By going through these CBSE Class 12 Accountancy Notes Chapter 7 Issue and Redemption of Debentures, students can recall all the concepts quickly.

Issue and Redemption of Debentures Notes Class 12 Accountancy Chapter 7

In today’s growing business equity sources of financing only are not sufficient to meet the ever-growing needs of corporate expansion and growth. As a result, the companies turn to raise long-term funds by issuing debentures. Debt financing not only helps in reducing the cost of capital but also helps in designing the appropriate capital structure for the company.

Meaning of Debenture: The term, ‘debenture’ has been derived from the Latin word “debre” which means “to borrow”. Thus, it is a written document acknowledging a debt under the common seal of the company and containing a contract for the repayment of the principal sum at a specified date and for the payment of interest (usually half-yearly) at a fixed rate percent until the principal sum is repaid.

→ “Debenture includes debenture stock, bonds and any other securities of a company whether constituting a charge on the assets of the company or not.”- Section 2(12) of the Companies Act, 1956

→ “A debenture is a document given by a company as evidence of a debt to the holder usually arising out of a loan and most commonly secured by a charge.”- Topham

→ “Debenture is a document under company’s seal which provides for the repayment of a principal sum and interest thereon at regular intervals which is usually secured, by a fixed or floating charge on the company’s property and which acknowledges loan of-a company.” – E. Thomas

→ “Debenture means a document which either creates a debt or acknowledges it and any document which fulfills either of these conditions.” -Chitty J.

Bond: Bond, like debenture, is an acknowledgment of debt issued under the seal of a company and signed by an authorized signatory.

Charge: It means securing the loan by encumbering a specific part of assets towards the loan. It means, if the company fails to meet its obligation, the lender can secure his payment from the assets mortgaged or in case of winding up of the company from the official liquidator.

The Companies Act, 1956) requires that all the charges be registered with the Registrar of Companies. Section 125 (4) of the Companies Act, 1956 requires that a charge when created on the following be got registered:

For the purpose of securing any issue of debentures.

- On uncalled share capital of the company.

- On calls made but not paid.

- On any book debts of the company.

- On any immovable property, wherever situated, or any interest therein.

- On a ship or any share in the ship.

- On goodwill, on a patent or a license under a patent, on a trademark or on the copyright or a license under copyright.

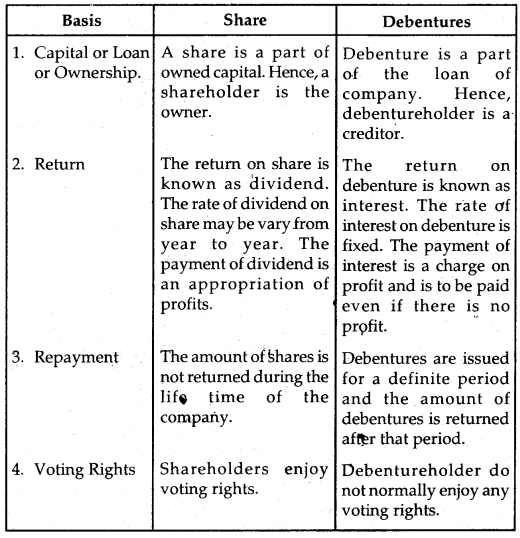

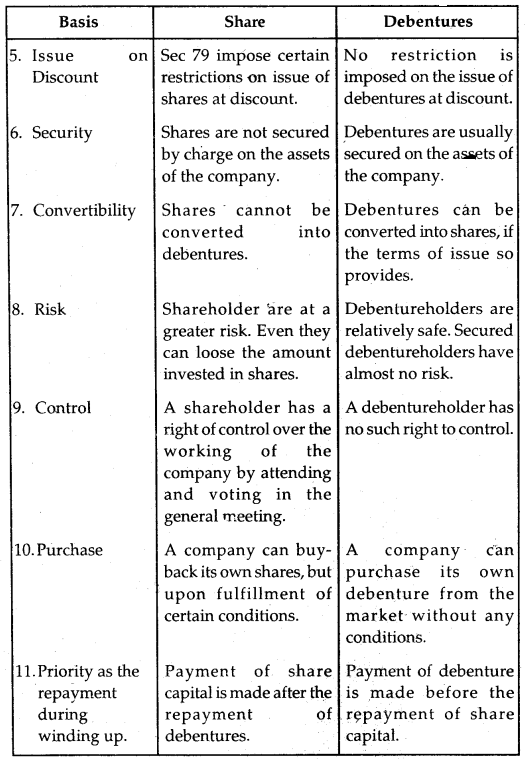

Difference Between Share and Debenture:

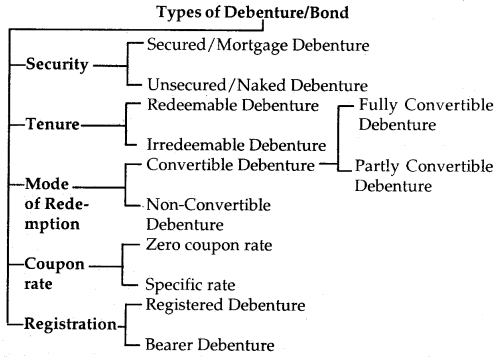

Types of Debentures:

1. Security point of view

(a) Secured/Mortgage Debentures: Secured Debentures are those which are secured either on a particular asset or on all the assets of the company in general.

(b) Unsecured/Naked Debentures: Unsecured Debentures do not have a specific charge on the assets of the company.

2. Tenure point of view:

(a) Redeemable Debentures: Redeemable debentures are those that will be repaid by the company at the end of a specified period during the existence of the company.

(b) Irredeemable Debentures: Irredeemable debentures are those that are not repayable during the lifetime of the company.

3. Mode of Redemption point of view:

(a) Convertible Debentures: Convertible debentures are those the holder of which is given an option of

exchanging the amount of their debenture for equity shares after a specified period.

These are of two types:

- Fully Convertible Debentures (FCD) are those debentures where the whole amount is to be converted into equity shares.

- Partly Convertible Debentures (PCD) are those debentures where only a part of the amount of debenture is convertible into equity shares.

(b) Non-Convertible Debentures: The debentures which cannot be converted into shares or in any other securities are called non-convertible debentures.

4. Coupon Rate point of view:

(a) Zero Coupon Rate Debenture: These debentures do not carry a specific rate of interest.

(b) Specific Coupon Rate Debenture: These debentures are issued with a specified rate of interest, which may either be fixed and floating.

5. Registration point of view:

(a) Registered Debentures: Registered debentures are those which are payable to the persons whose name appears in the Register of Debenture holders. These can be transferred only by executing a transfer deed.

(b) Bearer Debentures: Bearer debentures are those which are payable to the bearer thereof. These can be transferred merely by delivery. Interest is paid to the persons who produced the interest coupon attached to such debenture.

Issue of Debentures: Debentures can be issued at par, at a premium, or at a discount. They can also be issued for consideration other than cash or as Collateral Security. Accounting treatment regarding the issue of debenture is done in the same manner as in the case of the issue of share. The only difference is that ‘Debenture’ in place of ‘Share’ and ‘Debenture A/e’ in place of ‘Share Capital A/c’ is substituted.

Issue of Debentures at Par: Debentures are said to have been issued at par when the issue price is equal to their face value.

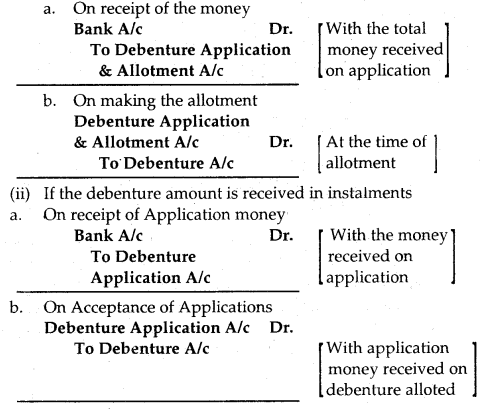

1. If the debenture amount is received in one installment (lump sum).

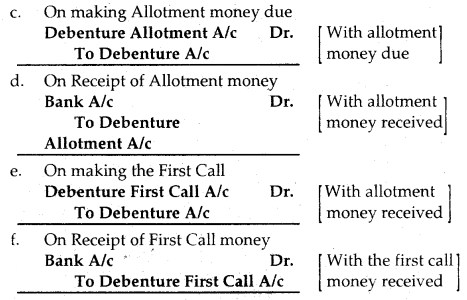

Similar entries like e, f may be made for the second call and final call.

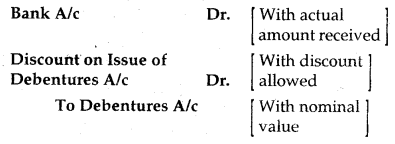

Issue of Debentures at a Discount: When the debentures are issued at less than the face value, it is said to be issued at discount. Discount on issue of debenture is a capital loss and is shown on the assets side of the Balance Sheet under the head “Miscellaneous Expenditure” till it is written off.

Accounting Treatment:

On the issue of debentures at a discount

Debenture Allotment A/c Dr.

Discount of Issue of Debenture A/c Dr.

To Debenture A/c

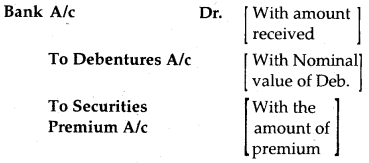

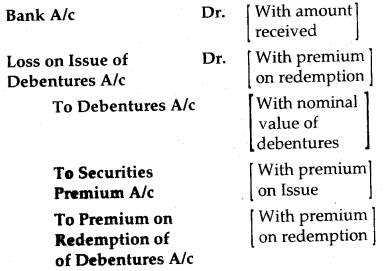

Issue of Debentures at Premium: A debenture is said to have been issued at a premium when the price charged is more than the face value of debenture. Premium on Issue of Debenture represents a capital receipt and should be transferred to Securities Premium A/c. It can be used for writing off capital losses and fictitious assets. This account is shown on the liabilities side of the Balance Sheet under the head of ‘Reserves & Surplus’.

Accounting Treatment:

On Issue of Debenture at Premium

Debenture Allotment A/c Dr.

To Debenture A/c To Securities Premium A/c

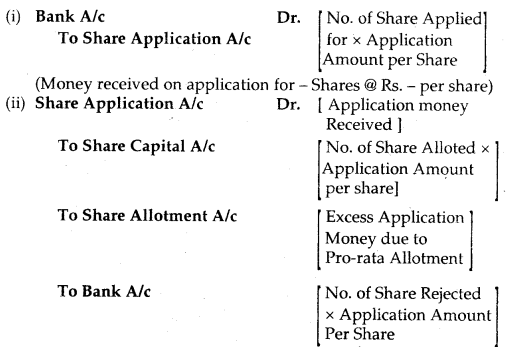

Over Subscription: When the number of debentures applied for is more than the number of debentures offered to the public, the issue is said to be oversubscribed. The excess money received on oversubscription may be retained for adjustment towards allotment and respective calls when the amount is payable in Instalments or excess money will be refunded.

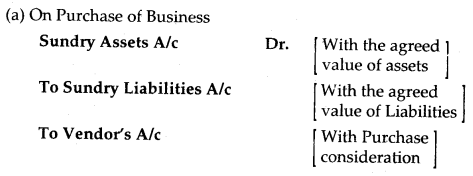

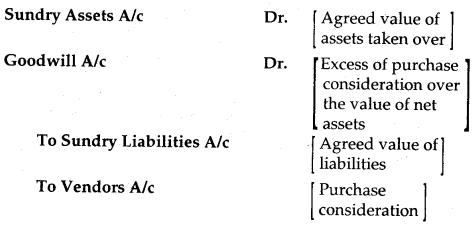

Issue of Debentures for Consideration Other than Cash: When the company purchases some assets (including services) and instead of making the payment to the supplier in the form of cash, issues its fully paid debentures, such issue of debentures is called the Issue of Debentures for Consideration Other than Cash. Such debentures can be issued at par, a premium, or at a discount.

If the purchase consideration is greater than the value of the net assets acquired (i.e., the difference between the agreed value of the assets taken over and the agreed value of liabilities taken over), the difference is treated as a capital loss which should be debited to Goodwill A/c.

Or

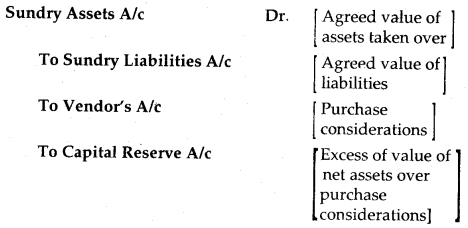

If the amount of the purchase consideration is lower than the value of the net assets acquired, the difference is treated as a capital profit which should be credited to Capital Reserve A/c.

(b) On the issue of Debentures

1. At par

Vendor’s A/c Dr.

To Debentures A/c

2. At Premium

Vendor’s A/c Dr.

To Debentures A/c To Securities Premium A/c

3. At a Discount Vendor’s A/c

Discount on Issue of Debentures A/c

To Debentures A/c

No. of Debentures issued = \(\)\(\)

Issue Price of a Debenture:

Issue of Debentures as Collateral Security: When a company takes a loan from a bank or any other party and gives some additional security in the shape of debentures, the debentures are said to be issued as collateral security. In such a case, the lender has the absolute right over the debentures unless and until the loan is repaid. On repayment of the loan, the lender is legally bond to release the debenture forthwith.

In case the loan is not repaid by the company on the due date, the lender has the right to retain these debentures and realize them. The holder of such debentures is entitled to interest only on the amount of loan, but not on the debentures.

Debentures issued as collateral security can be dealt with in two ways in the books.

1. No accounting entry is required to be shown in the books at the time of issue of such debentures, but a footnote to the fact that the loan has been secured by the issue of debentures is appended.

2. If it is desired that such an issue of debentures is to be recorded in the books, the following entries are recorded:

(a) On the issue of Debentures as Collateral Security

Debentures Suspense A/c Dr.

To Debentures A/c

(b) On repayment of the loan

Debentures A/c Dr.

To Debentures Suspense A/c The net effect of the above two entries is nil.

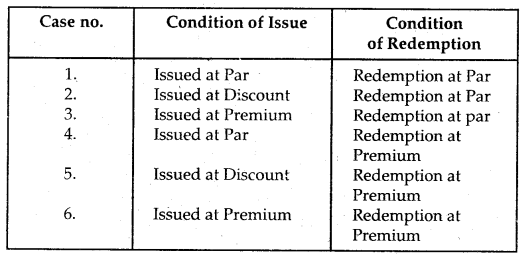

Issue of Debentures From Condition of Redemption Point of View: Redemption of debentures means discharge of liability on account of debentures by repayment made to the debenture holders. Depending upon the terms and conditions of issue and redemption of debentures, there may be the following six cases:

Accounting Treatment:

Case 1: Issue at Par and Redemption at Par

Case 2: Issue at Discount and Redemption at Par

Case 3: Issue at Premium and Redemption at Par.

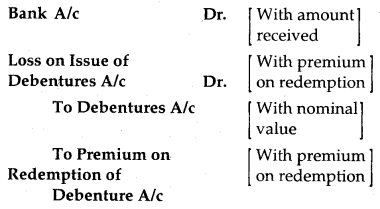

Case 4: Issue at Par and Redemption at Premium

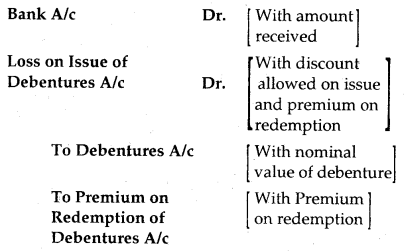

Case 5: Issue at Discount and Redemption at Premium

Case 6: Issued at Premium and Redemption at Premium

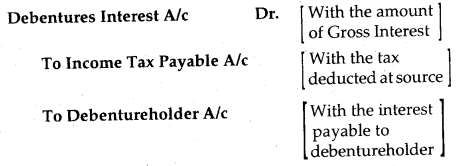

Interest on Debentures: Interest on debentures is a charge against the profits of the company and is payable irrespective of the fact whether there are profits or not. It is calculated on the face value of the debenture. According to Income-tax Act, 1961, the company must deduct income tax at the prescribed rate from the gross amount of interest payable on debenture before the annual amount is paid to debenture holders. Accounting Treatment:

1. For Interest due

2. For Payment of Interest

Debentureholder A/c Dr.

To Bank A/c

3. On Closing of Debenture Interest A/c

Profit and Loss A/c Dr.

To Debenture Interest A/c

4. For Payment of Income Tax to Government

Income Tax Payable A/c Dr.

To Bank A/c

Writing off Discount/Loss on Issue of Debentures: The discount/ loss on the issue of debentures is a capital loss and therefore must be written off during the lifetime of debentures. The discount/loss on the issue of debentures is shown under the head “Miscellaneous Expenditure” on the assets side of the Balance Sheet. Section 78 of the Companies Act, 1956 permits the utilization of Securities Premium for writing off the discount/loss on the issue of the debenture.

Entry is following:

Security Premium A/c Dr.

To Discount/Loss on

Issue of Debenture A/c

In case there are no capital profits or if the capital profits are not adequate, the amount of such discount/loss can be written off by utilizing the revenue profits.

There are two methods, which can be used to write off the Discount/Loss on the issue of debentures:

(a) Fixed Installment Method: When the debentures are redeemed at the end of a specified period, the total amount of discount should be written off in equal installments of a fixed amount over the period.

(b) Fluctuating Installment Method: When debentures are repaid by annual drawings or installments, the discount is written off in the ratio of debentures outstanding before redemption. The amount of discount, in this method, goes on reducing every year as a greater amount is used in the initial years than the later years. This method is also known as the Reducing Instalment Method.

Section-II

Redemption of Debentures: Redemption of debentures means repayment of the loan due on debentures to debenture holders. According to Section 117 C (3) of the Companies Act 1956, the debentures should be redeemed in accordance with the terms and conditions of their issue/ offer documents. The date, the terms, and the conditions are generally stated in the debenture certificate itself or in the trust deed.

On the due date or happening of the circumstances so specified, the company becomes liable to pay the principal amount to the debenture holder. A company may purchase its own debenture which then stands canceled.

In other words, the redemption of debentures means repayment of the number of debentures by the company. There are three aspects that a company should bear in mind regarding redemption namely the time of redemption, the amount to pay, and the sources from which redemption will have to be carried out.

Methods of the Redemption of Debentures: The various methods of redemption of debentures are as under:

- Payment in Lump-Sum

- Payment in Instalments

- Purchase in Open Market

- Conversion of existing Debenture into Shares or New Debentures.

1. Payment in Lump Sum: It means debentures can be redeemed by paying the debenture holders in one lump sum at the expiry of the agreed time or earlier at the option of the company. In this case, the time of repayment is known in advance and thus the company can plan its financial resources accordingly.

2. Payment in Instalments: It means the redemption is made in annual installments. The amount of installment is worked out by dividing the total amount of debentures by the number of years it is to last. The number of debentures to be redeemed each year are selected by lottery. Thus, it is also known as drawing by lottery or draw of lots.

3. Purchase in Open Market: A company, if authorized by its Articles of Association, can purchase its own debenture in the open market. Debentures so purchased may be canceled and it means the debentures have been paid.

4. Conversion of Existing Debentures into Shares or New Debentures: It means the debenture holder can exchange their debenture either for shares or new debentures of the company and the debentures which carry such right are called convertible debentures.

Sources of funds for Redemption of Debentures: The redemption of debentures can be done either out of capital or out of profits.

(a) Redemption of Debenture out of Capital: In this case, profits of the company are not utilized for the redemption of debentures, so the assets of the company are reduced by the amount paid. Normally the profits are transferred to Debenture Redemption Reserve for redemption. In case no profits have been transferred to Debenture Redemption Reserve and debentures are redeemed on the due date, it is regarded as redemption out of the capital. It is, however, presumed that the company has adequate funds to redeem the debentures.

Accounting Treatment:

(a) If debentures are to be redeemed at par

1. On debentures becoming due

Debentures A/c Dr.

To Debenture- holder A/c

2. On Redemption Debentureholder A/c Dr.

To Bank A/c

(b) If debentures are to be redeemed at a premium

1. On debentures becoming due

Debentures A/c Dr.

Premium on Redemption of

Debenture A/c Dr.

To Debentureholder A/c

2. On Redemption Debentureholder A/c Dr.

To Bank A/c

(b) Redemption of Debentures out of Profits: Redemption of debentures out of profits means the amount equal to that utilized for repayment to debenture holders is transferred from Profit and Loss Appropriation A/c to a newly opened A/c called ‘Debenture Redemption Reserve A/c’ (DRR). The portion of the profits set aside may either be retained in the business or maybe invested.

The Companies Act (Amendment), 2000 has introduced Section 117 C which provides as under:

(a) Where company-issued debentures after the commencement of this act, it shall create a DRR for the redemption of such debentures, to which adequate amount shall be credited, from out of its profits every year until such debentures are redeemed.

(b) The amount credited to the DRR shall not be utilized by the company except for the purpose of the redemption of debentures.

SEBI’s Guidelines: Securities and Exchange Board of India (SEBI) has provided some guidelines for the redemption of debentures. The focal points of these guidelines are:

- Every company shall create a venture Redemption Reserve in case of issue of debenture redeemable after a period of more than 18 months from the date of issue.

- The creation of Debenture Redemption Reserve is obligatory only for non-convertible debentures and a non-convertible portion of partly convertible debentures.

- A company shall create a Debenture Redemption Reserve equivalent to at least 50% of the amount of debenture issue before starting the redemption of the debenture.

- Withdrawal from Debenture Redemption Reserve is permissible only after 10% of the debenture liability has already been reduced by the company.

Exemption: SEBI guidelines would not apply under the following situations:

(a) Infrastructure company (a company wholly Engaged in the business of developing, maintaining, and operating infrastructure facilities.)

(b) A company issuing debentures with a maturity period of not more than 18 months.

Clarifications regarding Debenture Redemption Reserve:

The Department of Company Affairs, Government of India, vide their circular No. 9/2002, dates 18.04.2002 has issued the following clarifications regarding the creation of Debenture Redemption Reserve (DRR):

(a) No DRR is required for debentures issued by All India Financial Institutions, by RBI and, Banking Companies for both public as well as privately placed debentures.

(b) No DRR is required in case of privately placed debentures.

(c) Section 117c will apply to debentures issued and pending to be redeemed and, therefore, DRR will also be created for debentures issued prior to 13.12.2000 and pending redemption.

(d) Section 117c will apply to the non-convertible portion of debentures issued whether they are fully or partly paid.

Journal Entries:

- Debenture A/c To Debentureholders A/c

- Debenture holder A/c To Bank A/c

- Profit and Loss Appropriation A/c To Debenture Redemption Reserve A/c

DRR A/c appears on the liability side of the Balance Sheet, under the head “Reserves and Surplus”. The balance in DRR A/c increases with each redemption. When all the debentures are redeemed, the DRR A/c is closed by transferring its balance to General Reserve A/c.

Redemption by Purchase in the Open Market: A company, if authorized by its Articles of Association, can redeem its own debenture by purchasing them in the open market.

If a company purchases its own debenture for the purpose of immediate cancellation, the purchase and cancellation of such debenture are called, redemption by purchase in the open market.

Advantages:

- A company can redeem the debentures at its convenience whenever it has surplus funds.

- A company can save money by purchasing its own debenture when they are available in the market at discount.

Accounting Treatment:

(In case of Profits)

(a) On purchase of own debentures for immediate cancellation.

Debenture A/c Dr.

To Bank A/c

To Profit on Cancellation of Debenture A/c

(b) On transfer of Profit on Redemption

Profit on Cancellation of Debenture A/c Dr.

To Capital Reserve A/c

(In case of Loss)

(a) On purchase of own debenture for immediate cancellation.

Debenture A/c Dr.

Loss on Cancellation

of Debenture A/c Dr.

To Bank A/c

(b) On transfer of Loss on Redemption

Profit and Loss A/c Dr.

To Loss on Cancellation of Debenture A/c

Redemption by Conversion: Sometimes, at the time of issue of debentures, a company gives the convertible debenture holders the privilege that they can get their debentures converted into shares or new debentures after the expiry of a specified period. Whenever debenture is redeemed by conversion, the debenture holders have to.; apply for the same. The new shares or debentures may be issued at par, discount, or a premium.

No DRR is required in case of convertible debentures because no funds are required for redemption.

If debentures to be converted were issued at discount, the issue price of the share must be equal to the amount actually received from debentures. If this rule is not followed, it would be a violation of section 79 of the Companies Act, 1956.

Accounting Treatment:

(i) For the amount due to debenture holders

(a) If Redemption at par

Debentures A/c Dr.

To Debentureholder A/c

Or

If Redemption at a premium

Debentures A/c Dr.

Securities Premium A/c Dr.

To Debentureholder A/c

(b) For discharging obligation by issuing shares or debentures

Debentureholder A/c Dr.

To Equity Share Capital

Or

To Debentures A/c (New)

If the new shares/debentures are issued at a premium, the Securities Premium A/c is credited or new shares/debentures are issued at a discount, the Discount on Issue of Shares/Debentures A/c is debited in the above-mentioned entry (b).

Sinking Fund Method: The amount required for the redemption of debentures is generally large and the date of redemption is known to the company. Thus, it is prudent for a company to make arrangements to ensure the availability of adequate funds for the redemption of debenture at the end of the stipulated period for which debentures are issued. Hence, it is better for the company to set aside every year a part of divisible profits and to invest the same outside the business in marketable securities.

This is done by creating a Sinking Fund. The company adopts the method of Debenture Redemption Sinking Fund. An appropriate amount calculated by referring to Sinking Fund Factors, depending upon the interest rate on investments and the number of years for which investments are made, is set aside.

Debenture Redemption Sinking Fund A/c will be created every year to provide means for the redemption of debentures. The company sets aside every year a certain sum of money out of its profits and invests the same along with the interest that may be earned on an investment. The investment is sold when debentures fall due for redemption. The amount available from the sale of investment is utilized for the redemption of debentures.

Accounting Treatment:

I. At the end of First Year

(a) For setting aside the amount out of Profit

(b) For Investing the amount set aside

II. At the end of the second year and subsequent years other than the last year.

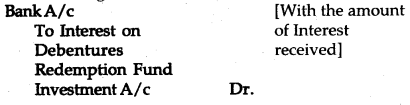

(a) For Receiving the Interest on Investments made

(b) For the transfer of Interest on Deb. Red. Fund Investment to DRF A/c

The interest of Deb. Red

Fund Investment A/c Dr.

To Debenture Redemption Fund A/c

(c) For Setting aside the number of profits

Profit and Loss Dr. [With the amount

Appropriation A/c of Profit set aside]

To Debenture Redemption FundA/c

(d) For Investing the amount set aside along with interest • received.

Deb. Red. Fund Investment A/c Dr.

ToBank A/c

III. At the end of last year

(a) For Receiving the Interest on Investment made

Bank A/c Dr.

To Interest on Deb. Red. Fund Investment A/c

(b) For the transfer of Interest on Deb. Red. Fund Investment to DRF A/c

Interest in Deb. Red.

Fund Investment A/c Dr.

To Deb. Red. Fund A/c

(c) For setting aside the number of profits

Profit & Loss

Appropriation A/c Dr.

To Deb. Red. Fund A/c

(d) For Realising the Investment made

Bank A/c Dr. [With the sale

To Deb. Red. Fund proceeds]

Investment A / c

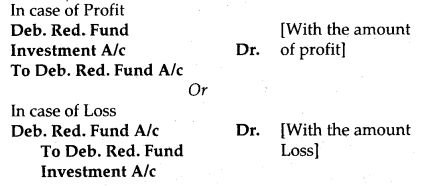

(e) For the transfer of profit/loss on realization of Deb. Red. Fund Investments

(f) For the amount due to debenture holders

Debenture A/c Dr.

To Debentureholders A/c

(g) For redemption

Debenture holders A/c

To Bank A/c

(h) For the transfer of the balance, if any, Discount on Issue of Debentures A/c/Loss on Issue of Debenture A/c

Deb. Red. Fund. A/c Dr.

To Discount on Issue of Debentures A/c,

To Loss on Issue of Debentures A/c

1. For the transfer of an amount from the Deb. Red. Fund A/c to General Reserve:

(a) If some of the Debentures are redeemed

(b) If all the Debentures are redeemed