFund to the Partners Capital A/c)

Ans.

(D) Workmen’s Compensation Fund A/c Ðr

To All Partners’ Capital A/cs

(Being Workmen’s CompensationFund to the Partners Capital A/c)

![]()

Question 15.

How is goodwill treated when there is a change in the profit sharing ratio?

(A) The gaining partners give the amount of goodwill to the sacrificing partner.

(B) The gaining partners give the proportionate amount of goodwill to the sacrificing partner.

(C) The sacrificing partner gives the amount of goodwill to the gaining partner.

(D) The sacrificing partner give the proportionate amount of goodwill to the gaining partner.

Ans.

(B) The gaining partners give the proportionate amount of goodwill to the sacrificing partner.

Question 16.

Which account will be prepared to record the adjusting amount of assets and liabilities?

(A) Profit and Loss Appropriation Account

(B) Profit and Loss Adjustment Account

(C) Realisation Account

(D) Revaluation Account

Ans.

(D) Revaluation Account

Explanation:

At the time of change in profit sharing ratio, the value of assets and reassessment of liabilities are revalued and the difference between the existing value and revalued amount is transferred to Revaluation Account.

Assertion and Reason Based MCQs

Directions: In the following questions, a statement

of Assertion (A) is followed by a statement of

Reason (R). Mark the correct choice as:

(A) Both Assertion (A) and Reason (R) are true, and Reason (R) is the correct explanation of Assertion (A).

(B) Both Assertion (A) and Reason (R) are true, but Reason (R) is not the correct explanation of Assertion (A).

(C) Assertion (A) is true, but Reason (R) is false.

(D) Assertion (A) is false, but Reason (R) is true.

![]()

Question 1.

Assertion (A): When a new partner is admitted it results in the restructuring of the firm.

Reason (R): When a new partner is added it leads to the change in profit sharing ratio.

Ans.

(B) Both Assertion (A) and Reason (R) are true, but Reason (R) is not the correct explanation of Assertion (A).

Explanation:

Admission is called restructuring of the firm as it leads to not only change in profit sharing ratio but also the change in the partnership deed.

Question 2.

Assertion (A): Restructuring of the firm leads to the change in the profit sharing ratio.

Reason (R): A change in the profit sharing ratio among the existing partners results in a gain of additional share in the future profit for some partners while a loss of a part thereof for other partners.

Answer:

(B) Both Assertion (A) and Reason (R) are true, but Reason (R) is not the correct explanation of Assertion (A).

Explanation:

Restructuring of the firm is when there is admission, retirement, death or even just change in the profit sharing ratio.

Question 3.

Assertion (A): Dissolution of the partnership firm is also called restructuring of the partnership.

Reason (R): Restructuring of the firm leads to the change in profit sharing ratio and adjustment of goodwill.

Answer:

(D) Assertion (A) is false, but Reason (R) is true.

Explanation:

Dissolution of the partnership firm is also called end of the partnership.

![]()

Question 4.

Assertion (A): At the time of change in profit sharing ratio, it is important to determine the sacrificing ratio and gaining ratio of partners. Reason (R): The gaining partners compensate the sacrificing partners by paying them appropriate

amount of goodwill.

Answer:

(A) Both Assertion (A) and Reason (R) are true, and Reason (R) is the correct explanation of Assertion (A).

Explanation:

At the time of change in profit sharing ratio, it is important to determine the sacrificing ratio and gaining ratio of partners, as the gaining partners need to compensate the sacrificing partners.

Question 5.

Assertion (A): The gaining partner transfers the amount of goodwill to the sacrificing partners in proportion.

Reason (R): The gaining ratio is the share of profit gained by a partner when there is a change in the profit sharing ratio.

Answer:

(B) Both Assertion (A) and Reason (R) are true, but Reason (R) is not the correct explanation of Assertion (A).

Explanation:

The gaining partner transfers the amount of goodwill to the sacrificing partners in proportion in order to compensate for the sacrificed goodwill as per the gaining ratio.

Question 6.

Assertion (A): Ram and Rahim share profits in the ratio 2:3. They decide to change the profit sharing ratio and share the profits equally. Ram is the gaining partner.

Reason (R): Ratio of Ram is \(\frac {1}{10}\)

Answer:

(B) Both Assertion (A) and Reason (R) are true, but Reason (R) is not the correct explanation of Assertion (A).

Explanation:

Ram is the gaining partner as his share of profit is increasing from to \(\frac {2}{5}\) to \(\frac {1}{2}\)

![]()

Question 7.

Assertion (A): Norsang and Nyomit share profit and loss in the ratio of 1:2. They decide to change the profit sharing ratio to 2:3. The goodwill of the firm stood at ?60,000. Norsang gave ₹ 2,000 to Nyomit as the share of goodwill.

Reason (R): If the partners decide to change their profit sharing ratio, the gaining partner must compensate the sacrificing partner by way of payment to him as goodwill in the gaining ratio.

Answer:

(A) Both Assertion (A) and Reason (R) are true, and Reason (R) is the correct explanation of Assertion (A).

Question 8.

Assertion (A): When the profit sharing ratio changes, all the reserves are transferred to the Profit and Loss Appropriation Account.

Reason (R): The reserves are transferred in the old profit sharing ratio.

Answer:

(B) Both Assertion (A) and Reason (R) are true, but Reason (R) is not the correct explanation of Assertion (A).

Explanation:

When the profit sharing ratio changes all the reserves are transferred to the Profit and Loss Appropriation Account in the old profit sharing ratio, so that the accumulated profits can be distributed among the partners for the restructuring of the firm.

Case-Based MCQs

I. Analyse the case given below and answer the questions that follow:

Mishra, Tiwari and Singh are partners in a firm sharing profits and losses in the ratio of 1 : 2 : 3. Their capitals on 31st March, 2017 were ₹ 4,00,000, ₹ 3,00,000 and ₹ 2,00,000 respectively. From 1st April, 2017 they agreed to change their profit and loss sharing ratio as 3 : 2 : 1 respectively.

On the day of reconstitution of the firm, their balance sheet showed a debit balance of Profit and Loss Account ? 30,000 and general reserve of ₹ 60,000. The value of the firm was decided at ₹ 2,10,000. It was also decided that the value of an asset which was previously not recorded in the books will be recorded with ₹ 21,000.

![]()

Question 1.

Sacrifice made by Tiwari on the reconstitution of the partnership will be:

(A) \(\frac {1}{2}\)

(B) \(\frac {1}{3}\)

(C) \(\frac {1}{4}\)

(D) Nil

Answer:

(D) Nil

Explanation:

There is no change in the profit I sharing ratio of Tiwari.

![]()

Question 2.

What will be the balance of Mishra’s capital on the reconstitution of the partnership after taking into account the above adjustments?

(A) ₹ 3,48,500

(B) ₹ 3,38,500

(C) ₹ 4,08,500

(D) ₹ 4,88,500

Answer:

(B) ₹ 3,38,500

Explanation:

Sacrifice/gain of Mishra = Old share-Newshare = \(\frac {1}{6}\) – \(\frac {3}{6}\) = \(\frac {2}{6}\)(gain)

Goodwill to be compensated by him to the sacrificing partner:

₹ 2,10,000 x \(\frac {2}{6}\) = ₹ 70,000

Capital of Mishra after all adjustments = Old Capital + General Reserve + Gain on Revaluation – Dr.

balance of Profit and Loss – Goodwill compensated by him = ₹ (4,00,000 + 10,000 + 3,500 – 5,000 – 70,000)

= ₹ 3,38,500

![]()

Question 3.

The ratio in which the loss or gain on revaluation to be distributed among the partners will be …………….

(A) 1 : 3 : 2

(B) 2 : 3 :1

(C) 3: 2 :1

(D) 1 : 2 : 3

Answer:

(D) 1 : 2 : 3

Explanation:

Loss or gain on revaluation is always distributed in old profit sharing ratio on reconstitution of partnership.

Question 4.

What journal entry will be passed for the treatment of Profit and Loss balance?

| (A) Profit & Loss Appropriation A/c Dr. To Mishra’s Capital A/c To Tiwari’s Capital A/c To Singh’s Capital A/c (Being the loss being shared by the partners) | 30,000 | 5,000 10,000 15,000 | |

| (B) Mishra’s Capital A/c Dr. Tiwari’s Capital A/c Dr. Singh’s Capital A/c Dr. To Profit and Loss A/c (Being the loss being shared by the partners) | 5,000 10,000 15,000 | 30,000 | |

| (C) Profit & Loss Appropriation A/c To Mishra’s Capital A/c To Tiwari’s Capital A/c To Singh’s Capital A/c (Being the loss being shared by the partners) | 60,000 | 10,000 20,000 30,000 | |

| (D) Mishra’s Capital A/c Dr. Tiwari’s Capital A/c Dr. Singh’s Capital A/c Dr. To Profit and Loss A/c (Being the loss being shared by the partners) | 10,000 20,000 30,000 | 60,000 |

Answer:

Option (B) is correct.

II. Read the following information and answer the given questions:

Abha and Vibha are partners, who shared profits and losses in the ratio of 2 :1. From the 1st January 2021, the partners decided to change their profit – sharing ratio to 3 : 2 and agreed upon the following:

(i) Goodwill of the firm valued at ₹ 45,000.

(ii) Creditors of ₹ 8,000 is not likely to be claimed hence should be written off.

(iii) Land and Building is overvalued by 10%.

(iv) Provision for doubtful debts to be reduced to ₹ 3,000 The partners neither want to record the goodwill nor to distribute the general reserve.

![]()

Question 1.

Abha’s gain or sacrifice in the profit sharing ratio is:

(A) Gain \(\frac {1}{3}\)

(B) Sacrifice \(\frac {1}{3}\)

(C) Gain \(\frac {1}{15}\)

(D) Sacrifice \(\frac {1}{15}\)

Answer:

(D) Sacrifice \(\frac {1}{15}\)

Explanation:

Abha’s sacrifice = \(\frac {2}{3}\) – \(\frac {3}{5}\) = \(\frac {10}{15}\) – \(\frac {9}{15}\) = \(\frac {1}{15}\)

Question 2.

Vibha s gain or sacnfice in the profit shanng raflo is:

(A) Gain \(\frac {1}{3}\)

(B) Sacrifice \(\frac {1}{3}\)

(C) Gain \(\frac {1}{15}\)

(D) Sacrifice \(\frac {1}{15}\)

Answer:

(C) Gain \(\frac {1}{15}\)

Explanation:

Vibha’s gain = \(\frac {1}{3}\) – \(\frac {2}{5}\) = \(\frac {5}{15}\) – \(\frac {6}{15}\) = \(\frac {-1}{15}\)

Question 3.

Who will give the amount of goodwill to whom in what amount?

(A) Abha will give ₹ 4,500 to Vibha.

(B) Vibha will give ₹ 4,500 to Abha.

(C) Abha will give ₹ 3,000 to Vibha.

(D) Vibha will give ₹ 3,000 to Abha.

Answer:

(D) Vibha will give ₹ 3,000 to Abha.

![]()

Question 4.

Which account will be opened to transfer the amount of creditors to be written off?

(A) Realisation Account

(B) Revaluation Account

(C) Both (A) and (B)

(D) Neither (A) nor (B)

Answer:

(B) Revaluation Account

Explanation:

Revaluation account is a nominal account, which is prepared for the distribution and transfer of profits and losses arising due to the increase and decrease of the book value of assets and liabilities during change in profit sharing ratio, admission of a partner, retirement of a partner and death of a partner.

III. Read the following hypothetical text and answer the given questions:

Rajiv, Poonam and Abhishek are partners sharing profits in ratio of 3 : 2 : 1 respectively. From 1st January, 2019 they decided to share profits in the ratio of 1 : 3 : 2. The partnership deed provides that in the event of any change in profit sharing ratio, the goodwill should be valued at the three years’ purchase of the average of five years’ profits. The profits and losses of the preceding five years are :

2014 : ₹ 1,20,000

2015 : ₹ 3,00,000

2016 : ₹ 3,40,000

2017 : ₹ 3,80,000

2018 :11,40,000 (Loss)

Question 1.

Which partner sacrifices the shares of profit?

(A) Rajiv

(B) Poonam

(C) Abhishek

(D) Can’t be determined

Answer:

(A) Rajiv

Explanation:

Rajiv = \(\frac{3}{6}-\frac{1}{6}=\frac{2}{6}\) (sacrifice)

Poonam = \(\frac{2}{6}-\frac{3}{6}=-\frac{1}{6}\) (gain)

Abhishek = \(\frac{1}{6}-\frac{2}{6}=-\frac{1}{6}\) – (gain)

![]()

Question 2.

The gaining ratio of Poonam is:

(A) \(\frac{2}{6}\)

(B) \(\frac{3}{6}\)

(C) \(\frac{1}{6}\)

(D) \(\frac{2}{6}\)

Answer:

(C) \(\frac{1}{6}\)

Question 3.

What is the amount of goodwill is to be given by the gaining partners?

(A) ₹ 1,00,000 each

(B) ₹ 1,20,000 and ₹ 80,000

(C) ₹ 1,50,000 and ₹ 1,00,000

(D) ₹ 80,000 each

Answer:

(A) ₹ 1,00,000 each

Explanation:

The gaining ratio is 1 : 1.

![]()

Question 4.

The goodwill of the firm is ………….

(A) ₹ 9,00,000

(B) ₹ 6,00,000

(C) ₹ 7,00,000

(D) ₹ 6,60,000

Answer:

(B) ₹ 6,00,000

Explanation:

Average Profit

= ₹ 2,00,000

Goodwill at 3 years’ purchases of Average Profits = ₹ 2,00,000 x 3 = ₹ 6,00,000

Question 1.

Bishan and Sudha were partners in a firm sharing profits and losses in the ratio of 5 : 3. Alena was admitted as a new partner. It was decided that the new profit sharing ratio of Bishan, Sudha and Alena will be 10 : 6 : 5. The sacrificing ratio of Bishan and Sudha will be:

(A) 5 : 3

(B) 25 : 78

(C) 6 : 5

(D) 2 : 1

Answer:

(B) 25 : 78

Explanation:

Bishan’s Sacrificing ratio = \(\frac{5}{8}-\frac{10}{21}=\frac{105}{168}-\frac{80}{168}=\frac{25}{168}\)

Sudha’s Sacrificing Ratio = \(\frac{3}{8}-\frac{6}{21}=\frac{63}{168}-\frac{48}{168}=\frac{15}{168}\)

Sacrificing Ratio = 25 : 15 = 5 : 3

![]()

Question 2.

A, B and C are partners in a firm. If D is admitted as a new partner:

(A) Old firm is dissolved.

(B) Old firm and old partnership is dissolved.

(C) Old partnership is reconstituted.

(D) None of the above.

Answer:

(C) Old partnership is reconstituted.

Explanation:

In Admission of a partner, the old partnership is reconstituted. Old firm is dissolved in case of dissolution of the partnership firm.

Question 3.

The ratio which is computed to determine the sacrifice of the old partners made in favour of new partner which is admitted into partnership is :

(A) Gaining Ratio

(B) Old Profit Sharing Ratio

(C) New Profit Sharing Ratio

(D) Sacrificing Ratio

Answer:

(D) Sacrificing Ratio

Explanation:

The ratio which is computed to determine the sacrifice of the old partners made in favour of new partner which is admitted into’ partnership is sacrificing ratio, calculated with the help of old profit sharing ratio and new profit sharing ratio.

Gaining Ratio is the one when old partner retires or dies calculated with the help of old profit sharing ratio and new profit sharing ratio.

![]()

Question 4.

The account which is prepared to adjust the increase or decrease in the value of assets at the time of admission of partner is called :

(A) Realisation Account

(B) Revaluation Account

(C) P & L Account

(D) None of these

Answer:

(B) Revaluation Account

Explanation:

Revaluation Account is prepared to adjust the increase or decrease in the values of assets and liabilities at the time of admission of a partner.

Realisation Account is prepared at the time of dissolution of the firm. P & L Account is prepared while making the final accounts irrespective of reconstitution of the firm.

Question 5.

Ram and Shyam were equal partners in a partnership. They admitted Mohan for \(\frac {1}{4}\) share. He acquired his share equally from Ram and Shyam. Consider the statements below :

(i) Ram and Shyam both will sacrifice equally to Mohan.

(ii) Ram’s sacrificing ratio is more than that of Shyam.

(iii) The new profit sharing ratio of Ram, Shyam and Mohan will be 11 : 6 : 5.

Choose the correction option :

(A) Only (i) is correct.

(B) Only (ii) is correct.

(C) Only (iii) is correct.

(D) All of the above IS

Answer:

(A) Only (i) is correct.

Explanation:

As Mohan acquires his equally from Ram and Shyam, the sacrificing ratio is equal for both, hence statement (i) is only true.

Question 6.

A and B are partners sharing profit in the ratio of 3 : 2. They admit C as a partner by giving him l/3rd share in future profits. The new ratio will be :

(A) 12 : 8 : 5

(B) 8 : 12 : 5

(C) 5 : 5 :12

(D) None of these

Answer:

(D) None of these

![]()

Explanation:

A’s New share = \(\frac{3}{5} \times \frac{2}{3}\) = \(\frac {6}{15}\)

B’s New share = \(\frac{2}{5} \times \frac{2}{3}=\frac{4}{15}\)

C’s Share = \(\frac{1}{3}=\frac{5}{15}\)

A : B : C = 6 : 4 : 5

Thus none of the mentioned ratios is correct.

Question 7.

When a new partner enters into the partnership firm, old partners some part of their old share.

(A) Sacrifice

(B) Gain

(C) Retain

(D) None of these

Answer:

(A) Sacrifice

Question 8.

Arun and Barun share profits in the ratio of 2 : 1. Charan is admitted with 1/5 share in profits. Charan acquires 2/3 of his share from Arun and 1/3 of his share from Barun. The new ratio will be:

(A) 2 : 1 :1

(B) 23 :13 : 12

(C) 8 : 4 : 3

(D) 13 : 23 :12

Answer:

(C) 8 : 4 : 3

Explanation:

Aran’s New Share = \(\frac{2}{3} \times \frac{4}{5}=\frac{8}{15}\)

Barun s Share = \(\frac{1}{3} \times \frac{4}{5}=\frac{4}{15}\)

Charan’s Share = \(\frac{1}{5}=\frac{3}{15}\)

Arun: Barun : Charan = 8 : 4 : 3

![]()

Question 9.

For which of the following situations, the old profit sharing ratio of partners is used at the time of admission of a new partner?

(A) When new partner brings only a part of his share of goodwill.

(B) When new partner is not able to bring his share of goodwill.

(C) When at the time of admission, goodwill already appears in the balance sheet.

(D) When new partner brings his share of goodwill in cash.

Answer:

(C) When at the time of admission, goodwill already appears in the balance sheet.

Explanation:

The old profit sharing ratio of the partners is used at the time of admission of a new partner when the goodwill already exists in the balance Sheet. In other cases the new partner just needs to compensate as per the gaining ratio.

![]()

Question 10.

Anita and Babita were partners sharing profits and losses in the ratio of 3 : 1. Savita was admitted for l/5th share in the profits. Savita was unable to bring her share of goodwill premium in cash. The journal entry recorded for goodwill premium is given below:

| Date. | Particulars | L.F | Amount Dr. (₹) | Amount Cr. (₹) |

| Savita’s Current A/c Dr. To Anita’s Capital A/c To Babita’s Capital A/c (Being adjustment of goodwill premium on Savita’s Admission) | 24,000 | 8,000 16,000 |

The new profit sharing ratio of Anita, Babita and Savita, will be:

(A) 41 : 7 : 12

(B) 13 : 12 : 10

(C) 3 : 1 : 1

(D) 5 : 3 : 2

Answer:

(A) 41 : 7 : 12

Explanation:

New share = Old share – Sacrificing share

Anita’s new share = \(\frac{3}{4}-\left(\frac{1}{5} \times \frac{1}{3}\right)=\frac{3}{4}-\frac{1}{15}=\frac{41}{60}\)

Babita’s new share = \(\frac{1}{4}-\left(\frac{1}{5} \times \frac{2}{3}\right)=\frac{1}{4}-\frac{2}{15}=\frac{7}{60}\)

Sarita’s share = \(\frac{1}{5} \times \frac{12}{12}=\frac{12}{60}\)

![]()

Question 11.

When the incoming partner brings his share of premium for goodwill in cash, it is adjusted by crediting to :

(A) His Capital Account

(B) Premium for Goodwill Account

(C) Sacrificing Partners’ Capital Accounts

(D) None of the above

Answer:

(C) Sacrificing Partners’ Capital Accounts

Explanation:

When the incoming partner brings his share of premium for goodwill in cash, it is adjusted by crediting to sacrificing partners’ capital account. His capital is debited and premium for Goodwill account is created when the new partner doesn’t bring the goodwill in cash.

Question 12.

Z is admitted in a firm for l/4th share in the profits for which he brings ? 10,000 towards premium for goodwill. It will be taken by the old partners in :

(A) Old Profit Sharing Ratio

(B) New Profit Sharing Ratio

(C) Sacrificing Ratio

(D) None of the above A

Answer:

(C) Sacrificing Ratio

Explanation:

The amount of goodwill brought by the new partner is shared by the sacrificing partner in the sacrificing ratio. The old profit sharing ratio and new profit sharing ratio help in the calculation of the sacrificing ratio. The Accumulated profits and revaluation profit or loss is shared in the old profit sharing ratio.

![]()

Question 13.

If the incoming partner is to bring Premium for Goodwill in cash and also a balance exists in Goodwill Account, then this Goodwill Account is written off among old partners in :

(A) New Profit Sharing Ratio

(B) Old Profit Sharing Ratio

(C) Sacrificing Ratio

(D) None of the above A

Answer:

(B) Old Profit Sharing Ratio

Explanation:

The goodwill shown in the balance sheet is shared among the partners in’ I the old profit sharing ratio. Sacrificing ratio is used to share the goodwill to be brought in by the new partner. New profit sharing ratio is used to reconstitute the capital of the firm if it is decided by the partners to make it proportionate to their profit sharing ratio.

Question 14.

Mohit and Govind were partners in a firm in the ratio of 1: 2. They admitted Ravi for l/5th share in profits. He brought ? 2,50,000 for capital but could not bring goodwill. The goodwill of the firm was valued at ? 3,00,000. What Journal Entry will be passed for the treatment of goodwill ?

(A) Asset A/c Dr.

To Ravi’s Capital A/c

(B) Cash A/c Dr.

To Goodwill A/c

(C) Mohit’s Capital A/c Dr.

Govind’s Capital A/c Dr.

To Ravi’s Capital A/c

(D) Ravi’s Capital A/c Dr.

To Mohit’s Capital A/c To Govind’s Capital A/c

Answer:

(D) Ravi’s Capital A/c Dr.

To Mohit’s Capital A/c To Govind’s Capital A/c

Explanation:

The goodwill share of Ravi will be shared among the sacrificing partners in the sacrificing ratio.

![]()

Question 15.

Anita and Babita are partners sharing profits and losses as 3 : 2. Chandani is admitted and profit sharing ratio becomes 4 : 3 : 2. Goodwill is valued at ₹ 94,500. Chandani brings required goodwill in cash. Goodwill amount that will be credited by Chandani is:

(A) Anita ₹ 14,000 and Babita ₹ 7,000

(B) Anita ₹ 12,000 and Babita ₹ 9,000

(C) Anita ₹ 15,000

(D) Anita ₹ 21,000 A

Answer:

(C) Anita ₹ 15,000

Explanation:

Only Anita is the partner that is sacrificing her share and both Babita and Chandani are gaining, so they need to give the proportionate goodwill to Anita.

Question 16.

When the value of goodwill is not specified at the time of admission of a partner is called …………..

(A) Goodwill in Kind

(B) Hidden Goodwill

(C) Both (A) and (B)

(D) Neither (A) nor (B)

Answer:

(B) Hidden Goodwill

![]()

Question 17.

General Reserve at the time of admission of a partner is transferred to :

(A) Revaluation Account

(B) Old Partners’ Capital Accounts

(C) Neither of the two

(D) Both (A) and (B)

Answer:

(B) Old Partners’ Capital Accounts

Explanation:

The reserve and surplus that are there during the reconstitution of the firm is to be shared by the old partners in old partners’ capital or current account in the old profit sharing ratio.

Question 18.

Balance in the Investment Fluctuation Reserve, after meeting the loss on revaluation of Investments, at the time of admission of a partner will be transferred to:

(A) Old Partners’ Capital Accounts

(B) Revaluation Account

(C) Sacrificing Ratio

(D) None of the above

Answer:

(A) Old Partners’ Capital Accounts

Explanation:

Any accumulated reserves and surplus is transferred to the old partners’ capital accounts and not to the revaluation account in the old profit sharing ratio and not in sacrificing ratio.

![]()

Question 19.

On admission of a new partner, increase in the value of assets is debited to :

(A) P & L Adjustment Account

(B) Assets Account

(C) Old Partners’ Capital Accounts

(D) None of the above 52

Answer:

(B) Assets Account

Explanation:

On admission of a new partner, increase in the value of assets is debited to Assets account and shown in the balance sheet and the Revaluation Account. It is credited to the Revaluation account and P/L Adjustment and Old Partners Capital Account are not used for revaluation of assets and liabilities.

Question 20.

Pick the odd one out:

(A) Increase in assets

(B) Increase in liabilities

(C) Decrease in liabilities

(D) Taking an unrecorded asset in books

Answer:

(B) Increase in liabilities

Explanation:

Increase in liabilities is the only item which will come in the credit side of the revaluation account.

![]()

Question 21.

Karan and Saran are partners in a partnership. They admitted Mohit as a new partner for 1/4th share in profits.

If 5% creditors are not likely to claim their dues, what amount of creditors will be shown in Balance Sheet on Mohit’s admission?

(A) ₹ 20,000

(B) ₹ 23,750

(C) ₹ 25,000

(D) ₹ 26,250

Answer:

(B) ₹ 23,750

Explanation: 25,000 – 5% of 25,000 = 25,000 – 1,250 = 23,750

Question 22.

Ravi and Gaurav are partners in a firm. They want to admit Dhruv for \(\frac {1}{4}\) share in profit. For this, they revalued their machinery from ₹ 30,000 to ₹ 40,000 and creditors from ₹ 1,10,000 to ₹ 1,00,000. What journal entry will be passed :

(A) Machinery A/c Dr.

Creditors A/c Dr.

To Revaluation A/c

(B) Machinery A/c Dr.

Revaluation A/c Dr.

To Creditors A/c

(C) Machinery A/c Dr.

To Revaluation A/c

To Creditors A/c

(D) None of the above

Answer:

(A) Machinery A/c Dr.

Creditors A/c Dr.

Explanation:

Increase in assets and decrease in liabilities is debited to the revaluation account.

![]()

Question 23.

The accumulated profit of the firm will be recorded in.which of the following accounts at the time of admission of a new partner?

(A) Revaluation Account

(B) Old Partner’s Capital Account

(C) Profit and Loss Account

(D) All Partner’s Capital Account

Answer:

(B) Old Partner’s Capital Account

Question 24.

Which of the following is not readjusted at the time of admission of a new partner?

(A) Capital Account

(B) Profit Sharing Ratio

(C) Profit and Loss Account

(D) None of the above 52

Answer:

(C) Profit and Loss Account

Explanation:

The Profit and Loss Account is not readjusted at the time of admission of a new partner only the capital account and profit sharing ratio is adjusted. Change in the value of assets and liabilities are done through the revaluation account.

![]()

Question 25.

If goodwill is not brought in cash by the new partner, it should be debited to his Account.

(A) Current

(B) Capital

(C) Loan

(D) Either (A) or (B) 52

Answer:

(D) Either (A) or (B) 52

Explanation:

If goodwill is not brought in cash by the new partner, it should be debited to his either his capital or current account. The amount is transferred to the loan account only during retirement or death of the partner and the remaining partner cannot pay the amount at the moment.

Assertion And Reason Based MCQs

Directions: In the following questions, a statement of Assertion (A) is followed by a statement of Reason (R). Mark the correct choice as:

(A) Both Assertion (A) and Reason (R) are true, and Reason (R) is the correct explanation of Assertion (A).

(B) Both Assertion (A) and Reason (R) are true, but Reason (R) is not the correct explanation of Assertion (A).

(C) Assertion (A) is true, but Reason (R) is false.

(D) Assertion (A) is false, but Reason (R) is true.

Question 1.

Assertion (A): A new partner can be admitted into a partnership firm with the consent of all the existing partners.

Reason (R): According to Section 31 of the Indian Partnership Act, 1932, a new partner shall not be introduced into a firm without the consent of all the existing partners, unless it is agreed otherwise by the partners in the partnership deed.

Answer:

(A) Both Assertion (A) and Reason (R) are true, and Reason (R) is the correct explanation of Assertion (A).

![]()

Question 2.

Assertion (A): It is the right of new partner on the firm’s assets and liabilities.

Reason (R): Old Partners of the firm sacrifice some profit according to the new profit sharing ratio in favour of incoming partner.

Answer:

(B) Both Assertion (A) and Reason (R) are true, but Reason (R) is not the correct explanation of Assertion (A).

Explanation:

It is the right of new partner on the firm’s assets and liabilities on behalf of capital which is brought by him/her, as he/ she brings the required amount of capital and goodwill.

Question 3.

Assertion (A): New Profit Sharing Ratio is the ratio in which old partners including the new partner, share the profits or losses of the firm.

Reason (R): When a new partner is admitted to the firm it is necessary to calculate the new profit sharing ratio with the help of the share agreed to forgo by the old partners.

Answer:

(B) Both Assertion (A) and Reason (R) are true, but Reason (R) is not the correct explanation of Assertion (A).

Explanation:

New Profit Sharing Ratio is the ratio in which old partners including the new partner, share the profits or losses of the firm, calculated as agreed by the partners, as the future profit and loss need to be shared differently as a new partner is added to the firm.

![]()

Question 4.

Assertion (A): When the new partner brings his share of goodwill in cash and it is to be paid to the existing partners privately, no entry is passed in the books.

Reason (R): The intention of the partners is not to show any amount/transaction relating to goodwill for any of the reasons.

Answer:

(A) Both Assertion (A) and Reason (R) are true, and Reason (R) is the correct explanation of Assertion (A).

Question 5.

Assertion (A): If goodwill is already appearing in the book, old goodwill should always be written off among old partners in the old ratio.

Reason (R): The amount of goodwill should be adjusted through partners’ capital/current accounts.

Answer:

(B) Both Assertion (A) and Reason (R) are true, but Reason (R) is not the correct explanation of Assertion (A).

Explanation:

If goodwill is already appearing in the book, old goodwill should always be written off among old partners in the old ratio through the Capital or Current Accounts as per the AS 26.

![]()

Question 6.

Assertion (A): Whenever new partner brings goodwill in cash, he should bring the amount of goodwill, only for his share.

Reason (R): It is a common rule that the gaining partner should compensate the sacrificing partner to the extent of his gain.

Answer:

(A) Both Assertion (A) and Reason (R) are true, and Reason (R) is the correct explanation of Assertion (A).

Question 7.

Assertion (A): On admission of a new partner, Assets and liabilities are revalued.

Reason (R): Assets and liabilities are revalued so as to show the proper financial position of the firm and the capital hold by the partners at the time of admission.

Answer:

(A) Both Assertion (A) and Reason (R) are true, and Reason (R) is the correct explanation of Assertion (A).

Question 8.

Assertion (A): At the time of admission of a partner if there is any General Reserve, Reserve Fund or the balance of Profit & Loss Account appearing in the balance sheet, it should be transferred to old partners’ capital/current accounts in their old profit sharing ratio.

Reason (R): The General reserve, Reserve Fund or the Balance of Profit and Loss Account are the result of the past profits when the new partner was not admitted.

Answer:

(A) Both Assertion (A) and Reason (R) are true, and Reason (R) is the correct explanation of Assertion (A).

Explanation:

All accumulated profits, reserves I need to be written off as they are the result of the past profits of the firm.

![]()

Question 9.

Assertion (A): The treatment of revaluation of assets and reassessment of liabilities is done in same manner as done in case of change in profit sharing ratio.

Reason (R): Revaluation of assets and liabilities is only done when the new partner is admitted.

Answer:

(C) Assertion (A) is true, but Reason (R) is false.

Explanation:

Revaluation of assets and liabilities is done when a partner is admitted, retires or dies.

![]()

Question 10.

Assertion (A): Profit or loss on revaluation of assets and reassessment of liabilities is transferred to the old partners’ capital/current accounts in old profit sharing ratio.

Reason (R): All the accumulated profit or loss and reserves are transferred to the old partners’ capital/ current accounts in old profit sharing ratio.

Answer:

(B) Both Assertion (A) and Reason (R) are true, but Reason (R) is not the correct explanation of Assertion (A).

Explanation:

Profit or loss on revaluation of assets and reassessment of liabilities is transferred to the old partners’ capital/current accounts in old profit sharing ratio, as it is a result of the under or over valuation of the old I partners but it is not an accumulated profit.

Question 11.

Assertion (A): If goodwill is not brought in cash, it can be adjusted only through the new partner’s capital account.

Reason (R): The adjustment will reduce the capital of the partner.

Answer:

(D) Assertion (A) is false, but Reason (R) is true.

Explanation:

If goodwill is not brought in cash, it can be adjusted through the new partner’s capital account or current account as the case may be.

![]()

I. Read the following hypothetical text and answer the given questions:

Amit and Mahesh were partners in a fast – food corner sharing profits and losses in ratio 3 : 2. They sold fast food items across the counter and did home delivery too. Their initial fixed capital contribution was ₹ 1,20,000 and ₹ 80,000 respectively. At the end of first year their profit was ₹ 1,20,000 before allowing the remuneration of ₹ 3,000 per quarter to Amit and ₹ 2,000 per half year to Ranju. Such a promising performance for first year was encouraging, therefore, they decided to expand the area of operations.

For this purpose, they needed a delivery van, a few Scotties and an additional person to support. Six months into the accounting year they decided to admit Sundram as a new partner and offered him 20% as a share of profits along with monthly remuneration of ₹ 2,500. Sundram was asked to introduce ₹ 30,000 for capital and ₹ 70,000 for premium for goodwill. Besides this Sundram was required to provide ₹ 1,00,000 as loan for two years. Sundram readily accepted the offer. The terms of the offer were duly executed and he was admitted as a partner. [CBSE QB 2021]

Question 1.

Remuneration will be transferred to of Amit and Mahesh at the end of the accounting period.

(A) Capital account

(B) Loan account

(C) Current account

(D) None of the above

Answer:

(C) Current account

Explanation:

Parners are following Fixed Capital Method.

![]()

Question 2.

Upon the admission of Sundram, the sacrifice for providing his share of profits would be done:

(A) by Amit only

(B) by Mahesh only

(C) by Amit and Mahesh equally

(D) by Amit and Mahesh in the ratio of 3 : 2.

Answer:

(D) by Amit and Mahesh in the ratio of 3 : 2.

Explanation:

The sacrifice ratio will be same as the profit sharing ratio.

Question 3.

Sundram will be entitled to a remuneration of at the end of the year.

(A) ₹ 15,000

(B) ₹ 27,000

(C) ₹ 30,000

(D) ₹ 45,000

Answer:

(A) ₹ 15,000

Explanation:

Amit’s Remuneration : ₹ 2,500 monthly ₹ 2,500 x 6 = ₹15,000

![]()

Question 4.

While taking up the accounting procedure for this reconstitution the accountant of the firm Mr. Suraj Marwah faced a difficulty. Solve it be answering the following: For the amount of loan that Sundram has agreed to provide, he is entitled to interest thereon at the rate of …………….

(A) 12%

(B) 6%

(C) 5%

(D) 10%

Answer:

(B) 6%

Explanation:

If partnership deed is absent, then the partner is eligible for a 6% interest on loan on the firm.

II. Based on the below information, you are required to answer the given questions:

Sterling Enterprises is a partnership business with Ryan, Williams and Sania as partners engaged in production and sales of electrical items and equipment. Their capital contributions were ₹ 50,00,000, ₹ 50,00,000 and ₹ 80,00,000 respectively with the profit the sharing ratio of 5 : 5 : 8. As they are now looking forward to expanding their business, it was decided that they would bring in sufficient cash to double their respective capitals.

![]()

This was duly followed by Ryan and Williams but due to unavoidable reasons Sania could not do so and ultimately it was agreed that to bridge the shortfall in the required capital a new partner should be admitted who would bring in the amount that Sania could not bring and that the new partner would get share of profits equal to half of Sania’s share which would be sacrificed by Sania only. Consequent to this agreement Ejaz was admitted and he brought in the required capital and ₹ 30,00,000 as premium for goodwill.

Question 1.

What will be the new profit-sharing ratio of Ryan, Williams, Sania and Ejaz?

(A) 1 : 1 : 1 : 1

(B) 5 : 5 : 8 : 8

(C) 5 : 5 : 4 : 4

(D) None of these

Answer:

(C) 5 : 5 : 4 : 4

Explanation:

New share of Ryan = \(\frac {5}{18}\)

New share of William = \(\frac {5}{18}\)

New share of Sania = \(\frac {8}{18}\) x \(\frac {1}{2}\) = \(\frac {4}{18}\)

Share of Ejaz = \(\frac {8}{18}\) x \(\frac {1}{2}\) = \(\frac {4}{18}\)

New profit sharing ratio of Ryan, Williams,

Sania and Ejaz = \(\frac {5}{18}\) : \(\frac {5}{18}\) : \(\frac {4}{18}\) : \(\frac {4}{18}\) or 5 : 5 : 4 : 4

Question 2.

What is the amount of capital brought in by the new partner Ejaz?

(A) ₹ 50,00,000

(B) ₹ 80,00,000

(C) ₹ 40,00,000

(D) ₹ 30,00,000

Answer:

(B) ₹ 80,00,000

Explanation:

Sania had to bring additional capital so that her capital would be doubled.

It means she had to bring ₹ 80,00,000. She could not bring her additional capital which was brought in by new partner. Hence capital brought in by Ejaz is also ₹ 80,00,000

![]()

Question 3.

What is the value of the goodwill of the firm?

(A) ₹ 1,35,00,000

(B) ₹ 30,00,000

(C) ₹ 1,50,00,000

(D) Cannot be determined from the given data.

Answer:

(A) ₹ 1,35,00,000

Explanation:

Goodwill for – part = 30,00,000

(goodwill brought in by Ejaz for \(\frac {4}{18}\) part)

Total goodwill of the firm = 30,00,000 x \(\frac {18}{4}\) = 1,35,00,000

Question 4.

What will be correct journal entry for distribution of Premium for Goodwill brought in by Ejaz?

| (A) Ejaz Capital A/c Dr. To Sania’s Capital A/c (Being …………) | 30,00,000 | 30,00,000 |

| (B) Premium for Goodwill A/c Dr. To Sania’s Capital A/c (Being ………….) | 30,00,000 | 30,00,000 |

| (C) Premium for Goodwill A/c…… Dr. To Reyan’s Capital A/c To William’s Capital A/c To Ejaz’s Capital A/c (Being …………) | 30,00,000 | 8,33,333 8,33,333 13,33,333 |

| (D) Premium for Goodwill A/c…… Dr. To Reyan’s Capital A/c To William’s Capital A/c To Ejaz’s Capital A/c (Being ………..) | 30,00,000 | 10,00,000 10,00,000 10,00,000 |

Answer:

Option (B) is correct

Explanation:

As only Sania is sacrificing. So, the amount of goodwill brought in by the new partner will be credited to the Sania’s capital account.

III. Based on the below information, answer the given questions:

Aditi and Parul are partners in a firm with capitals of ₹ 35,000 each. They shared profits and losses in the ratio of 3 : 1. On 1st April, 2017, they admit Chanda into their partnership with l/5 th share in the profits. Chanda brings in ₹ 40,000 as her capital and her share of goodwill in cash. Her share of goodwill is calculated on the basis of her capital contribution and her share of profits in the firm. At the time of Chanda’s admission:

(a) The firm had a Workmen Compensation Reserve of ₹ 60,000 against which there was a claim of ₹ 20,000.

(b) Creditors of ₹ 8,000 were paid by Aditi privately for which she is not to be reimbursed.

(c) There was no change in the value of other assets and liabilities.

![]()

Question 1.

What is the value of goodwill to be contributed by Chanda?

(A) ₹ 8,400

(B) ₹ 4,000

(C) ₹ 8,000

(D) ₹ 4,200

Answer:

(A) ₹ 8,400

Explanation:

I. Capitalised Value of the business/Net worth (including Goodwill)

Total Capital of the firm based on Chanda’s capital = 5 x ₹ 40,000 = ₹ 2,00,000

II. Net worth of the business (excluding Goodwill) adjusted capital of all the partners:

Aditi = ₹ (35,000 + 30,000 + 6,000) = ₹ 71,000

Parul = ₹ (35,000 + 10,000 + 2,000) = ₹ 47,000

Chanda = ₹ 40,000

Total Capital = ₹ 1,58,000

III. Hidden Goodwill of the firm (A – B) = 42,000

Chanda’s Goodwill = 1/5 of ₹ 42,000 = ₹ 8,400

Question 2.

What is the amount of goodwill to be transferred to Aditi’s Capital Account?

(A) ₹ 2,100

(B) ₹ 6,300

(C) ₹ 8,400

(D) None of these

Answer:

(B) ₹ 6,300

Explanation:

\(\frac {3}{4}\) of ₹ 8400 = ₹ 6,300

![]()

Question 3.

How much amount of workmen compensation reserve will be transferred to Parul’s Capital Account?

(A) ₹ 30,000

(B) ₹ 10,000

(C) ₹ 15,000

(D) ₹ 20,000

Answer:

(B) ₹ 10,000

Explanation:

\(\frac {1}{4}\) of (₹ 60,000 – ₹ 20,000) = ₹ 10,000

Question 4.

In which account will the gain on creditor’s account be transferred?

(A) Realisation Account

(B) Revaluation Account

(C) Aditi’s Capital Account

(D) Parul’s Capital Account

Answer:

(B) Revaluation Account