Cash Flow Statement Class 12 MCQs Questions with Answers

Cash Flow Statement MCQ Class 12 Question 1.

Which of the following is not an investing cash flow?

(A) Purchase of marketable securities for ₹ 25,000 cash

(B) Sales of land for ₹ 28,000 cash

(C) Sale of 2,500 shares (held as an investment) for ₹ 15 each

(D) Purchase of equipment for ₹ 500 cash

Answer:

(A) Purchase of marketable securities for ₹ 25,000 cash

Explanation:

Purchase of marketable securities is considered as cash and cash equivalents and so does not form the part of investing cash flow.

![]()

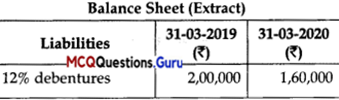

MCQ On Cash Flow Statement Class 12 Question 2.

Additional Information

Interest on debentures is paid on half yearly basis on 30th September and 31st March each year. Debentures were redeemed on 30th September, 2019.

How much amount (related to above information) will be shown in Financing Activity for Cash Flow Statement prepared on 31st March, 2020?

(A) Outflow ₹ 40,000

(B) Inflow ₹ 42,600

(C) Outflow ₹ 61,600

(D) Outflow ₹ 64,000

Answer:

(C) Outflow ₹ 61,600

Explanation:

Cash flow from financing activities :

Interest on debentures

= 1,60,000 x \(\frac {12}{100}\) + 40,000 x \(\frac {12}{100}\) x \(\frac {6}{100}\)

= ₹ 19,200 + ₹ 2,400

= ₹ 21,600

Cash Flow Statement On MCQ Class 12 Question 3.

Which of the following transactions will result into ‘Inflow of Cash’ ?

(A) Deposited ₹ 10,000 into bank

(B) Withdrew cash from bank ₹ 14,500

(C) Sale of machinery of the book value of ₹ 74,000 at a loss of ₹ 9,000

(D) Converted ₹ 2,00,000 9% debentures into equity shares

Answer:

(C) Sale of machinery of the book value of ₹ 74,000 at a loss of ₹ 9,000

Explanation:

Inflow of cash will be ₹ 65,000.

![]()

MCQ On Cash Flow Statement Class 12 Chapter 11 Question 4.

Which of the following transactions will not result into flow of cash?

(A) Issue of equity shares of ₹ 1,00,000

(B) Purchase of machinery of ₹ 1,75,000

(C) Redemption of 9% debentures ₹ 3,50,000

(D) Cash deposited into bank ₹ 15,000

Answer:

(D) Cash deposited into bank ₹ 15,000

Explanation:

Cash deposited into bank is simply the movement between items of cash and cash equivalents.

Cash Flow MCQ Class 12 Chapter 11 Question 5.

Cash Flow Statement is based upon :

(A) Accrual basis of accounting

(B) Cash basis of accounting

(C) Accounting equation

(D) None of the above

Answer:

(B) Cash basis of accounting

Explanation:

Cash flow statement is based on the cash basis of accounting as it only shows the movement of cash.

![]()

Cash Flow Statement MCQ Questions And Answers Pdf Class 12 Question 6.

Payment of income tax is classified under :

(A) Operating activity

(B) Financing activity

(C) Investing activity

(D) None of the above

Answer:

(A) Operating activity

Explanation:

Income tax is paid as a matter of operation of business, so it is classified under Operating Activity.

Question 7.

Dividend received by other than financial enterprise is shown in cash flow statement under :

(A) Operating activity

(B) Financing activity

(C) Investing activity

(D) None of the above

Answer:

(C) Investing activity

Explanation:

Dividend is received as a part of investment done, thus it is shown on the investing activity in the cash flow statement.

Question 8.

Dividend received by financial enterprise is shown in cash flow statement under :

(A) Operating activity

(B) Financing activity

(C) Investing activity

(D) None of these

Answer:

(A) Operating activity

Explanation:

As purchase and sale of securities giving out of loans and advances is a principle business activity of the financial enterprises, it is shown under the Operating Activity in the cash flow statement.

![]()

Question 9.

Pick the odd one out :

(A) Issue of shares in cash

(B) Issue of debentures in cash

(C) Proceeds from long-term loans

(D) Cash received as royalty

Answer:

(D) Cash received as royalty

Explanation:

Cash received as royalty comes under the head of operating activities and rest are in financing activities.

Question 10.

Pick the odd one out:

(A) Cash in hand

(B) Cash at bank ‘

(C) Marketable Securities

(D) Non-current Investments

Answer:

(D) Non-current Investments

Explanation:

Non-current investments is odd as it is the only one which is not a cash and a cash equivalent.

![]()

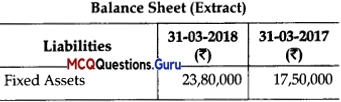

Question 11.

Additional Information:

Depreciation on fixed assets was ₹ 2,00,000 for the year. How much amount for ‘Purchase of fixed assets’ will be shown in investing activity for cash flow statement prepared on 31st March, 2018 ?

(A) Outflow ₹ 8,30,000

(B) Inflow ₹ 42,600

(C) Outflow ₹ 6,30,000

(D) None of these

Answer:

(A) Outflow ₹ 8,30,000

Explanation:

Cash Outflow = Value of Fixed Assets on 31/3/2018 – Value of Fixed asset on 31/03/2017 + Depreciation = ₹ 23,80,000 – ₹ 17,50,000 + ₹ 2,00,000 = ₹ 8,30,000

Assertion And Reason Based MCQs

Directions: In the following questions, a statement of Assertion (A) is followed by a statement of Reason (R). Mark the correct choice as:

(A) Both Assertion (A) and Reason (R) are true, and Reason (R) is the correct explanation of Assertion (A).

(B) Both Assertion (A) and Reason (R) are true, but Reason (R) is not the correct explanation of Assertion (A).

(C) Assertion (A) is true, but Reason (R) is false .

(D) Assertion (A) is false, but Reason (R) is true.

Question 1.

Assertion (A): Depreciation is added to the net profit before tax.

Reason (R): Depreciation is a non-cash item which is an expense.

Answer:

(A) Both Assertion (A) and Reason (R) are true, and Reason (R) is the correct explanation of Assertion (A).

Explanation:

There was cash outflow for de-predation.

![]()

Question 2.

Assertion (A): By-back of equity shares comes under financing activities.

Reason (R): Financing activities are the activities which result in change in size composition of owner’s capital and borrow of the enterprise from other sources.

Answer:

(A) Both Assertion (A) and Reason (R) are true, and Reason (R) is the correct explanation of Assertion (A).

Question 3.

Assertion (A): Sale of fixed asset is written under the Investing Activities.

Reason (R): Sale of fixed asset leads to inflow of cash.

Answer:

(B) Both Assertion (A) and Reason (R) are true, but Reason (R) is not the correct explanation of Assertion (A).

Explanation:

Investing activities are the acquisition and disposal of long-term assets and other investments not included in cash equivalents.

![]()

Question 4.

Assertion (A): Proceeds from Issue of Shares and Debentures are recorded in Financing Activity.

Reason (R): Issue of shares and debentures are the cash inflow or outflow made to finance the company.

Answer:

(A) Both Assertion (A) and Reason (R) are true, and Reason (R) is the correct explanation of Assertion (A).

Case-Based MCQs

I. Read the following information and answer the given questions:

Krishika an alumni of IIM Ahemdabad initiated her startup Krishika Ltd. in 2018. The profits of Krishika Ltd. in the year 2019-20 after all appropriations was ₹ 31,25,000. This profit was arrived after taking into consideration the following items:

| Particulars | Amount (in ₹) |

| 1. Gain on sale of fixed tangible assets | 12,50,000 |

| 2. Goodwill written off | 7,80,000 |

| 3. Transfer to General Reserve | 8,75,000 |

| 4. Provision for taxation | 4.37,500 |

Additional Information:

| Particulars | 31.3.2020(₹) | 31.3.2019 (₹) |

| Prepaid Expenses | 7,50,000 | 5,00,000 |

| Inventory | 10,50,000 | 8,20,000 |

| Trade Payable | 4,50,000 | 3,50,000 |

| Trade Receivables | 6,20,000 | 5,90,000 |

Question 1.

Net Profit before Tax will be ₹ …………

(A) 22,50,000

(B) 35,62,500

(C) 39,67,500

(D) 44,37,500

Answer:

(D) 44,37,500

Explanation:

Net Profit before Tax = Profit after all Appropriations + Provision for Taxation + Transfer to General Reserve = ₹ 31,25,000 + ₹ 4,37,000 + ₹ 8,75,000 = ₹ 44,37,500

![]()

Question 2.

Operating profit before working capital changes will be ……….

(A) 52,17,500

(B) 64,67,500

(C) 39,67,500

(D) 39,69,500

Answer:

(C) 39,67,500

Explanation:

Operating profit before Working Capital changes = Net Profit before tax – Gain on sale of Fixed tangible assets + Goodwill written off

= ₹ 44,37,500 – ₹ 12,50,000 + ₹ 7,80,000 = ₹ 39,67,500

Question 3.

Cash from operating activities before tax will be ………….

(A) 35,57,500

(B) 40,67,500

(C) 37,87,500

(D) 35,67,300

Answer:

(A) 35,57,500

Explanation:

Cash from Operating Activities before Tax = Operating Profit before Working Capital changes – Increase in Current Assets + Increase in Current liabilities = ₹ 39,67,500 – ₹ 2,50,000 – ₹ 2,30,000 – ₹ 30,000 + ₹ 1,00,000 = ₹ 35,57,500

![]()

Question 4.

Cash flow from Operating Activities will be ₹ ………..

(A) 39,95,000

(B) 31,20,000

(C) 40,67,500

(D) 31,00,000

Answer:

(B) 31,20,000

Explanation:

Cash flow from Operating Activities = Cash from Operating Activities before tax – Tax paid = ₹ 35,57,500 – ₹ 4,37,500 = ₹ 31,20,000

II. Read the following information and answer the given questions:

X Ltd. made a profit of ₹ 5,00,000 after consideration of the following items :

(i) Goodwill written off 5,000

(ii) Depreciation on Fixed Tangible Assets 50,000

(iii) Loss on Sale of Fixed Tangible Assets (Machinery) 20,000

(iv) Provision for Doubtful Debts 10,000

(v) Gain on Sale of Fixed Tangible Assets (Land) 7,500

Additional Information:

| Particulars | 31.3.2019 (₹) | 31.3.2018 (₹) |

| Trade Receivables | 78,800 | 52,000 |

| Prepaid Expenses | 3,000 | 2,000 |

| Trade Payables | 51,000 | 30,000 |

| Expenses Payable | 20,000 | 34,000 |

![]()

Question 1.

How will goodwill written off be adjusted in the cash flow statement?

(A) Added to the Net Profit Before Tax

(B) Subtracted the Net Profit before Tax

(C) Not recorded in the Cash Flow

(D) None of these

Answer:

(A) Added to the Net Profit Before Tax

Explanation:

It is a non-cash item and should not form a part of cash flow.

Question 2.

What will be the amount of Trade payables added to get the Cash flow from operations?

(A) ₹ 51,000

(B) ₹ 30,000

(C) ₹ 21,000

(D) ₹ 31,000

Answer:

(C) ₹ 21,000

Explanation:

₹ 51,000 – ₹ 30,000 = ₹ 21,000

Question 3.

What amount of Trade Receivables will be subtracted from the Cash flow Statement to get Cash flow from operations?

(A) ₹ 78,800

(B) ₹ 52,000

(C) ₹ 3,000

(D) ₹ 26,800

Answer:

(D) ₹ 26,800

Explanation:

₹ 78,800 – ₹ 52,000 = ₹ 26,800

![]()

Question 4.

Which of the following items will adjust to Net Profit before Tax?

(A) Trade Receivables

(B) Prepaid Expenses

(C) Loss on sale of Fixed Asset

(D) Expenses Payable

Answer:

(C) Loss on sale of Fixed Asset

Explanation:

It is a non-operating item.

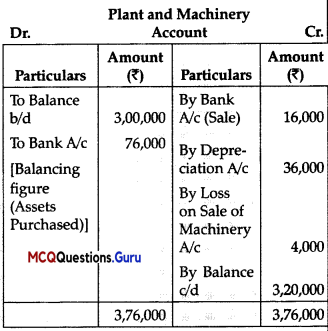

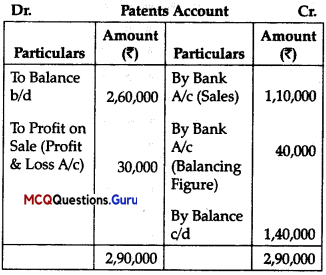

III. Read the following information and answer the questions that follow:

Following are the opening and closing balances of Jayesh Ltd:

| Particulars | Opening Balances (₹) | Closing Balances (₹) |

| Plant & Machinery (at cost) | 3,00,000 | 3,20,000 |

| Accumulated | 90,000 | 1,00,000 |

| Depreciation | 2,60,000 | 1,40,000 |

| Patents | 80,000 | 1,00,000 |

Additional information:

During the year:

(a) Depreciation charged on Plant and Machinery was ₹ 36,000.

(b) A machine having a book value of ₹ 20,000 was sold for ₹ 16,000.

(c) Patents having a book value of ₹ 80,000 were sold for ₹ 1,10,000.

![]()

Question 1.

What amount of Sales proceeds of Plant and Machinery will be added/subtracted?

(A) ₹ 20,000 added

(B) ₹ 20,000 subtracted

(C) ₹ 16,000 added

(D) ₹ 16,000 subtracted

Answer:

(C) ₹ 16,000 added

Explanation:

Question 2.

What amount of machinery was purchased?

(A) ₹ 70,000

(B) ₹ 76,000

(C) ₹ 3,20,000

(D) ₹ 20,000

Answer:

(B) ₹ 76,000

![]()

Question 3.

What amount of patents will be added/subtracted to get the cash flow from the investment?

(A) ₹ 1,50,000 added

(B) ₹ 1,50,000 subtracted

(C) ₹ 1,20,000 added

(D) ₹ 1,20,000 subtracted

Answer:

(A) ₹ 1,50,000 added

Explanation:

![]()

Question 4.

What is the cash flow from investing activities?

(A) ₹ 70,000

(B) ₹ 72,000

(C) ₹ 73,000

(D) ₹ 80,000

Answer:

(A) ₹ 70,000

Explanation:

| Particulars Amount | (₹) |

| Proceeds from Sale of Plant and Machinery | 16,000 |

| Payment for Purchase of Plant and Machinery | (76,000) |

| Proceeds from Sale of Patent (1,10,000 + 40,000) | 1,50,000 |

| Purchase of Goodwill (1,00,000 – 80,000) | (20,000) |