By going through these CBSE Class 11 Accountancy Notes Chapter 16 Accounting for Not-for-Profit Organisation, students can recall all the concepts quickly.

Accounting for Not-for-Profit Organisation Notes Class 11 Accountancy Chapter 16

There are certain institution or organization which are set-up not to earn a profit, but for providing service to its members and the public in general. The main aim of these institutions or organizations is rendering service to their members and public, but not the profit as in the case of business. Such organization includes schools, hospitals, clubs, charitable institutions, religious organizations, trade unions, welfare societies, consumer-cooperatives, literary societies, etc.

These organizations or institutions are managed by a group of people known as trustees who are fully accountable to their members and the society for the utilization of funds and the objectives of the organization. So, you have to maintain proper accounts and financial statements in the form of the Receipt and Payment Account, Income and Expenditure Account, and the Balance Sheet. These financial statements help them to keep track of their income and expenditure as well as fulfill the legal requirements for maintaining records.

Meaning of Not-For-Profit Organisation:

All trading and business organizations are profit organizations since their main objective is to earn profit. Not-For-Profit Organisations are those organizations whose main aim/objective is to rendering service to their members or the society at large and not the earning of profits.

These organizations refer to the organizations that are set up for the welfare of the society, as a charitable institution, which runs without profit motive. Its main aim is to provide services to its members. The main source of their income usually is subscriptions from their members, donations, grants, income from investment, etc. These organizations keep the accounting records to meet the statutory requirements and controlling the utilization of their funds. They usually prepare them at the end of the financial year to ascertain their income and expenditure and the financial position of the organization and submit them to the statutory authority i.e. Registrar of Societies.

Characteristics of Not-For-Profit Organisation:

1. Service Motive: The main motive of these organizations is service motive. They provide service either free of cost or at a nominal cost and not to earn profit. These are formed for rendering service to a specific group or society at large such as education, health care, recreation, sports, and so on without any consideration of caste, creed, and color.

2. Organisation: Not-For-Profit Organisations are organized as charitable trusts or societies. The subscribers to such trust or societies are called its members.

3. Management: The affairs of Not-For-Profit Organisations are normally managed by a managing committee or executive committee. These committees are elected by their members or subscribers.

4. Source of Income: The main source of income of these organizations are:

- Subscriptions from members

- Life-membership fees

- Endowment fund

- Donations

- Legacies

- Grant-in-aid

- Income from investments etc.

5. Capital Fund or General Fund: The funds raised by Not-For-Profit Organisations through various sources are credited to capital funds or general funds.

6. Surplus Added to Capital Fund: The surplus generated in the form of excess income over expenditure is simply added to the capital fund or general fund. It is not distributed amongst the members as in trading or business organization.

7. Goodwill: The Not-For-Profit Organisation earn their reputation or goodwill on the basis of their contribution to the welfare of the society rather than on the customers’ satisfaction or owner’s satisfaction.

8. Accounting Records: The accounting records of these organizations are totally different from the trading or business organization. They are not prepared financial statements like Trading Account and Profit & Loss Account, instead, they prepare Receipts and Payment Account and Income and Expenditure Account. The preparation of the Balance Sheet is the same in both organizations.

9. Statutory Requirement: The accounting information provided by such organizations is meant for the present and potential contributors to meet the statutory requirements.

Accounting Records of Not-For-Profit Organisations:

As we know that Not-For-Profit Organisations are not engaged in any trading or business activity normally. Their main source of income are subscriptions, donations, financial assistance or grant from the government, etc. Most of their transactions are in form of cash or through the bank. These organizations are required by law to keep proper accounting records and keep proper control over the utilization of their funds.

For maintaining accounting records these organizations usually keep a cash book to record all receipts and payments and maintain ledger accounts of all income, expenses, assets, and liabilities. In addition, they maintain a stock register to keep records of all fixed assets and consumables.

In place of the capital account, they maintain a capital fund or general fund that goes on the increase due to surpluses, life membership fees, donations, legacies, etc. received from year to year.

Final Accounts or Financial Statements of Not-For-Profit Organisation:

As they are non-profit making entities, so they are not required to make Trading and Profit & Loss Account but instead of these accounts to know whether the income during the year was enough to meet the expenses or not they prepare

- Receipts and Payment Account,

- Income and Expenditure Account, and

- Balance Sheet.

For the preparation of these financial statements, the general principles of accounting are fully applicable. The statements provide the necessary financial information to members, donors, and to the Registrar of Societies.

Along with all these, Not-For-Profit organizations also prepare a trial balance for checking the accuracy of ledger accounts. The trial balance also facilitates the preparation of accurate Receipts and Payment Account as well as the Income and Expenditure Account and the Balance Sheet.

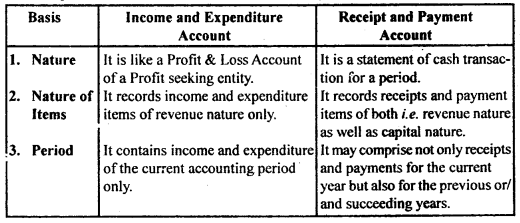

Receipts and Payment Account:

A Receipts and Payment Account is a summary of cash transactions. It is prepared at the end of the accounting period from the cash receipts journal and cash payment journals.

“Receipts and Payment Account is nothing more than a summary of the cash book (Cash and Bank transactions) over a certain period, analyzed and classified under the suitable heading. It is the form of account most commonly adopted by the treasurers of societies, clubs, associations, etc. when preparing the results of the year’s working.” – William Pickles

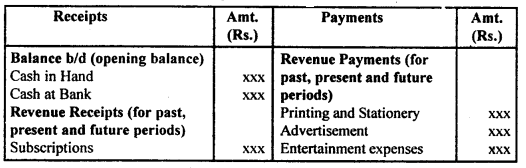

In other words, Receipts and Payment Account simply is a summary’ of cash and bank transactions under various heads. On the debit side, it begins with an opening balance of cash and bank and records all the items of receipts irrespective of whether they are of capital or revenue nature or whether they pertain to the current or past or future accounting periods.

The payments are recorded on the credit side without making any distinction between items of revenue and capital nature and whether they belong to the current or past or future accounting period(s). It may be noted that this account does not show any non-cash item like depreciation. At the end of the period, this account is balanced to ascertain the balance of cash in hand or cash at the bank. The annual totals of various items of receipts and payments are found from their respective accounts in the ledger or from the cash book and are then entered in the Receipts and Payment Account.

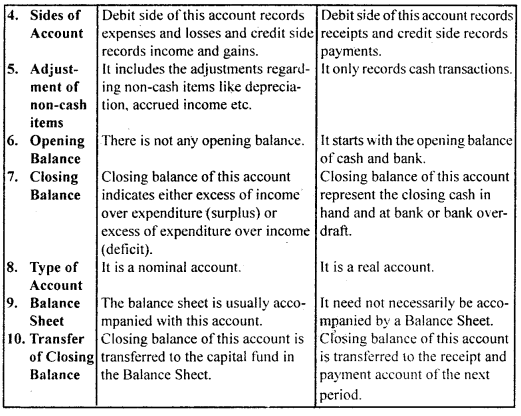

Salient Features of Receipts and Payment Account:

1. Real Account-It is a real account, so the rule of real account. e. ‘Debit what comes in and credit what goes out is followed. Thus receipts are recorded on the Debit side and the payments are recorded on the Credit side.

2. Summary of the Cash Book: It is a summary of the cash book. Its form is similar to cash book (without discount and bank column) with debit and credit sides.

3. Shows amount irrespective of period: It shows the total amount of all receipts and payments irrespective of the period to which they pertain.

4. No distinction between nature (Capital or Revenue nature): It includes all receipts and payments whether they are of capital nature or of revenue nature.

5. No distinction between the mode of the transaction (Cash or Bank): No distinction is made in receipts/payments make cash or through the bank. With the exception of the opening and closing balances, the total amount of each receipt and payment is shown in this account.

6. Do not show non-cash items: Non-cash items like depreciation, outstanding expenses, accrued income, etc. are not shown in this account.

7. Opening and closing balances: The opening and closing balances in it respectively mean cash in hand or cash at the bank in the beginning and at the end. The balance of receipts and payment account must be debit being cash in hand or cash at the bank unless there is a bank overdraft.

8. Does not reflect net income or net loss: This account does not tell us whether the current income exceeds the current expenditure or vice versa or in other words, it does not give any information of net income or a net loss.

Steps in the Preparation of Receipt and Payment Account

1. Put the opening balance of cash in hand and cash at the bank at the beginning on the Receipt side. If there is a bank overdraft at the beginning, but the same in the Payment side of the account.

2. Enter the total amounts of all receipts (either cash or cheque) in the Receipt side (Dr. side) irrespective of their nature (whether capital or revenue) and whether they pertain to past, present, and future periods.

3. Enter the total amounts of all payments (either cash or cheque) in the Payment side (Cr. side) irrespective of their nature (whether capital or revenue) and whether they pertain to past, present, and future periods.

4. Do not enter the non-cash item like depreciation, outstanding expenses, accrued income, etc.

5. Find out the difference between the total debit side and the total credit side of the account and enter the same on the credit side as the closing balance of cash or bank balances.

But, if the total of credit side is more than of debit side, show the difference on the debit as bank overdraft and close the account.

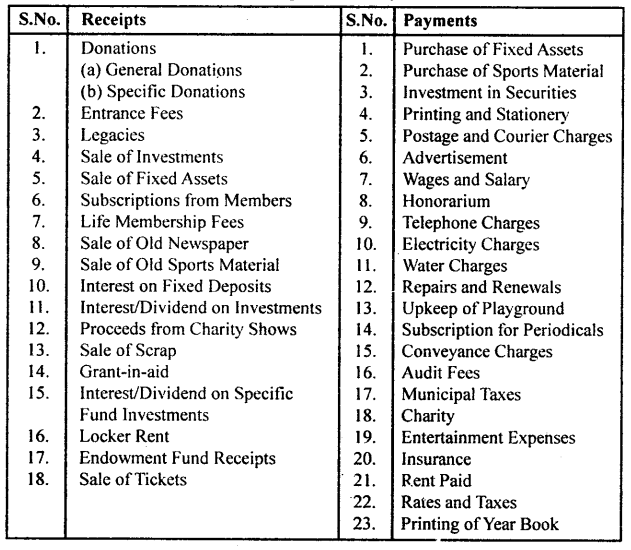

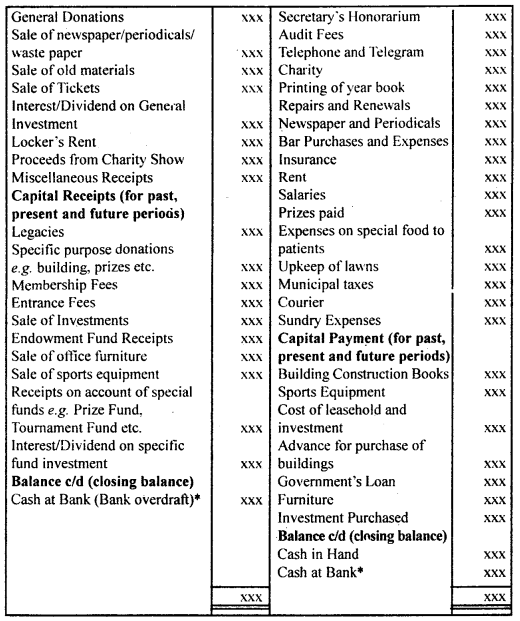

Examples of Important Receipts and Payments Items

Format of Receipts and Payments Account

Receipts and Payments Account

There will be either of the two amounts i.e. cash at a bank or bank overdraft, not both.

Limitations of Receipts and Payments Account:

- It does not show expenses and incomes on an accrual basis.

- It does not show whether the organization is able to meet its day-to-day expenses out of its income.

Income and Expenditure Account:

it is a nominal account of Not-For-Profit Organisation equivalent to the Profit & Loss Account of the grading concerns. The terms profit is substituted by the words excess of income over expenditure (surplus) and the loss is expressed as an excess of expenditure over income (deficit). It reveals the surplus or deficit arising out of the organization’s activities during an accounting period.

This account is prepared on an accrual basis and includes only items of a revert ie nature. All the revenue items placing to the current penned shop in the account, the expenses and losses on the expenditure side (debit side), and incomes and gains on the income side (credit side) of the account. It shows the net operating result in the form of surplus or deficit, which is transferred to the capital fund is shown in the balance sheet.

Salient Features of Income and Expenditure Account:

1. Nominal Account: It is a nominal account, therefore the ride of nominal account i.e. “Debit all expenses and losses and credit all incomes and gains” is followed.

2. Ignore Items of Capital Nature: In this account, only items of revenue nature are to be considered and all the items of capital nature should be ignored.

3. Prepare from Receipt and Payment Account: It is generally prepared from a given Receipts and Payments Account and other information after making necessary adjustments.

4. No Opening and Closing Balances: In this account, no opening and closing balances of cash and bank are recorded.

5. Same as Profit & Loss Account: This account is prepared in the same manner in which a Profit & Loss Account is prepared, considering, all adjustments relating to the current year.

6. Exclude Past and Future Items: It excludes all the items of income and expenditure which do not pertain to the current period.

7. End-balance of this Account: The end-balance of the Income and Expenditure Account, which may be either “excess of income over expenditures’ or ‘excess of expenditure over income’ would be added to or deducted from, as the case may be, the capital fund, on the liabilities side of the Balance Sheet.

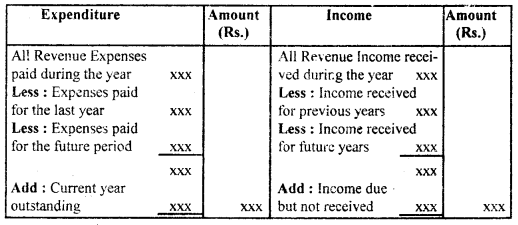

Steps in the Preparation of Income and Expenditure Account:

1. From the Receipts and Payments Account exclude the opening and closing balance of cash and bank as they are not an income.

2. Exclude the items of capital nature as these are to be shown in the balance sheet.

3. Take out the revenue receipts only for the current year to be shown on the income side of the Income and Expenditure Account. These are adjusted by excluding the amounts relating to the preceding and the succeeding periods and including the amounts relating to the current year not yet received.

4. Take out the revenue payments only for the current year to be shown on the expenditure side of the Income and Expenditure Account. These are adjusted by excluding the amounts relating to the preceding and the succeeding periods and including the amounts relating to the current year not yet paid.

5. Make the adjustments to non-cash items like

(a) Depreciation on fixed assets.

(b) Provision for doubtful debts, if required.

(c) Profit or Loss on sale of fixed assets etc.

For determining the surplus/deficit for the current year.

So, we can also prepare the Income and Expenditure Account with the help of the following methods after considering the Receipt and Payment Account and information given

Income and Expenditure Account for the year ended………..

Format of Income and Expenditure Account

Income and Expenditure Account for the year ended…………..

The distinction between Income and Expenditure Account and Receipt and Payment Account

Balance Sheet:

Not-For-Profit organizations prepare a Balance Sheet at the end of an accounting period to ascertain the financial position of the organization. The preparation of their Balance Sheet is the same as that of the business or trading entities. It is prepared in the usual way showing assets on the ‘right-hand side and the liabilities on the ‘left-hand side. However, the term capital is not to be found.

Instead, there will be a capital fund or a general fund, or an accumulated fund, and the surplus or deficit as per the Income and Expenditure Account shall be added to or deducted from this fund. Some capitalized items like legacies, entrance fees, and life membership fees directly (added) in the capital fund.

Sometimes it becomes necessary to prepare a Balance Sheet at the beginning of the year in order to find out the opening balance of the capital/general fund.

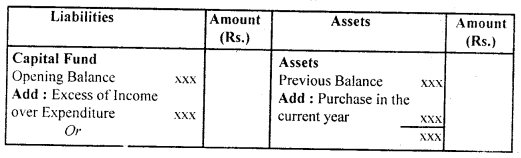

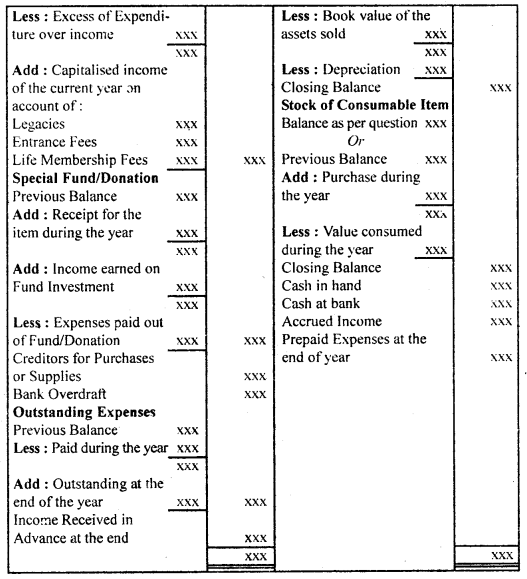

Steps in the Preparation of Balance Sheet:

1. Find out the Capital fund as per the Opening Balance Sheet and add surplus from the Income and Expenditure Account. Then, add capitalized items like legacies, entrance fees, and life membership fees, etc. received during the year.

2. Put all the fixed assets (from the opening balance sheet) with additions (from Receipts and Payments Account) after charging depreciation (as per Income and Expenditure Account), on the assets side of the balance sheet.

3. Compare items on the receipts side of the Receipts and Payments Account with the income side of the Income and Expenditure Account to find out the amounts of

(a) Subscription due but not yet received,

(b) income received in advance,

(c) Sale of fixed assets made during the year,

(d) Items to be capitalized etc.

4. Compare items on the payment side of the Receipts and Payments Account with the expenditure side of the Income and Expenditure Account to find out the amount of

(a) Outstanding Expenses,

(b) Prepaid Expenses,

(c) Purchases of a fixed asset during the year,

(d) Depreciation on fixed assets,

(e) Stock of consumable items like stationery in hand,

(f) Closing balance of cash in hand and cash at bank etc.

Format of Balance Sheet

Balance Sheet of…………………

as on ………………….

Some important items relating to Not-For-Profit Organisations

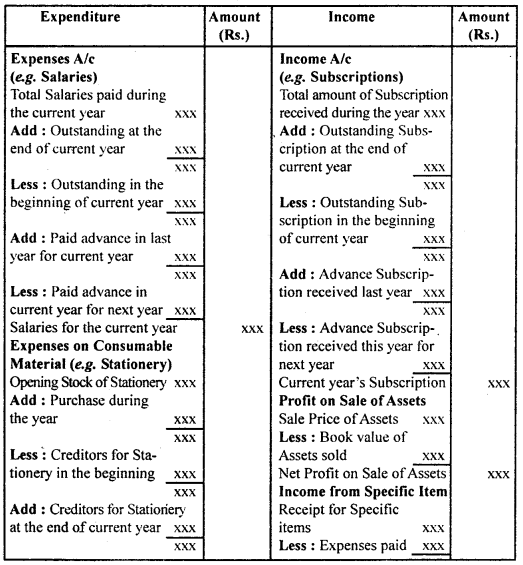

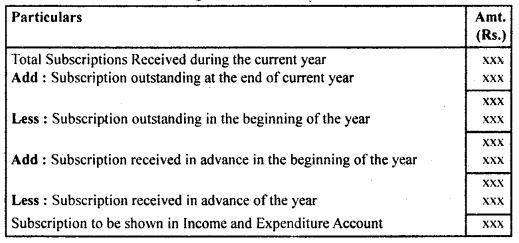

1. Subscription: It is the amount paid by the members of the organization periodically so that their membership is not canceled. This is the main source of income of Not-For-Profit Organisations.

Treatment:

1. The total amount of subscriptions received during the accounting period is shown on the receipt side (Dr. side) of the Receipt and Payment Account.

2. Subscription related to the current period shown in the income side (Cr. side) of Income and Expenditure Account. The amount of subscription to be shown in the Income and Expenditure Account is calculated as follows :

Table Showing Calculation of Subscriptions

Or

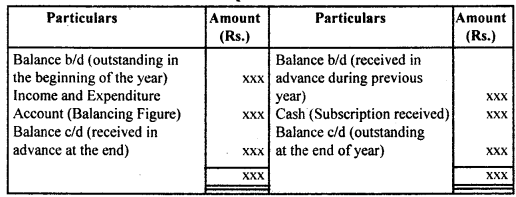

Subscription Account

3. Subscription Outstanding at the end of the year is shown on the assets side of the Balance Sheet and subscription received in advance in the current year for the next year is shown on the liabilities side of the Balance Sheet.

2. Donations: It is a type of gift in cash or in property received from some person, firm, or company. The donation can be for specific purposes or for general purposes.

Both the donation received appears on the receipts side of the Receipts and Payments Account.

1. Specific Donations: If the amount received as the donation is for a specific purpose such as a donation for extension of the existing building, donation for the library, for construction of new computer laboratory, etc., it is capitalized and is shown on the liabilities side of Balance Sheet.

2.. General Donations: Such donations are to be utilized to promote the general purpose of the organization. It is of two types:

(a) General Donation of Big Amount: It is shown on the liability side of the Balance Sheet because it is non-recurring in nature as the donations of huge amounts cannot be expected every year.

(b) General Donation of Small Amount: These are treated as revenue receipts as it is a regular source of income hence, it is taken to the income side of the Income and Expenditure Account of the current year.

3. Legacies: It is in the nature of a gift, received in cash or in the property as per the will of a deceased person. It is not treated as an income because it is not of recurring nature. Such receipts come very rarely and therefore it is of a capital nature and is shown on the liabilities side of the Balance Sheet. It appears on the receipt side of the Receipts and Payments Account and is directly added to Capital Fund in the Balance Sheet. However, legacies of the small amount may be treated as income and show on the income side of the Income and Expenditure Account.

4. Life Membership Fees: In order to become a member of an organization for the whole of the life, some members pay the fee in lump sum i.e. once in their lifetime. It is a receipt of non¬recurring nature since the members will not be required to pay the fees regularly. It is shown on the receipt side of the Receipt and Payment Account and added to the Capital Fund in the Balance Sheet. It should not be credited to the Income and Expenditure Account.

5. Entrance Fees: The entrance fee also known as the Admission Fee is paid only once by the member at the time of becoming a member.

1. In the case of organizations like clubs and some charitable institutions, where the membership is limited and the amount of Entrance Fees is quite large, it is treated as the non-recurring item and added directly to Capital Fund in the Balance Sheet and also shows in the receipt side of the Receipt and Payment Account.

2. For some organizations like educational institutions the entrance fee is a regular income and the amount is quite small. So it is treated as the recurring item and shown in the income side of the Income and Expenditure Account. It is also shown on the receipt side by the Receipt and Payment Account.

From the examination point of view, if there is no specific instruction about Entrance Fees, it should be treated as Capital Receipt and directly added to Capital Fund in the Balance Sheet.

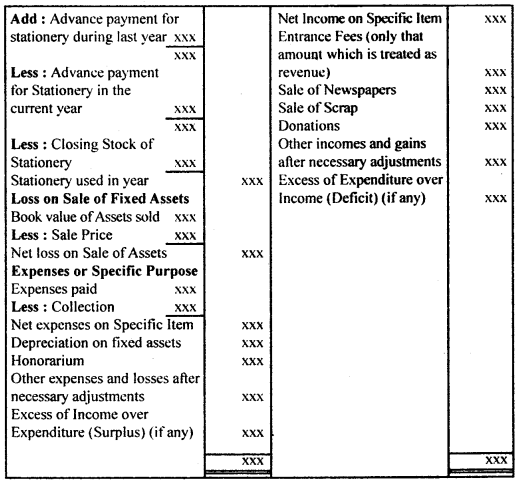

6. Sale of Old Assets: Receipt from the sale of the old asset appears in the receipt side of Receipt and Payment Account. Only the profit or loss on the sale of a fixed asset is credited or debited, as the case may be, to the Income and Expenditure Account. In the Balance Sheet, the book value of the asset sold should be deducted from the relevant asset.

7. Sale of Periodicals: Receipts from the sale of periodicals shown in the receipt side of Receipt and Payment Account. It is an item of recurring nature and shown in the income side of the Income and Expenditure Account.

8. Sale of Sports Materials: The sale of sports materials like old bats, old nets, etc. is a regular feature with any sports club. It is treated as revenue income on the assumption that their book value is zero. It is therefore shown in the income side of the Income and Expenditure Account. It is also shown on the receipt side of the Receipt and Payment Account.

9. Payment of Honorarium: It is the payment made to a person for his specific services rendered by him, not as a regular employee. This is an item of expense and is shown in the ‘debit or expenditure side’ of the Income and Expenditure Account.

→ Endowment Fund: “It is a fund arising from a bequest or gift, the income of which is devoted for a specific purpose.” – Eric L. Kohler

Thus, Endowment Fund is a capital receipt and is shown on the liabilities side of the Balance Sheet.

→ Government Grant: Some organizations like schools, colleges, public hospitals, etc. depend upon Government grants for their activities.

It is shown on the receipt side of the Receipt and Payment Account:

- The maintenance grant is a recurring grant. It is treated as a revenue receipt and shown on the income side of the Income and Expenditure Account.

- Grants such as building grants are treated as capital receipts and transferred to the building fund account.

→ Cash subsidy: Some Not-For-Profit Organisations receive cash subsidies from the Government or Government agencies. This subsidy is also treated as revenue income for the year in which it is received.

→ Special Funds: Not-For-Profit Organisation creates some special funds for a specific purpose such as ‘prize funds’, ‘match fund’ and ‘sports fund’ etc. The amount of such fund is invested in securities and the income earned on such investment is added to the respective fund, not credited to the Income and Expenditure Account. Similarly, the expenses incurred on such a specific purpose are also deducted from the fund.

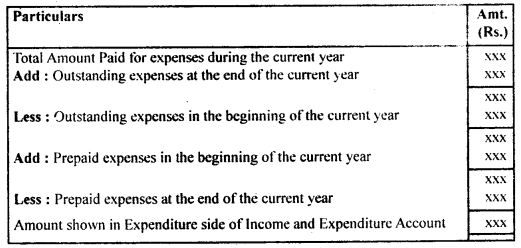

→ Stationery (or some consumable items): Expenses incurred on Stationery (or some consumable items) are charged to the Income and Expenditure Account.

If the opening or closing stock of stationery is given, then the amount of stationery consumed during the year will be shown in the Income and Expenditure Account and the closing stock in the Balance Sheet.

The calculation for Expenses for the Current Year

Total Amount paid shown in Payment side of Receipt and Payment Account. Outstanding experiences at the end of the current year shown in the Liabilities side of the Balance Sheet and prepaid at the end shown in the Assets side of the Balance Sheet.

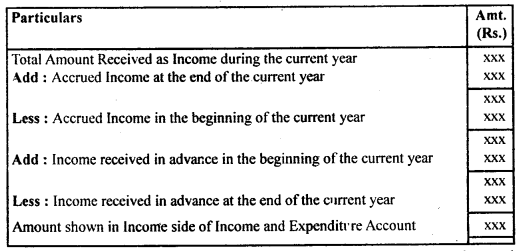

The calculation for Income for the Current Year

Total Amount Received shown in Receipt side of Receipt and Payment Account. Accrued income at the end of the current year shown in the assets side of the Balance Sheet and Income received in advance at the end of the current year shown on the liabilities side of the Balance Sheet.