ML Aggarwal Class 10 Solutions for ICSE Maths Chapter 2 Banking Ex 2

These Solutions are part of ML Aggarwal Class 10 Solutions for ICSE Maths. Here we have given ML Aggarwal Class 10 Solutions for ICSE Maths Chapter 2 Banking Ex 2

More Exercises

- ML Aggarwal Class 10 Solutions for ICSE Maths Chapter 2 Banking EX 2

- ML Aggarwal Class 10 Solutions for ICSE Maths Chapter 2 Banking MCQS

- ML Aggarwal Class 10 Solutions for ICSE Maths Chapter 2 Banking Chapter Test

Question 1.

Shweta deposits Rs. 350 per month in a recurring deposit account for one year at the rate of 8% p.a. Find the amount she will receive at the time of maturity.

Solution:

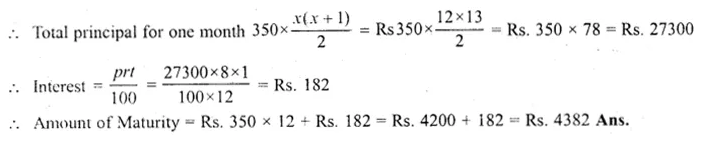

Deposit per month = Rs 350,

Rate of interest = 8% p.a.

Period (x) = 1 year

= 12 months

Question 2.

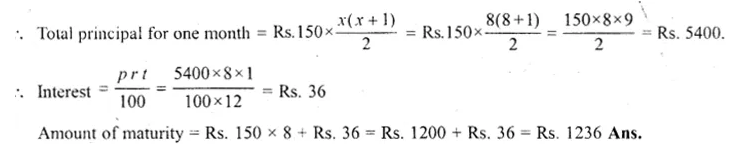

Salom deposited Rs 150 per month in a bank for 8 months under the Recurring Deposit Scheme. ‘What will be the maturity value of his deposit if the rate of interest is 8% per annum ?

Solution:

Deposit per month = Rs. 150

Rate of interest = 8% per

Period (x) = 8 month

Question 3.

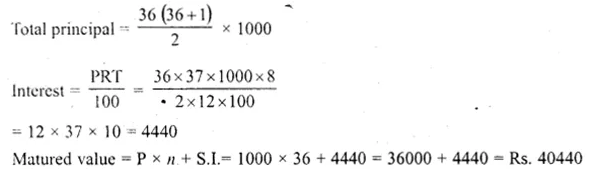

Mrs. Goswami deposits Rs. 1000 every month in a recurring deposit account for 3 years at 8% interest per annum. Find the matured value. (2009)

Solution:

Deposit per month (P) = Rs. 1000

Period = 3 years = 36 months

Rate = 8%

Question 4.

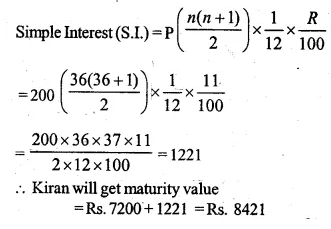

Kiran deposited Rs. 200 per month for 36 months in a bank’s recurring deposit account. If the banks pays interest at the rate of 11% per annum, find the amount she gets on maturity ?

Solution:

Amount deposited month (P) = Rs. 200

Period (n) = 36 months,

Rate (R) = 11% p.a.

Now amount deposited in 36 months = Rs. 200 x 36 = Rs 7200

Question 5.

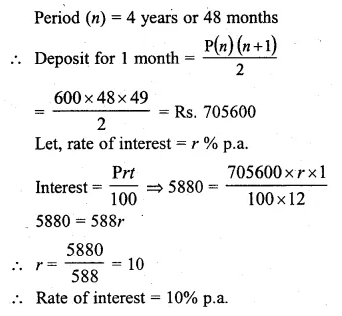

Haneef has a cumulative bank account and deposits Rs. 600 per month for a period of 4 years. If he gets Rs. 5880 as interest at the time of maturity, find the rate of interest.

Solution:

Interest = Rs. 58800

Monthly deposit (P) = Rs. 600

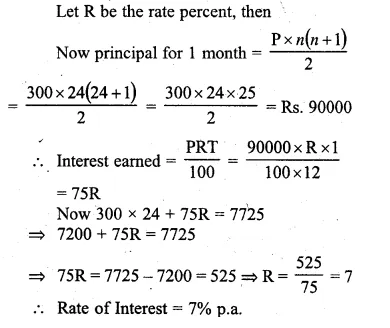

Question 6.

David opened a Recurring Deposit Account in a bank and deposited Rs. 300 per month for two years. If he received Rs. 7725 at the time of maturity, find the rate of interest per annum. (2008)

Solution:

Deposit during one month (P) = Rs. 300

Period = 2 years = 24 months.

Maturity value = Rs. 7725

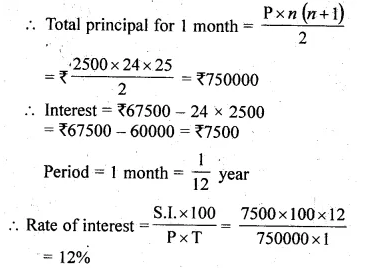

Question 7.

Mr. Gupta-opened a recurring deposit account in a bank. He deposited Rs. 2500 per month for two years. At the time of maturity he got Rs. 67500. Find :

(i) the total interest earned by Mr. Gupta.

(ii) the rate of interest per annum.

Solution:

Deposit per month = Rs. 2500

Period = 2 years = 24 months

Maturity value = Rs. 67500

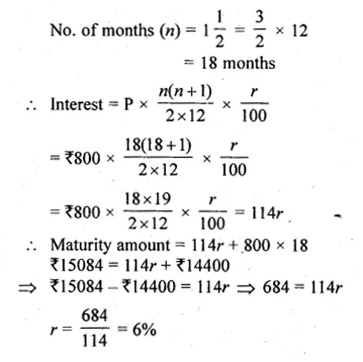

Question 8.

Shahrukh opened a Recurring Deposit Account in a bank and deposited Rs 800 per month for \(1 \frac { 1 }{ 2 } \) years. If he received Rs 15084 at the time of maturity, find the rate of interest per annum.

Solution:

Money deposited by Shahrukh per month (P)= Rs 800

r = ?

Question 9.

Mohan has a recurring deposit account in a bank for 2 years at 6% p.a. simple interest. If he gets Rs 1200 as interest at the time of maturity, find:

(i) the monthly instalment

(ii) the amount of maturity. (2016)

Solution:

Interest = Rs 1200

Period (n) = 2 years = 24 months

Rate (r) = 6% p.a.

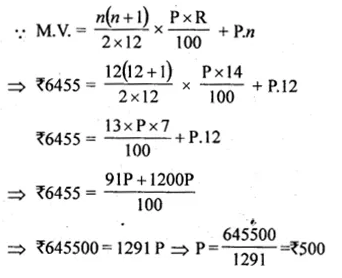

Question 10.

Mr. R.K. Nair gets Rs 6,455 at the end of one year at the rate of 14% per annum in a recurring deposit account. Find the monthly instalment.

Solution:

Let monthly instalment is Rs P

here n = 1 year = 12 months

n = 12

Question 11.

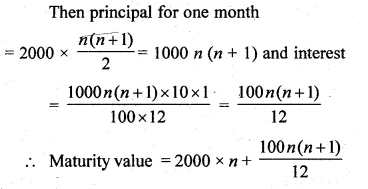

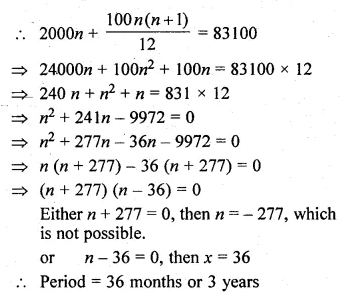

Samita has a recurring deposit account in a bank of Rs 2000 per month at the rate of 10% p.a. If she gets Rs 83100 at the time of maturity. Find the total time for which the account was held.

Solution:

Deposit per month = Rs 2000,

Rate of interest = 10%, Let period = n months

Hope given ML Aggarwal Class 10 Solutions for ICSE Maths Chapter 2 Banking Ex 2 are helpful to complete your math homework.

If you have any doubts, please comment below. Learn Insta try to provide online math tutoring for you.